Vous aimerez peut-être aussi

- SIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)D'EverandSIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)Évaluation : 5 sur 5 étoiles5/5 (1)

- Incoterms Chart of Responsibility 2020 1Document1 pageIncoterms Chart of Responsibility 2020 1Hiro Katsumoto100% (1)

- CFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)D'EverandCFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)Évaluation : 4.5 sur 5 étoiles4.5/5 (5)

- Auditing Theory - PRTCDocument35 pagesAuditing Theory - PRTCjpbluejn100% (8)

- CFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)D'EverandCFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)Évaluation : 5 sur 5 étoiles5/5 (1)

- Ilovepdf MergedDocument688 pagesIlovepdf MergedSpade XPas encore d'évaluation

- CISA Exam-Testing Concept-Knowledge of Risk AssessmentD'EverandCISA Exam-Testing Concept-Knowledge of Risk AssessmentÉvaluation : 2.5 sur 5 étoiles2.5/5 (4)

- Audit Testbank-Bobadilla PDFDocument560 pagesAudit Testbank-Bobadilla PDFNir Noel Aquino100% (12)

- The Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiD'EverandThe Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiPas encore d'évaluation

- Ch13 - Substantive Audit Testing Financing and Investing CycleDocument18 pagesCh13 - Substantive Audit Testing Financing and Investing CycleAbas Norfarina100% (2)

- 5 Audit PlanningDocument53 pages5 Audit PlanningrogealynPas encore d'évaluation

- Auditing Theory PRTC1Document35 pagesAuditing Theory PRTC1Kevin James Sedurifa OledanPas encore d'évaluation

- Statement of Account: Blok A2-3-1, Flat Ampang Hilir, Taman Ampang Hilir Ampang 68000 SELANGORDocument2 pagesStatement of Account: Blok A2-3-1, Flat Ampang Hilir, Taman Ampang Hilir Ampang 68000 SELANGORNoriza GhazaliPas encore d'évaluation

- Merchandising BusinessDocument10 pagesMerchandising BusinessMichiiee BatallaPas encore d'évaluation

- C. A Review Engagement Focuses On Providing Limited Assurance On Financial Statement of A Private CompanyDocument14 pagesC. A Review Engagement Focuses On Providing Limited Assurance On Financial Statement of A Private CompanyNoro100% (1)

- AUDIT - 1ST Preboard (SET A)Document13 pagesAUDIT - 1ST Preboard (SET A)KriztleKateMontealtoGelogo0% (1)

- ch13 - Substantive Audit Testing - Financing and Investing CycleDocument19 pagesch13 - Substantive Audit Testing - Financing and Investing CycleJoshua WacanganPas encore d'évaluation

- Substantive Audit Testing CompDocument36 pagesSubstantive Audit Testing CompJoshua WacanganPas encore d'évaluation

- Auditing Attestation and AssuranceDocument10 pagesAuditing Attestation and Assurancechiji chzzzmeowPas encore d'évaluation

- Auditing Concepts Psa Based QuestionsDocument665 pagesAuditing Concepts Psa Based QuestionsMae Danica CalunsagPas encore d'évaluation

- Q7 Reviewer (Completing The Audit)Document7 pagesQ7 Reviewer (Completing The Audit)John Lexter MacalberPas encore d'évaluation

- C. A Review Engagement Focuses On Providing Limited Assurance On Financial Statement of A PrivateDocument13 pagesC. A Review Engagement Focuses On Providing Limited Assurance On Financial Statement of A PrivateNoroPas encore d'évaluation

- Ch01 - Auditing, Attestation, and AssuranceDocument9 pagesCh01 - Auditing, Attestation, and AssuranceRamon Jonathan Sapalaran100% (2)

- At TestbankDocument5 pagesAt TestbankMartinez JomarPas encore d'évaluation

- Nurse Staffing Ratio PosterboardDocument1 pageNurse Staffing Ratio Posterboardapi-260974225100% (1)

- ReSA B42 AUD First PB Exam Questions Answers Solutions PDFDocument24 pagesReSA B42 AUD First PB Exam Questions Answers Solutions PDFNamnam KimPas encore d'évaluation

- 618B - Advanced Audit and AssuranceDocument25 pages618B - Advanced Audit and AssuranceZain MaggssiPas encore d'évaluation

- Assurance by KonrathDocument8 pagesAssurance by KonrathDominic Earl AblanquePas encore d'évaluation

- Chapter 1 Auditing and Assurance Services: Multiple Choice QuestionsDocument9 pagesChapter 1 Auditing and Assurance Services: Multiple Choice Questionsalmira garciaPas encore d'évaluation

- Final Exam - Auditing & Assurance PrinciplesDocument13 pagesFinal Exam - Auditing & Assurance PrinciplesGia Sarah Barillo BandolaPas encore d'évaluation

- AuditingDocument10 pagesAuditingGhillian Mae GuiangPas encore d'évaluation

- AUDIT Mar 12 With AnswersDocument37 pagesAUDIT Mar 12 With AnswersCybill AiraPas encore d'évaluation

- Auditing Theory PRTC PDFDocument35 pagesAuditing Theory PRTC PDFArah OpalecPas encore d'évaluation

- Audit Theory-WPS OfficeDocument6 pagesAudit Theory-WPS OfficeApril Rose Sobrevilla DimpoPas encore d'évaluation

- AuditingDocument5 pagesAuditingMariel Jane EngracialPas encore d'évaluation

- Auditing Theory PRTCDocument44 pagesAuditing Theory PRTCMisa AmanePas encore d'évaluation

- Source: Auditing: A Risk Analysis Approach 5 Edition by Larry F. KonrathDocument19 pagesSource: Auditing: A Risk Analysis Approach 5 Edition by Larry F. KonrathMelanie SamsonaPas encore d'évaluation

- Multiple-Choice QuestionsDocument17 pagesMultiple-Choice QuestionsathenaPas encore d'évaluation

- AT 2nd Monthly AssessmentDocument8 pagesAT 2nd Monthly AssessmentCiena Mae AsasPas encore d'évaluation

- CH 13Document18 pagesCH 13xxxxxxxxxPas encore d'évaluation

- AuDocument5 pagesAuJohn Paulo SamontePas encore d'évaluation

- N C O B A A: Ational Ollege F Usiness ND RTSDocument9 pagesN C O B A A: Ational Ollege F Usiness ND RTSNico evansPas encore d'évaluation

- Lí thuyết kiểm toánDocument13 pagesLí thuyết kiểm toánLinh Nguyễn Thị KhánhPas encore d'évaluation

- NAQDOWN - Elimination Auditing TheoryDocument5 pagesNAQDOWN - Elimination Auditing TheoryKarina Barretto AgnesPas encore d'évaluation

- Auditing Bit BankDocument22 pagesAuditing Bit Bankanon_957979387Pas encore d'évaluation

- 602U1 - AuditingDocument21 pages602U1 - AuditingZain MaggssiPas encore d'évaluation

- Pre Test 4 SET ADocument13 pagesPre Test 4 SET AMotchi RockyPas encore d'évaluation

- AUDITING Material 3Document35 pagesAUDITING Material 3Blessy Zedlav LacbainPas encore d'évaluation

- CH 13Document19 pagesCH 13pesoload100Pas encore d'évaluation

- 3349 - Midterm Exam Winter 2015 SOLUTIONDocument14 pages3349 - Midterm Exam Winter 2015 SOLUTIONKathya SilvaPas encore d'évaluation

- Exam 14 February 2020 Questions and AnswersDocument7 pagesExam 14 February 2020 Questions and AnswersDan Andrei BongoPas encore d'évaluation

- Compilation atDocument20 pagesCompilation atAshley Levy San PedroPas encore d'évaluation

- AUDITINGDocument8 pagesAUDITINGby ScribdPas encore d'évaluation

- 02 Quiz On Topic 2 With Answer KeyDocument3 pages02 Quiz On Topic 2 With Answer KeyNye NyePas encore d'évaluation

- Chapter 4 Engagement Planning: Multiple Choice QuestionsDocument21 pagesChapter 4 Engagement Planning: Multiple Choice QuestionsNicale JeenPas encore d'évaluation

- Multiple-Choice QuestionsDocument20 pagesMultiple-Choice QuestionsRafael GarciaPas encore d'évaluation

- JHLKHNDocument114 pagesJHLKHNgladsPas encore d'évaluation

- AlibabaDocument2 pagesAlibabaHicham MaatoukPas encore d'évaluation

- My Internship Report Bank Alfalah Islamic Ltd. CompletedDocument63 pagesMy Internship Report Bank Alfalah Islamic Ltd. Completedanon_512862546Pas encore d'évaluation

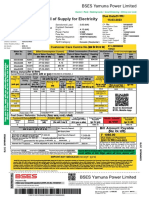

- Bill of Supply For Electricity: BSES Yamuna Power LimitedDocument2 pagesBill of Supply For Electricity: BSES Yamuna Power LimitedSUJIT SINGHPas encore d'évaluation

- Issued By: Go Air: Nikitha Online Services R04AG3006Document2 pagesIssued By: Go Air: Nikitha Online Services R04AG3006NIKITHA ONLINESERVICESPas encore d'évaluation

- Account Usage and Recharge Statement From 02-May-2023 To 17-May-2023Document30 pagesAccount Usage and Recharge Statement From 02-May-2023 To 17-May-2023Arivazhagan RajendiranPas encore d'évaluation

- e-StatementBRImo 581201036477530 Oct2023 20231110 175401Document1 pagee-StatementBRImo 581201036477530 Oct2023 20231110 175401MuhammadIqbalHanafiPas encore d'évaluation

- Don T Get Left Behind - Why Fis and Large Corporates Should Migrate To Iso 20022 StandardsDocument8 pagesDon T Get Left Behind - Why Fis and Large Corporates Should Migrate To Iso 20022 StandardsJózsef PataiPas encore d'évaluation

- Annual Report 2017-18 - United India Insurance PDFDocument394 pagesAnnual Report 2017-18 - United India Insurance PDFjusmi100% (1)

- Tax Invoice: TIN#: 1000145GST501Document1 pageTax Invoice: TIN#: 1000145GST501aishathPas encore d'évaluation

- Bill of LadingDocument1 pageBill of LadingJohn Mark VerarPas encore d'évaluation

- The Implementation of Ten Operation Management Decision in BusinessDocument32 pagesThe Implementation of Ten Operation Management Decision in BusinessNormyzatul AkmalPas encore d'évaluation

- Ye Olde Book Store Opened Its Doors For Business OnDocument2 pagesYe Olde Book Store Opened Its Doors For Business OnAmit PandeyPas encore d'évaluation

- ZT - Zte Mu5001 5g Mini Router DatasheetDocument2 pagesZT - Zte Mu5001 5g Mini Router DatasheetThomvar VargasPas encore d'évaluation

- Module 3 Lab Manual 5 Input Validation - AnswerDocument9 pagesModule 3 Lab Manual 5 Input Validation - AnswerLakshmi PriyaPas encore d'évaluation

- Qip PesentationDocument14 pagesQip Pesentationapi-340409341Pas encore d'évaluation

- Problem 3 - Adjusting Entries General Journal: Date Particulars F DebitDocument4 pagesProblem 3 - Adjusting Entries General Journal: Date Particulars F DebityeshaPas encore d'évaluation

- Revision Quizzes 4Document6 pagesRevision Quizzes 4Nghi AnPas encore d'évaluation

- Bank of Punjab ATM EnglishDocument43 pagesBank of Punjab ATM EnglishphooolPas encore d'évaluation

- Period Close Exceptions Report (XML)Document6 pagesPeriod Close Exceptions Report (XML)Priya NimmagaddaPas encore d'évaluation

- Chap 1-4Document20 pagesChap 1-4Rose Ann Robante TubioPas encore d'évaluation

- Omni-Channel Logistics in The Finnish Retail MarketDocument89 pagesOmni-Channel Logistics in The Finnish Retail MarketClarence CHENPas encore d'évaluation

- DNR PDFDocument1 pageDNR PDFnurhayatiPas encore d'évaluation

- CH 01Document79 pagesCH 01Ko TunPas encore d'évaluation

- Assignment in Internal ControlDocument2 pagesAssignment in Internal ControlMAG MAGPas encore d'évaluation

- EBS 122 Cum RCD FINDocument118 pagesEBS 122 Cum RCD FINnicuPas encore d'évaluation

- CC Major SyllabusDocument25 pagesCC Major Syllabusganesh.gc8747Pas encore d'évaluation