Vous aimerez peut-être aussi

- Corporate Financial Analysis with Microsoft ExcelD'EverandCorporate Financial Analysis with Microsoft ExcelÉvaluation : 5 sur 5 étoiles5/5 (1)

- Guide to Contract Pricing: Cost and Price Analysis for Contractors, Subcontractors, and Government AgenciesD'EverandGuide to Contract Pricing: Cost and Price Analysis for Contractors, Subcontractors, and Government AgenciesPas encore d'évaluation

- Assignment 3Document7 pagesAssignment 3Abdullah ghauriPas encore d'évaluation

- Full and Ifrs SmeDocument14 pagesFull and Ifrs SmeAmir Ayub100% (2)

- Capital Structure TheoriesDocument8 pagesCapital Structure TheoriesLinet OrigiPas encore d'évaluation

- Introduction To Valuation Techniques Section 1Document11 pagesIntroduction To Valuation Techniques Section 1goody89rusPas encore d'évaluation

- Cash Accounting, Accrual Accounting, and Discounted Cash Flow ValuationDocument32 pagesCash Accounting, Accrual Accounting, and Discounted Cash Flow ValuationHanh Mai TranPas encore d'évaluation

- CVP NumericalDocument13 pagesCVP NumericalChandan JobanputraPas encore d'évaluation

- Primary MKTDocument24 pagesPrimary MKTdanbrowndaPas encore d'évaluation

- Chapter-9, Capital StructureDocument21 pagesChapter-9, Capital StructurePooja SheoranPas encore d'évaluation

- Warren Larsen Chp1 (Principles of Accounting)Document147 pagesWarren Larsen Chp1 (Principles of Accounting)annie100% (1)

- Concept and Classification of BetaDocument16 pagesConcept and Classification of BetamonuPas encore d'évaluation

- Investment Analysis & Portfolio EvaluationDocument7 pagesInvestment Analysis & Portfolio EvaluationchandreshmehraPas encore d'évaluation

- Portfolio TheoryDocument25 pagesPortfolio Theoryray92100Pas encore d'évaluation

- Jan 2018Document34 pagesJan 2018alekhya mannePas encore d'évaluation

- LeverageDocument36 pagesLeveragereddyhareePas encore d'évaluation

- Capital and Revenue ExpendituereDocument30 pagesCapital and Revenue ExpendituereDheeraj Seth0% (1)

- Investment Banking Chapter 1Document27 pagesInvestment Banking Chapter 1ravindergudikandulaPas encore d'évaluation

- 13 Capital Structure (Slides) by Zubair Arshad PDFDocument34 pages13 Capital Structure (Slides) by Zubair Arshad PDFZubair ArshadPas encore d'évaluation

- 5.valuation of BusinessDocument6 pages5.valuation of BusinessHalf-God Half-ManPas encore d'évaluation

- Depreciation: Depreciation Is A Term Used inDocument10 pagesDepreciation: Depreciation Is A Term Used inalbertPas encore d'évaluation

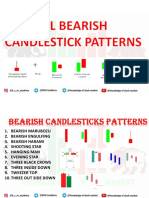

- All Bearish Candle Stick PatternsDocument18 pagesAll Bearish Candle Stick PatternsxhghdghPas encore d'évaluation

- Meaning and Characteristics of Financial PlanningDocument17 pagesMeaning and Characteristics of Financial PlanningROOBINIPas encore d'évaluation

- Chapter 04 Risk, Return, and The Portfolio TheoryDocument55 pagesChapter 04 Risk, Return, and The Portfolio TheoryAGPas encore d'évaluation

- Security Analysis & Portfolio Management Lec 1Document55 pagesSecurity Analysis & Portfolio Management Lec 1Anonymous utSFl8Pas encore d'évaluation

- Ifm-Chapter 9-Forecasting Financial Statement (Slide)Document36 pagesIfm-Chapter 9-Forecasting Financial Statement (Slide)minhhien222Pas encore d'évaluation

- Importance of Mutual FundsDocument14 pagesImportance of Mutual FundsMukesh Kumar SinghPas encore d'évaluation

- EVA Vs ROIDocument5 pagesEVA Vs ROINikhil KhobragadePas encore d'évaluation

- Special Economic ZoneDocument4 pagesSpecial Economic ZoneDhruvesh ModiPas encore d'évaluation

- Analysis of Stock MarketDocument19 pagesAnalysis of Stock MarketNibin Varghese CharleyPas encore d'évaluation

- Trends in International ManagementDocument5 pagesTrends in International ManagementAleksandra RudchenkoPas encore d'évaluation

- A Study Applying DCF Technique For Valuing Indian IPO's Case Studies of CCDDocument11 pagesA Study Applying DCF Technique For Valuing Indian IPO's Case Studies of CCDarcherselevators100% (1)

- Lecture 9 M17EFA - Company Valuation 2 1Document48 pagesLecture 9 M17EFA - Company Valuation 2 1822407Pas encore d'évaluation

- Projected Cash FlowDocument10 pagesProjected Cash FlowAni SinghPas encore d'évaluation

- IPCC - FAST TRACK MATERIAL - 35e PDFDocument69 pagesIPCC - FAST TRACK MATERIAL - 35e PDFKunalKumarPas encore d'évaluation

- Introduction To Financial ManagemntDocument29 pagesIntroduction To Financial ManagemntibsPas encore d'évaluation

- Sulimanalgelatema BlogspotDocument41 pagesSulimanalgelatema Blogspotheatdownblog80% (5)

- Dupont Analysis of Pharma CompaniesDocument8 pagesDupont Analysis of Pharma CompaniesKalyan VsPas encore d'évaluation

- Capital Structure: Theory and PolicyDocument31 pagesCapital Structure: Theory and PolicySuraj ShelarPas encore d'évaluation

- MGT705 - Advanced Cost and Management Accounting Midterm 2013Document1 pageMGT705 - Advanced Cost and Management Accounting Midterm 2013sweet haniaPas encore d'évaluation

- How To Write A Ratio AnalysisDocument2 pagesHow To Write A Ratio AnalysisLe TanPas encore d'évaluation

- Based On Session 5 - Responsibility Accounting & Transfer PricingDocument5 pagesBased On Session 5 - Responsibility Accounting & Transfer PricingMERINAPas encore d'évaluation

- ACC803 Advanced Financial Reporting: Week 2: Financial Statement Preparation and PresentationDocument21 pagesACC803 Advanced Financial Reporting: Week 2: Financial Statement Preparation and PresentationRavinesh PrasadPas encore d'évaluation

- Lecture 2 Behavioural Finance and AnomaliesDocument15 pagesLecture 2 Behavioural Finance and AnomaliesQamarulArifin100% (1)

- Chapter 16Document23 pagesChapter 16JJPas encore d'évaluation

- CH 11Document48 pagesCH 11Pham Khanh Duy (K16HL)Pas encore d'évaluation

- Accounting For Bonus and Right of Issue.Document38 pagesAccounting For Bonus and Right of Issue.Jacob SphinixPas encore d'évaluation

- Assignment of Time Value of MoneyDocument3 pagesAssignment of Time Value of MoneyMuxammil IqbalPas encore d'évaluation

- Investment Appraisal Taxation, InflationDocument8 pagesInvestment Appraisal Taxation, InflationJiya RajputPas encore d'évaluation

- Cost of Capital Lecture Slides in PDF FormatDocument18 pagesCost of Capital Lecture Slides in PDF FormatLucy UnPas encore d'évaluation

- Chapter 04 Working Capital 1ce Lecture 050930Document71 pagesChapter 04 Working Capital 1ce Lecture 050930rthillai72Pas encore d'évaluation

- Fundamentals of Corporate Finance, 2/e: Robert Parrino, Ph.D. David S. Kidwell, Ph.D. Thomas W. Bates, PH.DDocument56 pagesFundamentals of Corporate Finance, 2/e: Robert Parrino, Ph.D. David S. Kidwell, Ph.D. Thomas W. Bates, PH.DNguyen Thi Mai Lan100% (1)

- Construction Cost Handbook Korea 2012n PDFDocument73 pagesConstruction Cost Handbook Korea 2012n PDFSharafaz ShamsudeenPas encore d'évaluation

- Financial AdvisoryDocument19 pagesFinancial AdvisoryAbhijeet SinghPas encore d'évaluation

- Chapter Four StockDocument16 pagesChapter Four Stockሔርሞን ይድነቃቸው100% (1)

- Chapter 11 - Cost of Capital - Text and End of Chapter QuestionsDocument63 pagesChapter 11 - Cost of Capital - Text and End of Chapter QuestionsSaba Rajpoot50% (2)

- Statement of Cash Flows: Preparation, Presentation, and UseD'EverandStatement of Cash Flows: Preparation, Presentation, and UsePas encore d'évaluation

- Research Methodology:: The Objectives For Which Study Has Been Undertaken AreDocument13 pagesResearch Methodology:: The Objectives For Which Study Has Been Undertaken Arearpita64Pas encore d'évaluation

- Internal Rate of ReturnDocument1 pageInternal Rate of Returnharish chandraPas encore d'évaluation

- Project Report On Employees SatisfactionDocument64 pagesProject Report On Employees Satisfactionharish chandra0% (2)

- Internal Rate of ReturnDocument1 pageInternal Rate of Returnharish chandraPas encore d'évaluation

- Risk and Return: Financial ManagementDocument3 pagesRisk and Return: Financial Managementharish chandraPas encore d'évaluation

- Net Present ValueDocument2 pagesNet Present Valueharish chandraPas encore d'évaluation

- Organization Design and DevelopmentDocument3 pagesOrganization Design and Developmentharish chandraPas encore d'évaluation

- Environment in Human Resource ManagementDocument9 pagesEnvironment in Human Resource Managementharish chandraPas encore d'évaluation

- Finnncial AnalysisDocument8 pagesFinnncial Analysisharish chandraPas encore d'évaluation

- Managerial Position To Fulfill Some Specific Managerial Activities or Tasks. ThisDocument2 pagesManagerial Position To Fulfill Some Specific Managerial Activities or Tasks. Thisharish chandraPas encore d'évaluation

- Kiss PrincipleDocument4 pagesKiss Principleharish chandraPas encore d'évaluation

- Corporate Ch02Document40 pagesCorporate Ch02LeiPas encore d'évaluation

- Unit 2: Bussiness CommunicationDocument15 pagesUnit 2: Bussiness Communicationharish chandraPas encore d'évaluation

- Trial BalanceDocument21 pagesTrial BalanceRiza JauferPas encore d'évaluation

- Business LetterDocument17 pagesBusiness Letterharish chandraPas encore d'évaluation

- A Research Project Report: ON Human Resource Management SystemDocument78 pagesA Research Project Report: ON Human Resource Management Systemharish chandraPas encore d'évaluation

- Consumer BehaviourDocument1 pageConsumer Behaviourharish chandraPas encore d'évaluation

- Environment in Human Resource ManagementDocument2 pagesEnvironment in Human Resource Managementharish chandraPas encore d'évaluation

- Industrial Relation 1Document6 pagesIndustrial Relation 1harish chandraPas encore d'évaluation

- Business LetterDocument2 pagesBusiness Letterharish chandraPas encore d'évaluation

- Business LetterDocument2 pagesBusiness Letterharish chandraPas encore d'évaluation

- Sandeep Kumar SharmaDocument2 pagesSandeep Kumar Sharmaharish chandraPas encore d'évaluation

- MCA Notes 1 UnitDocument5 pagesMCA Notes 1 Unitharish chandraPas encore d'évaluation

- Organization DesignDocument5 pagesOrganization Designharish chandraPas encore d'évaluation

- Business LetterDocument17 pagesBusiness Letterharish chandraPas encore d'évaluation

- Financial Derivatives 260214Document347 pagesFinancial Derivatives 260214akshay mourya100% (1)

- Accounting TerminologyDocument8 pagesAccounting Terminologyharish chandraPas encore d'évaluation

- Compiled By-Harish Chandra MauryaDocument15 pagesCompiled By-Harish Chandra Mauryaharish chandraPas encore d'évaluation

- Salary Structure-Ctr 856Document5 pagesSalary Structure-Ctr 856Manish BoliaPas encore d'évaluation

- Presented By-Harish Chandra MauryaDocument12 pagesPresented By-Harish Chandra Mauryaharish chandraPas encore d'évaluation

- Covered Interest Rate ParityDocument4 pagesCovered Interest Rate Parityrani0326Pas encore d'évaluation

- Laabh BookletDocument33 pagesLaabh BookletSri RamPas encore d'évaluation

- Econ 101 Cheat Sheet (FInal)Document1 pageEcon 101 Cheat Sheet (FInal)Alex MadarangPas encore d'évaluation

- State Pension: Your Notes BookletDocument28 pagesState Pension: Your Notes BookletArup MitraPas encore d'évaluation

- Pivot Boss SummaryDocument36 pagesPivot Boss SummaryVarun Vasurendran100% (2)

- BCG Growth-Share MatrixDocument3 pagesBCG Growth-Share Matrixabhishek kunalPas encore d'évaluation

- Directional Options TradingDocument24 pagesDirectional Options Tradingmaoychris0% (1)

- Lembar Jawaban 2-BUKU BESARDocument13 pagesLembar Jawaban 2-BUKU BESAREnrico Jovian S SPas encore d'évaluation

- Topic 7 - Forecasting Financial Statements (Updated)Document64 pagesTopic 7 - Forecasting Financial Statements (Updated)Jasmine JacksonPas encore d'évaluation

- Goa University International Economics Sem V SyllabusDocument3 pagesGoa University International Economics Sem V SyllabusMyron VazPas encore d'évaluation

- Chapter 4: Analysis of Financial StatementsDocument50 pagesChapter 4: Analysis of Financial StatementsHope Trinity EnriquezPas encore d'évaluation

- Financial Institution & Investment Management - Final ExamDocument5 pagesFinancial Institution & Investment Management - Final Exambereket nigussie100% (4)

- Rythu Bandhu Group Life Insurance Scheme Form 971Document5 pagesRythu Bandhu Group Life Insurance Scheme Form 971CHETTI SAGARPas encore d'évaluation

- Mod 4.2Document27 pagesMod 4.2NitishPas encore d'évaluation

- DD MFR FinalDocument105 pagesDD MFR Finalbig johnPas encore d'évaluation

- Motor Vehicle InsuranceDocument6 pagesMotor Vehicle InsuranceArunKumarPas encore d'évaluation

- Creating Value Beyond The Deal: Financial Services: Maximise Success by Keeping An Intense Focus On Three Key ElementsDocument24 pagesCreating Value Beyond The Deal: Financial Services: Maximise Success by Keeping An Intense Focus On Three Key ElementsNick HuPas encore d'évaluation

- Far: Property, Plant, and Equipment: I. Definition and NatureDocument13 pagesFar: Property, Plant, and Equipment: I. Definition and NatureAl ChuaPas encore d'évaluation

- COGM5 Final RequirementDocument24 pagesCOGM5 Final RequirementLadignon IvyPas encore d'évaluation

- In The Partial Fulfillment of The Requirement For The Award of Degree inDocument17 pagesIn The Partial Fulfillment of The Requirement For The Award of Degree inMohmmedKhayyumPas encore d'évaluation

- Financial ManagementDocument11 pagesFinancial ManagementRuel VillanuevaPas encore d'évaluation

- Chapter 11 - Part 1 - Accounting FranchisesDocument13 pagesChapter 11 - Part 1 - Accounting FranchisesJane Dizon100% (1)

- AIG Global Funds ProspectusDocument257 pagesAIG Global Funds ProspectusserebryakovPas encore d'évaluation

- Pi ECO Vietnam Project Abstract & Summary 7 March 2019Document11 pagesPi ECO Vietnam Project Abstract & Summary 7 March 2019ICT Bảo HànhPas encore d'évaluation

- Day1 10daysaccountingchallengeDocument16 pagesDay1 10daysaccountingchallengeSeungyun ChoPas encore d'évaluation

- Format Laporan Petty CashDocument8 pagesFormat Laporan Petty CashIchalz NtsPas encore d'évaluation

- Clause 49 of Listing AgreementDocument18 pagesClause 49 of Listing AgreementJatin AhujaPas encore d'évaluation

- Unit II Methods of Valuing Material IssuesDocument21 pagesUnit II Methods of Valuing Material IssuesLeemaRosaline Simon0% (1)

- Average Age of InventoryDocument10 pagesAverage Age of Inventoryrakeshjha91Pas encore d'évaluation

- V. Commissioner of Internal Revenue, RespondentDocument3 pagesV. Commissioner of Internal Revenue, RespondentJenifferRimandoPas encore d'évaluation