Vous aimerez peut-être aussi

- Conrail ADocument4 pagesConrail ARaman Gupta100% (1)

- Conrail Analysis BDocument7 pagesConrail Analysis BRahul Garg50% (2)

- Conrail & CSXDocument6 pagesConrail & CSXAditya VermaPas encore d'évaluation

- The Acquisition of Conrail CorporationDocument7 pagesThe Acquisition of Conrail CorporationA.r. Pirzado100% (1)

- Conrail 2Document5 pagesConrail 2AEKaidarov100% (1)

- Conrail-CSX Case2Document5 pagesConrail-CSX Case2Anastasia_Nauc_1679100% (2)

- Assignment ConrailDocument2 pagesAssignment Conrailhim009Pas encore d'évaluation

- Conrail Case Solution - Group 8Document9 pagesConrail Case Solution - Group 8Arun Maithani100% (2)

- Conrail Case Solution Group 4Document8 pagesConrail Case Solution Group 4AnandPas encore d'évaluation

- Case Submission: Conrail A Group H8 FINA608Document6 pagesCase Submission: Conrail A Group H8 FINA608Nitin KhandelwalPas encore d'évaluation

- Case Submission: Conrail B Group H8 FINA608Document4 pagesCase Submission: Conrail B Group H8 FINA608Nitin KhandelwalPas encore d'évaluation

- Conrail Case QuestionsDocument1 pageConrail Case QuestionsPiraterija100% (1)

- Case 5 - Conrail A&B (Questions)Document1 pageCase 5 - Conrail A&B (Questions)syeda alinaPas encore d'évaluation

- Acquisition of Conrail Corp. by CSX Corp.: M&A AssignmentDocument10 pagesAcquisition of Conrail Corp. by CSX Corp.: M&A Assignmentkoundi_350% (2)

- CSX - Conrail - Group 13Document10 pagesCSX - Conrail - Group 13Saquib HasnainPas encore d'évaluation

- M&A 2013 Conrail Two Tier Offer CaseDocument4 pagesM&A 2013 Conrail Two Tier Offer CaseJanni BannyPas encore d'évaluation

- ConRail-B Case QuestionsDocument1 pageConRail-B Case Questionsrahul84803Pas encore d'évaluation

- ConrailM&a Group7Document15 pagesConrailM&a Group7Saquib HasnainPas encore d'évaluation

- Con RailDocument9 pagesCon RailMario A. BetancurPas encore d'évaluation

- Case ADocument7 pagesCase A徐楷筑Pas encore d'évaluation

- Conrail Valuation MultiplesDocument8 pagesConrail Valuation MultiplesabhishekPas encore d'évaluation

- KOHLR &co (A&B) : Asish K Bhattacharyya Chairperson, Riverside Management Academy Private LimitedDocument30 pagesKOHLR &co (A&B) : Asish K Bhattacharyya Chairperson, Riverside Management Academy Private LimitedmanjeetsrccPas encore d'évaluation

- USX (Questions)Document2 pagesUSX (Questions)DavidBudinas0% (3)

- USX Corporation and Associated Teaching NoteDocument24 pagesUSX Corporation and Associated Teaching Noteolegipod50530% (1)

- Acquisition Wars: Prof. Ian GiddyDocument30 pagesAcquisition Wars: Prof. Ian GiddyJunaid RazzaqPas encore d'évaluation

- Acquisition of Consolidated Rail CorporationDocument12 pagesAcquisition of Consolidated Rail CorporationEdithPas encore d'évaluation

- Why Is CSX Interested in Acquiring Consolidated Rail CorporationDocument6 pagesWhy Is CSX Interested in Acquiring Consolidated Rail CorporationTarun Madan0% (2)

- Case Studies On Cooper Industries IncDocument12 pagesCase Studies On Cooper Industries Inc黃靖順75% (4)

- Acquisition of Consolidated Rail Corp. (A)Document1 pageAcquisition of Consolidated Rail Corp. (A)Mike MC0% (1)

- Kohler Case Leo Final DraftDocument16 pagesKohler Case Leo Final DraftLeo Ng Shee Zher67% (3)

- The Acquisition of Consolidated Rail Corporation (A)Document15 pagesThe Acquisition of Consolidated Rail Corporation (A)tuhin14078Pas encore d'évaluation

- Assignment For MCIDocument3 pagesAssignment For MCIkashanr82100% (1)

- The MCI Takeover BattleDocument17 pagesThe MCI Takeover BattleLucas Tai100% (1)

- Submission2 - General Mills Acquisition of PillsburyDocument10 pagesSubmission2 - General Mills Acquisition of PillsburyAryan AnandPas encore d'évaluation

- Cooper Industries CaseDocument3 pagesCooper Industries CaseGeorge LamPas encore d'évaluation

- Linear TechnologyDocument6 pagesLinear Technologyprashantkumarsinha007100% (1)

- Submitted To: Submitted By: Dr. Kulbir Singh Vinay Singh 201922106 Aurva Bhardwaj 201922066 Deepanshu Gupta 201922069 Sameer Kumbhalwar 201922097Document3 pagesSubmitted To: Submitted By: Dr. Kulbir Singh Vinay Singh 201922106 Aurva Bhardwaj 201922066 Deepanshu Gupta 201922069 Sameer Kumbhalwar 201922097Aurva BhardwajPas encore d'évaluation

- Uttam Kumar Sec-A Dividend Policy Linear TechnologyDocument11 pagesUttam Kumar Sec-A Dividend Policy Linear TechnologyUttam Kumar100% (1)

- Sealed Air Corporation's Leveraged Recapitalization - RichaDocument3 pagesSealed Air Corporation's Leveraged Recapitalization - Richanishant kumarPas encore d'évaluation

- Case 13 - Corning - Questions111Document5 pagesCase 13 - Corning - Questions111timbulmanaluPas encore d'évaluation

- Facebook, Inc: The Initial Public OfferingDocument5 pagesFacebook, Inc: The Initial Public OfferingHanako Taniguchi PoncianoPas encore d'évaluation

- Individual AssignmentDocument10 pagesIndividual Assignmentparitosh nayakPas encore d'évaluation

- Dividend Policy Analysis Florida Power LightDocument5 pagesDividend Policy Analysis Florida Power LightShilpi Kumari100% (1)

- MCI Communications CorporationDocument6 pagesMCI Communications Corporationnipun9143Pas encore d'évaluation

- Kohler DCF Control Prem and DiscDocument6 pagesKohler DCF Control Prem and Discapi-239586293Pas encore d'évaluation

- Dividend Policy at Linear TechnologyDocument9 pagesDividend Policy at Linear TechnologySAHILPas encore d'évaluation

- Session-11 - Venture Capital Valuation Problem SetDocument2 pagesSession-11 - Venture Capital Valuation Problem SetSaurabh SinghPas encore d'évaluation

- Sealed Air Case StudyDocument8 pagesSealed Air Case StudyDo Ngoc Chau100% (4)

- Muddasir Noor Canadian Pacific Bid Case Analysis PDFDocument13 pagesMuddasir Noor Canadian Pacific Bid Case Analysis PDFAshish Gondane50% (2)

- General Mills Pillsbury Case - MACRDocument7 pagesGeneral Mills Pillsbury Case - MACRNikita GulgulePas encore d'évaluation

- Cooper Industries - Group 5Document11 pagesCooper Industries - Group 5Rudro MukherjeePas encore d'évaluation

- Blaine Kitchenware Case Study SolutionDocument5 pagesBlaine Kitchenware Case Study SolutionFarhanie Nordin100% (2)

- Mci Takeover Battle AnalysisDocument13 pagesMci Takeover Battle AnalysisAastha Swaroop50% (2)

- Session 9 Case Discussion Immulogic Pharmaceutical CorporationDocument32 pagesSession 9 Case Discussion Immulogic Pharmaceutical CorporationK RameshPas encore d'évaluation

- Sealed Air Co Case Study Queestions Why Did Sealed Air Undertake A LeveragDocument9 pagesSealed Air Co Case Study Queestions Why Did Sealed Air Undertake A Leveragvichenyu100% (1)

- Linear Technology Payout Policy Case 3Document4 pagesLinear Technology Payout Policy Case 3Amrinder SinghPas encore d'évaluation

- PDFFile5b28cbad75db10 11058940Document4 pagesPDFFile5b28cbad75db10 11058940Kurapati VenkatkrishnaPas encore d'évaluation

- MergersDocument4 pagesMergersNishant BiswalPas encore d'évaluation

- Futures Contracts Amended 09 Sep 05 Managem, EntDocument5 pagesFutures Contracts Amended 09 Sep 05 Managem, Entfarid401Pas encore d'évaluation

- The Acquisition of Consolidated Rail Corporation: Browse Essays BusinessDocument6 pagesThe Acquisition of Consolidated Rail Corporation: Browse Essays BusinessJun Wei LowPas encore d'évaluation

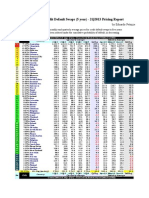

- Sovereign Credit Default Swaps (5 Year) - 2Q2013 Pricing ReportDocument1 pageSovereign Credit Default Swaps (5 Year) - 2Q2013 Pricing ReportEduardo PetazzePas encore d'évaluation

- Iim BDocument2 pagesIim BDhruv JainPas encore d'évaluation

- ABM PRINCIPLES OF MARKETING 11 - Q1 - W2 - Mod2Document10 pagesABM PRINCIPLES OF MARKETING 11 - Q1 - W2 - Mod2Alex M. PinoPas encore d'évaluation

- BrandingDocument28 pagesBrandingTejal PatilPas encore d'évaluation

- Business Finance All Lecture Notes 1 10Document143 pagesBusiness Finance All Lecture Notes 1 10sirkoywayo6628Pas encore d'évaluation

- Reflection-Paper Chapter 13 Direct Foreign InvestmentDocument1 pageReflection-Paper Chapter 13 Direct Foreign InvestmentJouhara G. San JuanPas encore d'évaluation

- Draw On Liquidity: Visual Guide by HansonDocument20 pagesDraw On Liquidity: Visual Guide by HansonNabeel Sarwar100% (3)

- Fundamentals of Financial Accounting 6th Edition Phillips Test BankDocument16 pagesFundamentals of Financial Accounting 6th Edition Phillips Test Bankjeanbarnettxv9v100% (13)

- Cfa 1Document16 pagesCfa 1Beatriz DiasPas encore d'évaluation

- Financial Accounting With International Financial Reporting Standards 4th Edition Weygandt Solutions ManualDocument43 pagesFinancial Accounting With International Financial Reporting Standards 4th Edition Weygandt Solutions Manualcanellacitrinec0kkb100% (31)

- Markowitz in Tactical Asset AllocationDocument12 pagesMarkowitz in Tactical Asset AllocationsoumensahilPas encore d'évaluation

- 11th Accounts Full Test MVPDocument17 pages11th Accounts Full Test MVPnandiniladdha16Pas encore d'évaluation

- Calls in AdvanceDocument14 pagesCalls in AdvanceShruti GoswamiPas encore d'évaluation

- CHAPTER 1 Bike Rental Business PlanDocument3 pagesCHAPTER 1 Bike Rental Business PlanLishaEli100% (1)

- Yogesh Hs ReportDocument43 pagesYogesh Hs ReportMohammed WasimPas encore d'évaluation

- KCP Capital BudgetingDocument98 pagesKCP Capital BudgetingVamsi SakhamuriPas encore d'évaluation

- Results Reporter: Multiple Choice QuizDocument2 pagesResults Reporter: Multiple Choice QuizBinod ThakurPas encore d'évaluation

- Assignment - DRM Given By: Mr. N P Singh: 1. Interest Rate SwapDocument3 pagesAssignment - DRM Given By: Mr. N P Singh: 1. Interest Rate SwapSahil MittalPas encore d'évaluation

- Financial Accounting An Introduction To Concepts Methods and Uses Weil 14th Edition Solutions ManualDocument24 pagesFinancial Accounting An Introduction To Concepts Methods and Uses Weil 14th Edition Solutions Manualstubbleubiquistu1nPas encore d'évaluation

- Admission of A Partner With AnswersDocument20 pagesAdmission of A Partner With AnswersAaira IbrahimPas encore d'évaluation

- Toolbox CRDV CRRIIDocument60 pagesToolbox CRDV CRRIINasim AkhtarPas encore d'évaluation

- Tata Motors ValuationDocument38 pagesTata Motors ValuationAkshat JainPas encore d'évaluation

- Best Practices: For TheDocument67 pagesBest Practices: For TheltfreedPas encore d'évaluation

- Commodity Derivatives and Risk Management - AssessmentDocument4 pagesCommodity Derivatives and Risk Management - AssessmentLokesh manglaPas encore d'évaluation

- Accounting Assignment & CATDocument14 pagesAccounting Assignment & CATMargaret IrunguPas encore d'évaluation

- FM-Sessions 23 - 24 Dividend Policy-CompleteDocument72 pagesFM-Sessions 23 - 24 Dividend Policy-CompleteSaadat ShaikhPas encore d'évaluation

- Techinical AnalysisDocument14 pagesTechinical AnalysisCamille BagadiongPas encore d'évaluation

- The Financial Statements: Chapter OutlineDocument15 pagesThe Financial Statements: Chapter OutlineBhagaban DasPas encore d'évaluation

- Charlie McElligott Chart Book January 2019Document25 pagesCharlie McElligott Chart Book January 2019kyriejohannesPas encore d'évaluation

- LK TPM 31 Des 2022Document81 pagesLK TPM 31 Des 2022Jefri Formen PangaribuanPas encore d'évaluation