Vous aimerez peut-être aussi

- USREITs REITs 101 - An IntroductionDocument89 pagesUSREITs REITs 101 - An Introductiong4nz0Pas encore d'évaluation

- Garbis - Tranquility at Fredericktown A Value Add Investment Proposition - 2009 - RosenbergDocument99 pagesGarbis - Tranquility at Fredericktown A Value Add Investment Proposition - 2009 - Rosenbergg4nz0Pas encore d'évaluation

- Sample Business Plan - Real Estate DevelopmentDocument78 pagesSample Business Plan - Real Estate Developmentg4nz094% (18)

- Graham and Doddsville Winter 2012Document52 pagesGraham and Doddsville Winter 2012waterhousebPas encore d'évaluation

- Graham & Doddsville 20091009Document29 pagesGraham & Doddsville 20091009wrolosonPas encore d'évaluation

- Graham & Doddsville: - Larry RobbinsDocument54 pagesGraham & Doddsville: - Larry RobbinsSaurabh DasPas encore d'évaluation

- Graham and Doddsville Newsletter Fall 2010Document35 pagesGraham and Doddsville Newsletter Fall 2010Jean-Marie TruellePas encore d'évaluation

- 2012-2014-Real Estate Land Bus PlanDocument55 pages2012-2014-Real Estate Land Bus Plang4nz0Pas encore d'évaluation

- Graham & Doddsville - Issue 15 - Spring 2012Document64 pagesGraham & Doddsville - Issue 15 - Spring 2012bijuePas encore d'évaluation

- Graham and Doddsville - Issue 13 - Fall 2011Document34 pagesGraham and Doddsville - Issue 13 - Fall 2011g4nz0Pas encore d'évaluation

- Graham and Doddsville - Issue 6 - Summer 2009Document37 pagesGraham and Doddsville - Issue 6 - Summer 2009g4nz0Pas encore d'évaluation

- Graham and Doddsville - Issue 5 Winter 2009Document35 pagesGraham and Doddsville - Issue 5 Winter 2009tatsrus1Pas encore d'évaluation

- Graham and Doddsville - Issue 12 - Spring 2011Document27 pagesGraham and Doddsville - Issue 12 - Spring 2011g4nz0Pas encore d'évaluation

- Graham and Doddsville - Issue 8 Winter 2010Document35 pagesGraham and Doddsville - Issue 8 Winter 2010tatsrus1Pas encore d'évaluation

- Graham and Doddsville - Issue 9 - Spring 2010Document33 pagesGraham and Doddsville - Issue 9 - Spring 2010g4nz0Pas encore d'évaluation

- Graham and Doddsville - Issue 3 - Winter 2007Document23 pagesGraham and Doddsville - Issue 3 - Winter 2007g4nz0Pas encore d'évaluation

- Graham and Doddsville - Issue 1 - Winter 2006Document22 pagesGraham and Doddsville - Issue 1 - Winter 2006David KesslerPas encore d'évaluation

- Monish PabraiDocument22 pagesMonish PabraiDavid SobkowiczPas encore d'évaluation

- Graham and Doddsville - Issue 2 - Summer 2007Document22 pagesGraham and Doddsville - Issue 2 - Summer 2007g4nz0Pas encore d'évaluation

- ModulosDocument7 pagesModulosg4nz0Pas encore d'évaluation

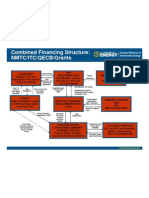

- Solar NMTC StructureDocument1 pageSolar NMTC Structureg4nz0Pas encore d'évaluation

- Selected Treasury 1603 Grant MaterialsDocument133 pagesSelected Treasury 1603 Grant Materialsg4nz0Pas encore d'évaluation

- Act 82 Energy Diversification ActDocument22 pagesAct 82 Energy Diversification Actg4nz0Pas encore d'évaluation

- InversoresDocument2 pagesInversoresg4nz0Pas encore d'évaluation

- Wind Energy FormsDocument5 pagesWind Energy Formsg4nz0Pas encore d'évaluation

- Building Energy Efficiency Retrofit FormsDocument5 pagesBuilding Energy Efficiency Retrofit Formsg4nz0Pas encore d'évaluation

- Act 83 of 2010 Renewable Incentives Bill Oficial EnglishDocument77 pagesAct 83 of 2010 Renewable Incentives Bill Oficial Englishg4nz0Pas encore d'évaluation

- Gold vs. Model: Date Ibbotson Real R 2% Deflatoadjusted F Inversion Leverage Model GoldDocument6 pagesGold vs. Model: Date Ibbotson Real R 2% Deflatoadjusted F Inversion Leverage Model Goldg4nz0Pas encore d'évaluation

- Sun Energy FormsDocument4 pagesSun Energy Formsg4nz0Pas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5782)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Photovoltaic Plant and BESS IntegrationDocument109 pagesPhotovoltaic Plant and BESS IntegrationHaoyi ChaiPas encore d'évaluation

- Journal of Applied Corporate Finance 2019 PE 4.0Document10 pagesJournal of Applied Corporate Finance 2019 PE 4.0Herleif HaavikPas encore d'évaluation

- 2Document411 pages2Balachandran Siddharthan SPas encore d'évaluation

- China Datang CorporationDocument262 pagesChina Datang CorporationmustaminPas encore d'évaluation

- Approval for 500Wp Solar Installation at Khatyad Khola Mini Hydro ProjectDocument4 pagesApproval for 500Wp Solar Installation at Khatyad Khola Mini Hydro ProjectRajan BhandariPas encore d'évaluation

- Accepted Manuscript: Renewable EnergyDocument38 pagesAccepted Manuscript: Renewable EnergyPrivatePas encore d'évaluation

- City Council AgendaDocument94 pagesCity Council AgendasebastienperthPas encore d'évaluation

- Photovoltaic-Thermal (PV/T) Hybrid Systems: State-Of-The-Art Technology, Challenges and OpportunitiesDocument46 pagesPhotovoltaic-Thermal (PV/T) Hybrid Systems: State-Of-The-Art Technology, Challenges and Opportunitiesroxana grigorePas encore d'évaluation

- Reinventing Energy FuturesDocument6 pagesReinventing Energy FuturesSean NessPas encore d'évaluation

- Grid Connected Rooftop Solar System PDFDocument28 pagesGrid Connected Rooftop Solar System PDFdebasisdgPas encore d'évaluation

- JGC Company Profile eDocument14 pagesJGC Company Profile eDAC ORGANIZERPas encore d'évaluation

- 5 Day Masterclass in Renewable Energy Modelling Terrapinn TrainingDocument6 pages5 Day Masterclass in Renewable Energy Modelling Terrapinn TrainingMohammed Al MandhariPas encore d'évaluation

- The Performance of KPK Govt in Power Sector in 5 YearsDocument6 pagesThe Performance of KPK Govt in Power Sector in 5 YearsInsaf.PKPas encore d'évaluation

- MESTEEDocument45 pagesMESTEEProject AnalysisPas encore d'évaluation

- LNG Journal Oct21 - CompressedDocument44 pagesLNG Journal Oct21 - CompressedKarima BelbraikPas encore d'évaluation

- Mail Approval Copy - Electricity LT Bills Feb 2024Document5 pagesMail Approval Copy - Electricity LT Bills Feb 2024Sheik SamdhaniPas encore d'évaluation

- Energy Booklet Y4Document84 pagesEnergy Booklet Y4Pima Ajah33% (3)

- Solar Energy Potential and Uses in Nigerian AgricultureDocument12 pagesSolar Energy Potential and Uses in Nigerian AgricultureChigbundu EmeruwaPas encore d'évaluation

- Solar Resource Mapping and PV Potential in MyanmarDocument8 pagesSolar Resource Mapping and PV Potential in Myanmarsalem BEN MOUSSA100% (1)

- Its The Architecture StupidDocument4 pagesIts The Architecture StupidNay ReyesPas encore d'évaluation

- Escp Emib-Mtp JP MareeDocument108 pagesEscp Emib-Mtp JP Mareephillip.mareePas encore d'évaluation

- Ieto - 2021 - IesrDocument93 pagesIeto - 2021 - IesrWatch MePas encore d'évaluation

- THE CAREER GUIDE Green JobsDocument24 pagesTHE CAREER GUIDE Green Jobsamila_vithanagePas encore d'évaluation

- Advantages and Disadvantages of Energy SourcesDocument9 pagesAdvantages and Disadvantages of Energy SourcesJulio CortezPas encore d'évaluation

- Feasible Alternatives To Green GrowthDocument7 pagesFeasible Alternatives To Green GrowthPeter DazsPas encore d'évaluation

- Energy MixDocument10 pagesEnergy MixPara DisePas encore d'évaluation

- The Effective of Geothermal Energy in BuDocument8 pagesThe Effective of Geothermal Energy in BuMeziane YkhlefPas encore d'évaluation

- MASTET Scholarships for African Students in Energy ProgramsDocument1 pageMASTET Scholarships for African Students in Energy ProgramsALAKOUKOPas encore d'évaluation

- Offshore Wind, Port Services & Logistics - Esbjerg PortDocument16 pagesOffshore Wind, Port Services & Logistics - Esbjerg PortAlex LiuPas encore d'évaluation

- WBCSD Corporate Renewable PPAs-in India-Market and Policy Update PDFDocument26 pagesWBCSD Corporate Renewable PPAs-in India-Market and Policy Update PDFKIRAN DASIPas encore d'évaluation