Vous aimerez peut-être aussi

- Landlord Tax Planning StrategiesD'EverandLandlord Tax Planning StrategiesPas encore d'évaluation

- Business Tax ReviewerDocument22 pagesBusiness Tax ReviewereysiPas encore d'évaluation

- RR 14-08 DigestDocument2 pagesRR 14-08 DigestPat PatPas encore d'évaluation

- Taxpayer's checklist for TRAIN law changesDocument6 pagesTaxpayer's checklist for TRAIN law changesChrislynPas encore d'évaluation

- Pre-Week Notes On Vat: Prepared by Dr. Jeannie P. LimDocument11 pagesPre-Week Notes On Vat: Prepared by Dr. Jeannie P. LimMark MagnoPas encore d'évaluation

- 3 Income Tax ConceptsDocument37 pages3 Income Tax ConceptsRommel Espinocilla Jr.Pas encore d'évaluation

- Module Part 2 - Business Taxation Dec. 14Document60 pagesModule Part 2 - Business Taxation Dec. 14Maybelyn PaalaPas encore d'évaluation

- How to Compute VAT Payable in the PhilippinesDocument5 pagesHow to Compute VAT Payable in the PhilippinesTere Ypil100% (1)

- Philippines - Income Tax: Tax Returns and ComplianceDocument11 pagesPhilippines - Income Tax: Tax Returns and ComplianceUnknown NamePas encore d'évaluation

- Bir TaxDocument157 pagesBir TaxMubarrach MatabalaoPas encore d'évaluation

- RR No. 11-2018 SummaryDocument6 pagesRR No. 11-2018 SummaryCaliPas encore d'évaluation

- Percentage TaxDocument5 pagesPercentage TaxGIGI BODOPas encore d'évaluation

- 55153rr10 17Document2 pages55153rr10 17fatmaaleahPas encore d'évaluation

- Republic Act No. 10963: Tax Reform For Acceleration and Inclusion (Train)Document24 pagesRepublic Act No. 10963: Tax Reform For Acceleration and Inclusion (Train)Johayra AbbasPas encore d'évaluation

- 2 Value Added TaxDocument216 pages2 Value Added TaxnichPas encore d'évaluation

- TRAIN Law - Diaz Murillo Dalupan and CompanyDocument215 pagesTRAIN Law - Diaz Murillo Dalupan and CompanyBien Bowie A. Cortez100% (1)

- BIR Tax Briefing - RR 11-2018Document3 pagesBIR Tax Briefing - RR 11-2018Jeff BulasaPas encore d'évaluation

- Faqs Withholding TaxDocument50 pagesFaqs Withholding TaxHarryPas encore d'évaluation

- Corporation As A TaxpayerDocument27 pagesCorporation As A TaxpayerBSA-2C John Dominic Mia100% (1)

- Axsdaqgasdgasdg 123123 Aeasdfw SadgDocument6 pagesAxsdaqgasdgasdg 123123 Aeasdfw SadgMark LimPas encore d'évaluation

- Tax Reform For Acceleration and Inclusion LawDocument28 pagesTax Reform For Acceleration and Inclusion LawGloriosa SzePas encore d'évaluation

- Tax-on-Individuals PhilippinesDocument21 pagesTax-on-Individuals PhilippinesMaria Regina Javier100% (2)

- Taxation Report Vina MarieDocument12 pagesTaxation Report Vina MarieAnonymous gmDxRbnwOPas encore d'évaluation

- Taxes On Commercial LeaseDocument8 pagesTaxes On Commercial Leasebelbel08Pas encore d'évaluation

- Frequently Asked Questions On VatDocument9 pagesFrequently Asked Questions On VatSteve SantillanPas encore d'évaluation

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Document33 pagesReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB CloydPas encore d'évaluation

- 3.2 Business Profit TaxDocument49 pages3.2 Business Profit TaxBizu AtnafuPas encore d'évaluation

- Final TaxDocument26 pagesFinal TaxMarie MendozaPas encore d'évaluation

- A Guide To Taxation in The PhilippinesDocument5 pagesA Guide To Taxation in The PhilippinesNathaniel MartinezPas encore d'évaluation

- Income TaxationDocument3 pagesIncome Taxationm.bagnas.488669Pas encore d'évaluation

- Percentage Tax Who Are Required To File?Document4 pagesPercentage Tax Who Are Required To File?Angelyn SamandePas encore d'évaluation

- Business TaxationDocument33 pagesBusiness Taxationrose querubinPas encore d'évaluation

- Value Added TaxDocument44 pagesValue Added TaxDa Yani ChristeenePas encore d'évaluation

- RMC No 51-2008Document7 pagesRMC No 51-2008Yasser MangadangPas encore d'évaluation

- Bir TaxDocument97 pagesBir TaxVincent De VeraPas encore d'évaluation

- VAT Concepts Tax 321Document28 pagesVAT Concepts Tax 321justinePas encore d'évaluation

- Vat PDFDocument28 pagesVat PDFJovelyn Villasenor33% (3)

- Quarterly Percentage Tax Rates TableDocument8 pagesQuarterly Percentage Tax Rates TableAngelyn SamandePas encore d'évaluation

- Excel Professional Services, Inc.: Management Firm of Professional Review and Training Center (PRTC)Document3 pagesExcel Professional Services, Inc.: Management Firm of Professional Review and Training Center (PRTC)Mae Angiela TansecoPas encore d'évaluation

- IndividualDocument14 pagesIndividualKenneth Bryan Tegerero TegioPas encore d'évaluation

- Notes in Tax On IndividualsDocument4 pagesNotes in Tax On IndividualsPaula BatulanPas encore d'évaluation

- Importance of Withholding Tax SystemDocument7 pagesImportance of Withholding Tax SystemALAJID, KIM EMMANUELPas encore d'évaluation

- Creditable Withholding Tax ReviewerDocument6 pagesCreditable Withholding Tax ReviewerMark Rainer Yongis LozaresPas encore d'évaluation

- VAT-ADDED TAXDocument22 pagesVAT-ADDED TAXDiossaPas encore d'évaluation

- Withholding Tax: Taxation LawDocument21 pagesWithholding Tax: Taxation LawB-an JavelosaPas encore d'évaluation

- Classification of Taxes: A. Domestic CorporationDocument5 pagesClassification of Taxes: A. Domestic CorporationWenjunPas encore d'évaluation

- Large Taxpayers Regulations on Filing & Payment DatesDocument3 pagesLarge Taxpayers Regulations on Filing & Payment DatesLady Ann CayananPas encore d'évaluation

- 2019 BAR Exam Tax Supplement by R.G. Manabat & CoDocument48 pages2019 BAR Exam Tax Supplement by R.G. Manabat & CoQueenie VallePas encore d'évaluation

- Digest RR 14-2018Document1 pageDigest RR 14-2018Carlota Nicolas VillaromanPas encore d'évaluation

- Business-Tax VAT FAQsDocument11 pagesBusiness-Tax VAT FAQsBryan VidalPas encore d'évaluation

- Module 4 - Value Added TaxDocument16 pagesModule 4 - Value Added Taxanon_455551365Pas encore d'évaluation

- Belmonte TAX Quiz. WITH PART 1docxDocument11 pagesBelmonte TAX Quiz. WITH PART 1docxRheyne Robledo-MendozaPas encore d'évaluation

- Frequently Asked QuestionsDocument40 pagesFrequently Asked Questionsroy rebosuraPas encore d'évaluation

- Gross IncomeDocument68 pagesGross IncomeNour Aira NaoPas encore d'évaluation

- New Tax ReformDocument4 pagesNew Tax ReformEDISON SAGUIRERPas encore d'évaluation

- TRAIN LAW Comparative AnalysisDocument2 pagesTRAIN LAW Comparative AnalysisElaine100% (3)

- Taxation Value-Added-TAX ExplainedDocument21 pagesTaxation Value-Added-TAX ExplainediBEAYPas encore d'évaluation

- Frequency of ReportingDocument5 pagesFrequency of ReportingNeriza maningasPas encore d'évaluation

- Taxation 1 Lesson 1. Returns and Payment of TaxDocument42 pagesTaxation 1 Lesson 1. Returns and Payment of TaxHarui Hani-31Pas encore d'évaluation

- Types: Fringe Benefit Vincent Ryan T. Esteves, Bsa-2Document1 pageTypes: Fringe Benefit Vincent Ryan T. Esteves, Bsa-2Lhorene Hope DueñasPas encore d'évaluation

- Statement of Axis Account No:917010040330266 For The Period (From: 09-06-2021 To: 08-09-2021)Document13 pagesStatement of Axis Account No:917010040330266 For The Period (From: 09-06-2021 To: 08-09-2021)Saurabh DandriyalPas encore d'évaluation

- Cheque Book Request LetterDocument1 pageCheque Book Request LetterMadhu SudananPas encore d'évaluation

- N28 TU2 Yljhuo PV 7 GDocument15 pagesN28 TU2 Yljhuo PV 7 GVishal BawanePas encore d'évaluation

- Payment Advice DetailsDocument2 pagesPayment Advice DetailsVishal KamblePas encore d'évaluation

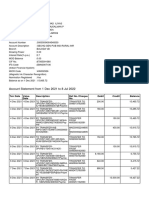

- Account Statement From 1 Dec 2021 To 8 Jul 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument15 pagesAccount Statement From 1 Dec 2021 To 8 Jul 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceVIVEK CHAUHANPas encore d'évaluation

- Individual Customer Relation Form: ApplicationDocument7 pagesIndividual Customer Relation Form: ApplicationJay JaniPas encore d'évaluation

- Einvoice 1661931542084Document1 pageEinvoice 1661931542084Jessica MathisPas encore d'évaluation

- A Practical Guide To GST - Adv. Sanjay Dwivedi (2017 Edition)Document435 pagesA Practical Guide To GST - Adv. Sanjay Dwivedi (2017 Edition)Sanjay DwivediPas encore d'évaluation

- Invoice No. 398484: Endor AGDocument1 pageInvoice No. 398484: Endor AGLamesHunterPas encore d'évaluation

- Case1 SecC GroupJDocument7 pagesCase1 SecC GroupJNimish JoshiPas encore d'évaluation

- Quantity Description Category Weight (LB) Length (CM) Width (CM) Height (CM) Weight Vol. (LB)Document1 pageQuantity Description Category Weight (LB) Length (CM) Width (CM) Height (CM) Weight Vol. (LB)Ardiyansyah NugrahaPas encore d'évaluation

- MIIA vs. Court of Appeals GR No. 155650Document2 pagesMIIA vs. Court of Appeals GR No. 155650ClarickJoshuaVijandrePas encore d'évaluation

- A1C019011 - Alifia Aprizila Putri - Tugas AKL.Document5 pagesA1C019011 - Alifia Aprizila Putri - Tugas AKL.Alifia AprizilaPas encore d'évaluation

- Evolution of the Philippine Tax Collection SystemDocument12 pagesEvolution of the Philippine Tax Collection SystemViAnne Reyes50% (2)

- BRIÑEZDocument2 pagesBRIÑEZMundo RealPas encore d'évaluation

- First Data Annual Report 2011Document178 pagesFirst Data Annual Report 2011SteveMastersPas encore d'évaluation

- SAP GST Configuration 1627828736Document31 pagesSAP GST Configuration 1627828736Parvati sbPas encore d'évaluation

- Payslip Dec2023Document1 pagePayslip Dec2023dhanalakhPas encore d'évaluation

- Income From Salary QUESTIONSDocument20 pagesIncome From Salary QUESTIONSSiva SankariPas encore d'évaluation

- SalaryDocument80 pagesSalarykalyanikamineniPas encore d'évaluation

- Account StatementDocument4 pagesAccount StatementdatadocsbdPas encore d'évaluation

- Advantages of Direct TaxesDocument3 pagesAdvantages of Direct TaxesIryna HoncharukPas encore d'évaluation

- Withholding of Income Tax On Compensation Income.-: REVENUE REGULATIONS NO. 10-2008 Issued On September 24, 2008Document17 pagesWithholding of Income Tax On Compensation Income.-: REVENUE REGULATIONS NO. 10-2008 Issued On September 24, 2008Kenneth Marvin MateoPas encore d'évaluation

- Bank Statement09-2020Document6 pagesBank Statement09-2020Tnt SolutionsPas encore d'évaluation

- InvoiceDocument1 pageInvoiceJakka LakshmikanthPas encore d'évaluation

- GST On Restaurants GST Regime: Rate of Bills Type of Restaurants Tax RateDocument17 pagesGST On Restaurants GST Regime: Rate of Bills Type of Restaurants Tax RateshyamPas encore d'évaluation

- Ellis S Frison IRS DecisionDocument5 pagesEllis S Frison IRS DecisionLilly EllisPas encore d'évaluation

- Tax Remedies Under NircDocument17 pagesTax Remedies Under NircFelixberto Jr. BaisPas encore d'évaluation

- SeafarersDocument2 pagesSeafarersJEZRELL E. ENRICOSOPas encore d'évaluation