Vous aimerez peut-être aussi

- CFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)D'EverandCFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)Évaluation : 4.5 sur 5 étoiles4.5/5 (5)

- Quizzer - Cost Volume Profit AnalysisDocument8 pagesQuizzer - Cost Volume Profit AnalysisJethro Gutlay100% (3)

- CFP Exam Calculation Workbook: 400+ Calculations to Prepare for the CFP Exam (2018 Edition)D'EverandCFP Exam Calculation Workbook: 400+ Calculations to Prepare for the CFP Exam (2018 Edition)Évaluation : 5 sur 5 étoiles5/5 (1)

- CVP Practice Exercises 3MA3 Part 2Document14 pagesCVP Practice Exercises 3MA3 Part 2Jyrus Cimatu100% (1)

- CVP Analysis Questions and AnswersDocument13 pagesCVP Analysis Questions and AnswersShe Rae PalmaPas encore d'évaluation

- EngineeringeconomyanswerssssDocument13 pagesEngineeringeconomyanswerssssMalik MalikPas encore d'évaluation

- Cost Accounting Interim ExamDocument5 pagesCost Accounting Interim Examgroup 1Pas encore d'évaluation

- Management Advisory Services ExamDocument12 pagesManagement Advisory Services ExamCiatto SpotifyPas encore d'évaluation

- Solutions Chapter 5Document13 pagesSolutions Chapter 5Laila Al Suwaidi100% (2)

- Managerial Accounting - Quiz.Document8 pagesManagerial Accounting - Quiz.chowchow12350% (2)

- CVP Analysis: Cost-Volume-Profit Techniques for Planning and Decision MakingDocument18 pagesCVP Analysis: Cost-Volume-Profit Techniques for Planning and Decision MakingDane Enterna50% (2)

- Module 4 Mark On Mark Down and Mark UpDocument46 pagesModule 4 Mark On Mark Down and Mark UpStacey VillanuevaPas encore d'évaluation

- Chapter 3 - TestbankDocument62 pagesChapter 3 - TestbankPhan Thi Tuyet Nhung67% (3)

- Cost Accounting Test Bank CKDocument12 pagesCost Accounting Test Bank CKLeo Tama67% (9)

- Accounting 122 Final ExamDocument6 pagesAccounting 122 Final ExamMethly MorenoPas encore d'évaluation

- Business Management Standard Level Paper 2: Instructions To CandidatesDocument7 pagesBusiness Management Standard Level Paper 2: Instructions To CandidatesjinLPas encore d'évaluation

- Practice: ACTG243 Quiz 5Document4 pagesPractice: ACTG243 Quiz 5GuruBaluLeoKingPas encore d'évaluation

- MSCI-3107 Managerial AccountingDocument4 pagesMSCI-3107 Managerial AccountingASMARA HABIB100% (1)

- A Sample Feasibility StudyDocument15 pagesA Sample Feasibility StudyJert Lee100% (4)

- 3 Test 3 AnswersDocument9 pages3 Test 3 AnswersRoger WilliamsPas encore d'évaluation

- Cost-Volume-Profit Analysis: True / False QuestionsDocument25 pagesCost-Volume-Profit Analysis: True / False QuestionsNaddie50% (2)

- ACC 115 - Chapter 21 Quiz - Cost Behavior and Cost-Volume-Profit AnalysisDocument3 pagesACC 115 - Chapter 21 Quiz - Cost Behavior and Cost-Volume-Profit AnalysisJoyPas encore d'évaluation

- Managerial Accounting 2Nd Edition Hilton Test Bank Full Chapter PDFDocument67 pagesManagerial Accounting 2Nd Edition Hilton Test Bank Full Chapter PDFjezebeldouglasz3n100% (8)

- CVP Excersise and ProjectsDocument6 pagesCVP Excersise and ProjectsbikilahussenPas encore d'évaluation

- MCQin Marginal CostingDocument5 pagesMCQin Marginal CostingnasPas encore d'évaluation

- CVP Analysis Chapter 4 Practice ProblemsDocument6 pagesCVP Analysis Chapter 4 Practice ProblemsAndrew Miranda100% (1)

- Model Exit Exam of Cost & Managerial CostDocument10 pagesModel Exit Exam of Cost & Managerial Costnewaybeyene5Pas encore d'évaluation

- Cost ObjectiveDocument5 pagesCost ObjectiveKarmen ThumPas encore d'évaluation

- Understanding Break-Even Analysis and Contribution Margin ConceptsDocument8 pagesUnderstanding Break-Even Analysis and Contribution Margin ConceptsraprapPas encore d'évaluation

- FAR EASTERN UNIVERSITY MANAGEMENT EXAMDocument18 pagesFAR EASTERN UNIVERSITY MANAGEMENT EXAMErin CruzPas encore d'évaluation

- Lyceum-Northwestern University: L-NU AA-23-02-01-18Document8 pagesLyceum-Northwestern University: L-NU AA-23-02-01-18Amie Jane MirandaPas encore d'évaluation

- Exercises Chapter 4 Cost Behavior and AnalysisDocument7 pagesExercises Chapter 4 Cost Behavior and AnalysishanaPas encore d'évaluation

- UNIVERSIDAD DE MANILA MIDTERM EXAMDocument6 pagesUNIVERSIDAD DE MANILA MIDTERM EXAMShiela Mae Pon AnPas encore d'évaluation

- 47 - 20210609083456 - Tugas Pertemuan 11 CVP AnalysisDocument5 pages47 - 20210609083456 - Tugas Pertemuan 11 CVP Analysistantri novebiPas encore d'évaluation

- MA - Practice Questions PDFDocument13 pagesMA - Practice Questions PDFSagunaChopraPas encore d'évaluation

- Cost Behavior QuestionsDocument13 pagesCost Behavior QuestionsNaddiePas encore d'évaluation

- CH 08 Pricing Q and MDocument17 pagesCH 08 Pricing Q and MJennifer ManlangitPas encore d'évaluation

- Answer2 TaDocument13 pagesAnswer2 TaJohn BryanPas encore d'évaluation

- Chapter 8 - QuestionsDocument22 pagesChapter 8 - QuestionsSoofeng LokPas encore d'évaluation

- Midterm Examination: Cost AccountingDocument12 pagesMidterm Examination: Cost AccountingHardly Dare GonzalesPas encore d'évaluation

- BreakevenDocument14 pagesBreakevenkay_kleirPas encore d'évaluation

- Accounting Hawk - AFAR - Incoming 3rd YearDocument11 pagesAccounting Hawk - AFAR - Incoming 3rd YearClaire BarbaPas encore d'évaluation

- Strategic Cost Management Midterm ExamDocument6 pagesStrategic Cost Management Midterm Examrizzamaybacarra.birPas encore d'évaluation

- Cost Test 1 PDFDocument3 pagesCost Test 1 PDFAnkit LilhaPas encore d'évaluation

- CVP Exercises ReviewerDocument2 pagesCVP Exercises Reviewerdaniellejueco1228Pas encore d'évaluation

- Review Materials Chapters 8, 10, 3 & 4 Term 3 Y18-19 PDFDocument19 pagesReview Materials Chapters 8, 10, 3 & 4 Term 3 Y18-19 PDFKrizelle Anne TaguinodPas encore d'évaluation

- Revision Module 7Document7 pagesRevision Module 7avineshPas encore d'évaluation

- Sample Problems 13Document7 pagesSample Problems 13milagrosdiPas encore d'évaluation

- Macc ReviewerDocument13 pagesMacc ReviewerAnnabel SenitaPas encore d'évaluation

- QuizDocument5 pagesQuizHà Nguyễn ThuPas encore d'évaluation

- Latihan Chapter 3 CVPDocument9 pagesLatihan Chapter 3 CVPS AdemPas encore d'évaluation

- Cs Marginal Costing TestDocument4 pagesCs Marginal Costing TestckbswcsypjPas encore d'évaluation

- Chapter 03 TestbankDocument108 pagesChapter 03 TestbankanukshaPas encore d'évaluation

- Module 3 Cost Volume Profit Analysis NA PDFDocument4 pagesModule 3 Cost Volume Profit Analysis NA PDFMadielyn Santarin Miranda50% (2)

- Kumpulan Kuis Akmen 2Document13 pagesKumpulan Kuis Akmen 2IstiqomahPas encore d'évaluation

- Multiple Choice QuestionsDocument31 pagesMultiple Choice QuestionsKim Audrey JalalainPas encore d'évaluation

- Consumer Choice Theory and Budget ConstraintsDocument8 pagesConsumer Choice Theory and Budget ConstraintsPhạm HuyPas encore d'évaluation

- Name Batch Teacher: Saba Nayyar Date Teacher Asstt: Shahab Marks 30Document4 pagesName Batch Teacher: Saba Nayyar Date Teacher Asstt: Shahab Marks 30shahabPas encore d'évaluation

- Strategic Cost Management Final ExamDocument8 pagesStrategic Cost Management Final Examrizzamaybacarra.birPas encore d'évaluation

- Measurement ConceptsDocument46 pagesMeasurement ConceptsPrabal Pratap Singh TomarPas encore d'évaluation

- Exercises: Variable Costing Antonio Jaramillo Dayag Multiple ChoiceDocument13 pagesExercises: Variable Costing Antonio Jaramillo Dayag Multiple ChoicenaddiePas encore d'évaluation

- MANAGEMENT ADVISORY SERVICESDocument16 pagesMANAGEMENT ADVISORY SERVICESEnola HolmesPas encore d'évaluation

- Cost2 AssiDocument4 pagesCost2 Assidamenaga35Pas encore d'évaluation

- SCM Print ReviewerDocument14 pagesSCM Print ReviewerprettyPas encore d'évaluation

- Practice Questions Week 5 Day 1 and 2 Multiple ChoiceDocument16 pagesPractice Questions Week 5 Day 1 and 2 Multiple ChoiceAnasChihabPas encore d'évaluation

- Multiple Choice Answer On The Scantron Provided ONLYDocument10 pagesMultiple Choice Answer On The Scantron Provided ONLYGiovana Marie Balasquide100% (1)

- AE22 ChapterTest 4 6 - AnswerKeyDocument6 pagesAE22 ChapterTest 4 6 - AnswerKeyElrey IncisoPas encore d'évaluation

- A to Z Cost Accounting Dictionary: A Practical Approach - Theory to CalculationD'EverandA to Z Cost Accounting Dictionary: A Practical Approach - Theory to CalculationPas encore d'évaluation

- ECN 321 - Intermediate Macroeconomics Practice QuestionsDocument2 pagesECN 321 - Intermediate Macroeconomics Practice Questionsmuyi kunlePas encore d'évaluation

- Consumption TheoriesDocument17 pagesConsumption Theoriesmuyi kunlePas encore d'évaluation

- MSC Practice QuestsDocument2 pagesMSC Practice Questsmuyi kunlePas encore d'évaluation

- 2020-2021 MSC Mon Econs AnswersDocument2 pages2020-2021 MSC Mon Econs Answersmuyi kunlePas encore d'évaluation

- Ecn121 MCQ AnswersDocument20 pagesEcn121 MCQ Answersmuyi kunlePas encore d'évaluation

- Fin 220 LMSDocument18 pagesFin 220 LMSmuyi kunlePas encore d'évaluation

- Data On Real GDP From 1999Document1 pageData On Real GDP From 1999muyi kunlePas encore d'évaluation

- National Income Accounting and Inflation MCQDocument29 pagesNational Income Accounting and Inflation MCQmuyi kunlePas encore d'évaluation

- Ecn 308Document2 pagesEcn 308muyi kunlePas encore d'évaluation

- Toto Inflation Term PaperDocument4 pagesToto Inflation Term Papermuyi kunlePas encore d'évaluation

- Econometrics TableDocument17 pagesEconometrics Tablemuyi kunlePas encore d'évaluation

- 318 Mcqs and AnswersDocument14 pages318 Mcqs and Answersmuyi kunlePas encore d'évaluation

- Cynthia ExactDocument2 pagesCynthia Exactmuyi kunlePas encore d'évaluation

- Econometrics TableDocument17 pagesEconometrics Tablemuyi kunlePas encore d'évaluation

- Tobin Q NoteDocument3 pagesTobin Q Notemuyi kunlePas encore d'évaluation

- Zach's Covid DataDocument5 pagesZach's Covid Datamuyi kunlePas encore d'évaluation

- Man Growth 2010 To 2016Document2 pagesMan Growth 2010 To 2016muyi kunlePas encore d'évaluation

- Basic Prod ConceptsDocument8 pagesBasic Prod Conceptsmuyi kunlePas encore d'évaluation

- INSTRUCTION: PLS, Try These Questions Whichever Way You Can. We'll Converge Here 9:00pm On Thursday To Share Solutions and CorrectionsDocument1 pageINSTRUCTION: PLS, Try These Questions Whichever Way You Can. We'll Converge Here 9:00pm On Thursday To Share Solutions and Correctionsmuyi kunlePas encore d'évaluation

- Collusive SolutionDocument2 pagesCollusive Solutionmuyi kunlePas encore d'évaluation

- Note On Circle GeometryDocument23 pagesNote On Circle Geometrymuyi kunlePas encore d'évaluation

- 314 Theory AnswersDocument1 page314 Theory Answersmuyi kunlePas encore d'évaluation

- Ols Simple RegressionDocument1 pageOls Simple Regressionmuyi kunlePas encore d'évaluation

- Effects of Public Expenditure On SelecteDocument18 pagesEffects of Public Expenditure On Selectemuyi kunlePas encore d'évaluation

- Rostow's 5 Stages of Economic Growth ModelDocument4 pagesRostow's 5 Stages of Economic Growth Modelmuyi kunlePas encore d'évaluation

- Standard Normal Probability DistributionDocument4 pagesStandard Normal Probability Distributionmuyi kunlePas encore d'évaluation

- A UnemploymentDocument13 pagesA Unemploymentmuyi kunlePas encore d'évaluation

- Taxation Ecn 314Document2 pagesTaxation Ecn 314muyi kunlePas encore d'évaluation

- Blanchard For ProjectDocument6 pagesBlanchard For Projectmuyi kunlePas encore d'évaluation

- Shadow Price: Socioeconomic Contributions of CommoditiesDocument1 pageShadow Price: Socioeconomic Contributions of Commoditiesmuyi kunlePas encore d'évaluation

- Potato Grader CIGR2019Document8 pagesPotato Grader CIGR2019Munnaf M AbdulPas encore d'évaluation

- Bill French Case Study AnalysisDocument11 pagesBill French Case Study AnalysisPRANAV KAKKARPas encore d'évaluation

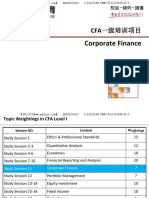

- v1 2015cfa强化一级班 企业理财 权益衍生 其他1Document250 pagesv1 2015cfa强化一级班 企业理财 权益衍生 其他1Mario XiePas encore d'évaluation

- Assignment On Cashew Nut Processing (Food Processing Management)Document10 pagesAssignment On Cashew Nut Processing (Food Processing Management)Slesha Patil100% (2)

- Retail Book Chap15Document31 pagesRetail Book Chap15Harman GillPas encore d'évaluation

- ENT Business Plan 07122022 121053pmDocument56 pagesENT Business Plan 07122022 121053pmAreej IftikharPas encore d'évaluation

- Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument6 pagesManila Cavite Laguna Cebu Cagayan de Oro Davaovane rondinaPas encore d'évaluation

- W12 Product EstimatingDocument61 pagesW12 Product EstimatingArizky Margo AgungPas encore d'évaluation

- Problems of Managing Small Scale Business in The Rural AreaDocument48 pagesProblems of Managing Small Scale Business in The Rural Areakritika soniPas encore d'évaluation

- Managerial Economics-Course PlanDocument2 pagesManagerial Economics-Course PlanAnnonymous963258Pas encore d'évaluation

- النسب المالية - إنجليزىDocument5 pagesالنسب المالية - إنجليزىMohamed Ahmed YassinPas encore d'évaluation

- 1 Om PPT M-1Document89 pages1 Om PPT M-1K P RUTHWIKPas encore d'évaluation

- Center of Gravity NoteDocument46 pagesCenter of Gravity Notefieyza adnPas encore d'évaluation

- Student Instructions - BikesDocument3 pagesStudent Instructions - BikesAndrea XiaoPas encore d'évaluation

- Akuntansi Manajemen Absoprtion CostingDocument7 pagesAkuntansi Manajemen Absoprtion CostingMuhammad SyahPas encore d'évaluation

- Be and CVP SamplesDocument7 pagesBe and CVP SamplesJeza Don LatosaPas encore d'évaluation

- MA2 Syllabus and Study Guide 2020-21 FINAL V2Document14 pagesMA2 Syllabus and Study Guide 2020-21 FINAL V2Mokoena RalesupiPas encore d'évaluation

- Basic Concepts of Economics MCQDocument64 pagesBasic Concepts of Economics MCQsachinPas encore d'évaluation

- Module 3 Week 7 Module Project FinalDocument25 pagesModule 3 Week 7 Module Project FinalMatthews OtalikePas encore d'évaluation

- Take-Home Diagnostic Examination (MS) : Accountancy ProgramDocument10 pagesTake-Home Diagnostic Examination (MS) : Accountancy ProgramSuzette VillalinoPas encore d'évaluation

- 4 2004 Jun QDocument10 pages4 2004 Jun Qmonazdeo9418Pas encore d'évaluation