Vous aimerez peut-être aussi

- 3.1 - FCFF ExcerciseDocument9 pages3.1 - FCFF ExcerciseHTPas encore d'évaluation

- Test 1Document6 pagesTest 1khowcatherine2000Pas encore d'évaluation

- Test 2Document7 pagesTest 2khowcatherine2000Pas encore d'évaluation

- LGC 142-164Document13 pagesLGC 142-164Pam YsonPas encore d'évaluation

- Pakistan Salary Income Tax Calculator Tax Year 2021 2022Document4 pagesPakistan Salary Income Tax Calculator Tax Year 2021 2022Kashif NiaziPas encore d'évaluation

- 2019 Tax Card PakistanDocument9 pages2019 Tax Card PakistanRaja Hamza rasgPas encore d'évaluation

- 24353-2002-Amending Ordinance No. 93-95 or TheDocument27 pages24353-2002-Amending Ordinance No. 93-95 or TheLUNA JEZERPas encore d'évaluation

- Tutorial 10 Tax AccountingDocument9 pagesTutorial 10 Tax AccountingAhmed HeshamPas encore d'évaluation

- Advanced Taxation - Singapore (Atx - SGP) : Strategic Professional - OptionsDocument12 pagesAdvanced Taxation - Singapore (Atx - SGP) : Strategic Professional - Optionsnivethababu7Pas encore d'évaluation

- Taxation - Singapore (TX - SGP) : Applied SkillsDocument19 pagesTaxation - Singapore (TX - SGP) : Applied SkillsLee WendyPas encore d'évaluation

- Advanced Taxation - Singapore (Atx - SGP) : Strategic Professional - OptionsDocument13 pagesAdvanced Taxation - Singapore (Atx - SGP) : Strategic Professional - OptionsLee WendyPas encore d'évaluation

- Tax Rates 2009-10Document2 pagesTax Rates 2009-10Mansoor AhmadPas encore d'évaluation

- Chapter 2Document17 pagesChapter 2ISLAM KHALED ZSCPas encore d'évaluation

- Instruction: Use This Excel File For Your SolutuonDocument3 pagesInstruction: Use This Excel File For Your SolutuonAudrelyn Carandang ArcenalPas encore d'évaluation

- Estate Tax Bir WebsiteDocument14 pagesEstate Tax Bir WebsiteCharlotte MalgapoPas encore d'évaluation

- Advanced Taxation - Singapore (Atx - SGP) : Strategic Professional - OptionsDocument12 pagesAdvanced Taxation - Singapore (Atx - SGP) : Strategic Professional - OptionsLee WendyPas encore d'évaluation

- RR 02-40Document137 pagesRR 02-40Nikki ChuaPas encore d'évaluation

- Taxation (Singapore) : March/June 2018 - Sample QuestionsDocument10 pagesTaxation (Singapore) : March/June 2018 - Sample QuestionsLee WendyPas encore d'évaluation

- Income Tax Rates For The Past 10 YearsDocument10 pagesIncome Tax Rates For The Past 10 YearsTarang DoshiPas encore d'évaluation

- Manila PDFDocument17 pagesManila PDFJela OasinPas encore d'évaluation

- Figures and Illustrations - Financial RatiosDocument19 pagesFigures and Illustrations - Financial RatioscamillaPas encore d'évaluation

- Real Property TaxDocument18 pagesReal Property TaxOman Paul AntiojoPas encore d'évaluation

- Jorg R. MenesesDocument3 pagesJorg R. MenesesKevin JugaoPas encore d'évaluation

- Finance DepartmenT CASE 3Document10 pagesFinance DepartmenT CASE 3Vighnesh ManojPas encore d'évaluation

- Taxation (Singapore) : March/June 2016 - Sample QuestionsDocument10 pagesTaxation (Singapore) : March/June 2016 - Sample QuestionsJobsdudePas encore d'évaluation

- Income TaxDocument5 pagesIncome TaxAshish NarulaPas encore d'évaluation

- Revenue Regulations No. 02-40Document1 pageRevenue Regulations No. 02-40Anonymous 01pQbZUMMPas encore d'évaluation

- Taxation 2 (Maika Notes)Document30 pagesTaxation 2 (Maika Notes)Maria Acepcion DelfinPas encore d'évaluation

- ESTATEDocument12 pagesESTATEVangie AntonioPas encore d'évaluation

- Price List 2012 TTCDocument5 pagesPrice List 2012 TTCRyan HjPas encore d'évaluation

- Donor'S Tax: BIR Form 1800Document4 pagesDonor'S Tax: BIR Form 1800JAYAR MENDZPas encore d'évaluation

- Sample BookkeepingDocument19 pagesSample BookkeepingENIDPas encore d'évaluation

- Tool - ROI CalculatorDocument10 pagesTool - ROI CalculatorTan TanPas encore d'évaluation

- Cash Budget AdvanceDocument6 pagesCash Budget AdvanceBhunesh KumarPas encore d'évaluation

- Diaper Case StudyDocument5 pagesDiaper Case StudyAbhijeet SarodePas encore d'évaluation

- f6sgp 2017 Sep Dec Q PDFDocument10 pagesf6sgp 2017 Sep Dec Q PDFJobsdudePas encore d'évaluation

- 1940 Income - Tax - Regulations20210424 12 1c79mjaDocument101 pages1940 Income - Tax - Regulations20210424 12 1c79mjaHADTUGIPas encore d'évaluation

- RR 2-40 Income TaxDocument165 pagesRR 2-40 Income Taxshinjha73Pas encore d'évaluation

- DHA Sector FinancialDocument3 pagesDHA Sector FinancialTJbossPas encore d'évaluation

- Break Even Analysis ActivityDocument3 pagesBreak Even Analysis ActivityHriday AmpavatinaPas encore d'évaluation

- Poultry Farm For 10000 ChicksDocument7 pagesPoultry Farm For 10000 ChicksDebashish PhonePas encore d'évaluation

- Taxation Question 2019 MarchDocument13 pagesTaxation Question 2019 MarchAlice DesiraeePas encore d'évaluation

- Income Tax Rates: For AY 2021-22 (New) & A.Y. 2020-21 (Old)Document2 pagesIncome Tax Rates: For AY 2021-22 (New) & A.Y. 2020-21 (Old)pankaj goyalPas encore d'évaluation

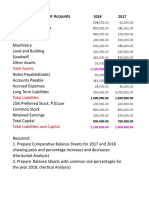

- Balance Sheet Accounts: Total AssetsDocument4 pagesBalance Sheet Accounts: Total AssetsJing SagittariusPas encore d'évaluation

- A Consent To Establish (Noc) : Industries Having Capital InvestmentDocument8 pagesA Consent To Establish (Noc) : Industries Having Capital InvestmentAnkit GuptaPas encore d'évaluation

- Illustrative Problem On Cash Budget: ST ND RD THDocument3 pagesIllustrative Problem On Cash Budget: ST ND RD THJean Kathyrine ChiongPas encore d'évaluation

- Professional Tax Act KPKDocument6 pagesProfessional Tax Act KPKHumayunPas encore d'évaluation

- Practical Test Finance & AccountingDocument7 pagesPractical Test Finance & AccountingAlbert CandraPas encore d'évaluation

- Lodge No. 761, 105 Phil. 983Document19 pagesLodge No. 761, 105 Phil. 983Kim EstalPas encore d'évaluation

- 2020 Minimum Taxable Income Rate of Tax Maximum Taxable Income Fixed Amount Amount ExceedingDocument2 pages2020 Minimum Taxable Income Rate of Tax Maximum Taxable Income Fixed Amount Amount Exceedingsarwar raziPas encore d'évaluation

- Indah Water Portal - Charges CommercialDocument2 pagesIndah Water Portal - Charges CommercialHafidzul ZakariaPas encore d'évaluation

- TEST3Document13 pagesTEST3Jonathan FaustinoPas encore d'évaluation

- Tax Computation FY 2020-21Document9 pagesTax Computation FY 2020-21kumar kartikeyaPas encore d'évaluation

- Group 2-Fin 6000BDocument7 pagesGroup 2-Fin 6000BBellindah wPas encore d'évaluation

- Description Tax Form Documentary Requirements Tax Rates Procedures Related Revenue Issuances Codal Reference Frequently Asked QuestionsDocument15 pagesDescription Tax Form Documentary Requirements Tax Rates Procedures Related Revenue Issuances Codal Reference Frequently Asked QuestionsJamel torresPas encore d'évaluation

- Pessimistic Expected OptimisticDocument3 pagesPessimistic Expected OptimisticGonçalo AlmeidaPas encore d'évaluation

- Bmac5203 AssgDocument8 pagesBmac5203 AssgMadhu SudhanPas encore d'évaluation

- F6SGP Dec2015q PDFDocument15 pagesF6SGP Dec2015q PDFDrift SirPas encore d'évaluation

- Judiciary Legal StandingDocument1 pageJudiciary Legal StandingHershey GabiPas encore d'évaluation

- Atty Sandoval - Oct 28Document6 pagesAtty Sandoval - Oct 28Hershey GabiPas encore d'évaluation

- Lyceum Vs CA - Corporate Name Doctrine of Secondary MeaningDocument2 pagesLyceum Vs CA - Corporate Name Doctrine of Secondary MeaningHershey GabiPas encore d'évaluation

- 124125-1998-City Sheriff Iligan City v. FortunadoDocument6 pages124125-1998-City Sheriff Iligan City v. FortunadoHershey GabiPas encore d'évaluation

- 3.-Commissioner of Internal Revenue v. GonzalesDocument13 pages3.-Commissioner of Internal Revenue v. GonzalesHershey GabiPas encore d'évaluation

- Fairbuilding Ne Twork: Bci'S Corporate Social Responsibility InitiativeDocument17 pagesFairbuilding Ne Twork: Bci'S Corporate Social Responsibility InitiativeHershey GabiPas encore d'évaluation

- 140424-1974-Occe - A - v. - Marquez20181119-5466-1pghgeyDocument8 pages140424-1974-Occe - A - v. - Marquez20181119-5466-1pghgeyHershey GabiPas encore d'évaluation

- People V SanchezDocument4 pagesPeople V SanchezHershey GabiPas encore d'évaluation

- Final Exams Week Study Plan: Monday Tuesday Wednesday Thursday Friday Saturday SundayDocument2 pagesFinal Exams Week Study Plan: Monday Tuesday Wednesday Thursday Friday Saturday SundayHershey GabiPas encore d'évaluation

- Lawyer's Duties in Handling Client's CaseDocument128 pagesLawyer's Duties in Handling Client's CaseHershey GabiPas encore d'évaluation

- Omnibus Notes Format 2019: RespondentsDocument1 pageOmnibus Notes Format 2019: RespondentsHershey GabiPas encore d'évaluation

- FBN Brochure Sept 2018 - For PrintDocument16 pagesFBN Brochure Sept 2018 - For PrintHershey GabiPas encore d'évaluation

- Midterms ProjectDocument14 pagesMidterms ProjectHershey GabiPas encore d'évaluation

- 01 - G.R. No. 97764 - Macasiano v. DioknoDocument10 pages01 - G.R. No. 97764 - Macasiano v. DioknoHershey GabiPas encore d'évaluation

- Playground BoqDocument2 pagesPlayground BoqHershey Gabi0% (1)

- People V Sanchez: Page 1 of 4Document4 pagesPeople V Sanchez: Page 1 of 4Hershey GabiPas encore d'évaluation

- 12 - G.R. No. L-24670 - Ortigas - Amp - Amp - Co., Ltd. Partnership v. FeatiDocument14 pages12 - G.R. No. L-24670 - Ortigas - Amp - Amp - Co., Ltd. Partnership v. FeatiHershey GabiPas encore d'évaluation

- PUBCORP Final Exam PointersDocument1 pagePUBCORP Final Exam PointersHershey GabiPas encore d'évaluation

- 03 - G.R. No. 73155 - Tan v. Commission On ElectionsDocument17 pages03 - G.R. No. 73155 - Tan v. Commission On ElectionsHershey GabiPas encore d'évaluation

- Gabi, Hershey Public Corporation Atty. Rodolfo Lapid: FactsDocument24 pagesGabi, Hershey Public Corporation Atty. Rodolfo Lapid: FactsHershey GabiPas encore d'évaluation

- Philippine Institute of ArbitratorsDocument8 pagesPhilippine Institute of ArbitratorsHershey GabiPas encore d'évaluation

- Solar RequirementsDocument2 pagesSolar RequirementsHershey GabiPas encore d'évaluation

- Suitability Assessment Form PDFDocument5 pagesSuitability Assessment Form PDFHershey GabiPas encore d'évaluation

- To Celebrate Our Successes, We Are Holding The 2 Fairbuilding Awards On 19 April 2018 at The Discovery Primea, Subject To ChangeDocument2 pagesTo Celebrate Our Successes, We Are Holding The 2 Fairbuilding Awards On 19 April 2018 at The Discovery Primea, Subject To ChangeHershey GabiPas encore d'évaluation

- Set 3 ConsolidatedDocument13 pagesSet 3 ConsolidatedHershey GabiPas encore d'évaluation

- AntiglobalizationDocument26 pagesAntiglobalizationDuDuTranPas encore d'évaluation

- Rasanga Curriculum VitaeDocument5 pagesRasanga Curriculum VitaeKevo NdaiPas encore d'évaluation

- FOR Office USE Only: HDFC Life Sb/Ca/Cc/Sb-Nre/Sb-Nro/OtherDocument2 pagesFOR Office USE Only: HDFC Life Sb/Ca/Cc/Sb-Nre/Sb-Nro/OtherVIkashPas encore d'évaluation

- Curriculum Vitae: Personal DataDocument3 pagesCurriculum Vitae: Personal DataAgungBolaangPas encore d'évaluation

- TeslaDocument20 pagesTeslaArpit Singh100% (1)

- Rec Max VS Opt AltDocument4 pagesRec Max VS Opt AltAloka RanasinghePas encore d'évaluation

- 12 CONFUCIUS SY 2O23 For Insurance GPA TemplateDocument9 pages12 CONFUCIUS SY 2O23 For Insurance GPA TemplateIris Kayte Huesca EvicnerPas encore d'évaluation

- Mariana Mazzucato - The Value of Everything. Making and Taking in The Global Economy (2018, Penguin)Document318 pagesMariana Mazzucato - The Value of Everything. Making and Taking in The Global Economy (2018, Penguin)Jorge Echavarría Carvajal100% (19)

- Professor Sir Colin Buchanan - Obituary From IndependentDocument3 pagesProfessor Sir Colin Buchanan - Obituary From IndependentSKM Colin BuchananPas encore d'évaluation

- Strategies For Managing Large-Scale Mining Sector Land Use Conflicts in The Global SouthDocument9 pagesStrategies For Managing Large-Scale Mining Sector Land Use Conflicts in The Global Southamerico centonPas encore d'évaluation

- Jose C. Guico For Petitioner. Wilfredo Cortez For Private RespondentsDocument5 pagesJose C. Guico For Petitioner. Wilfredo Cortez For Private Respondentsmichelle m. templadoPas encore d'évaluation

- PNB v. AtendidoDocument2 pagesPNB v. AtendidoAntonio RebosaPas encore d'évaluation

- CCM Parameters vs. J1939 ParametersDocument3 pagesCCM Parameters vs. J1939 Parameterszxy320dPas encore d'évaluation

- An Iot Based Dam Water Management System For AgricultureDocument21 pagesAn Iot Based Dam Water Management System For AgriculturemathewsPas encore d'évaluation

- Subject: Issues in Pakistan'S EconomyDocument13 pagesSubject: Issues in Pakistan'S EconomyTyped FYPas encore d'évaluation

- Scitech Prelim HandoutsDocument12 pagesScitech Prelim Handoutsms.cloudyPas encore d'évaluation

- New Economic Policy of IndiaDocument23 pagesNew Economic Policy of IndiaAbhishek Singh Rathor100% (1)

- BCG Tata GroupDocument3 pagesBCG Tata GroupChetanTejani100% (2)

- PAMI Asia Balanced Fund Product Primer v3 Intro TextDocument1 pagePAMI Asia Balanced Fund Product Primer v3 Intro Textgenie1970Pas encore d'évaluation

- Bank - A Financial Institution Licensed To Receive Deposits and Make Loans. Banks May AlsoDocument3 pagesBank - A Financial Institution Licensed To Receive Deposits and Make Loans. Banks May AlsoKyle PanlaquiPas encore d'évaluation

- ChartsDocument4 pagesChartsMyriam GGoPas encore d'évaluation

- Vol. 1: Basic Planning: Overseas Customer Service Facility GuideDocument35 pagesVol. 1: Basic Planning: Overseas Customer Service Facility GuideMishell TatianaPas encore d'évaluation

- 2.01 Economic SystemsDocument16 pages2.01 Economic SystemsRessie Joy Catherine FelicesPas encore d'évaluation

- Metro Manila, Philippines: by Junio M RagragioDocument21 pagesMetro Manila, Philippines: by Junio M RagragiofrancisPas encore d'évaluation

- Report Sugar MillDocument51 pagesReport Sugar MillMuhammadAyyazIqbal100% (1)

- AILET Last 5 Year Question Papers Answer Key 2019 2023Document196 pagesAILET Last 5 Year Question Papers Answer Key 2019 2023Pranav SinghPas encore d'évaluation

- Chicago 'Buycks' Lawsuit PlaintiffsDocument6 pagesChicago 'Buycks' Lawsuit PlaintiffsThe Daily CallerPas encore d'évaluation

- The Proof of Agricultural ZakatDocument7 pagesThe Proof of Agricultural ZakatDila Estu KinasihPas encore d'évaluation

- Life Cycle AssessmentDocument11 pagesLife Cycle Assessmentrslapena100% (1)

- KM 3Document4 pagesKM 3Ilham Binte AkhterPas encore d'évaluation

- Summary of Noah Kagan's Million Dollar WeekendD'EverandSummary of Noah Kagan's Million Dollar WeekendÉvaluation : 5 sur 5 étoiles5/5 (2)

- The Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeD'EverandThe Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeÉvaluation : 4.5 sur 5 étoiles4.5/5 (90)

- $100M Leads: How to Get Strangers to Want to Buy Your StuffD'Everand$100M Leads: How to Get Strangers to Want to Buy Your StuffÉvaluation : 5 sur 5 étoiles5/5 (19)

- $100M Offers: How to Make Offers So Good People Feel Stupid Saying NoD'Everand$100M Offers: How to Make Offers So Good People Feel Stupid Saying NoÉvaluation : 5 sur 5 étoiles5/5 (26)

- The Coaching Habit: Say Less, Ask More & Change the Way You Lead ForeverD'EverandThe Coaching Habit: Say Less, Ask More & Change the Way You Lead ForeverÉvaluation : 4.5 sur 5 étoiles4.5/5 (186)

- The Leader Habit: Master the Skills You Need to Lead--in Just Minutes a DayD'EverandThe Leader Habit: Master the Skills You Need to Lead--in Just Minutes a DayÉvaluation : 4 sur 5 étoiles4/5 (5)

- High Road Leadership: Bringing People Together in a World That DividesD'EverandHigh Road Leadership: Bringing People Together in a World That DividesPas encore d'évaluation

- Summary of Thinking, Fast and Slow: by Daniel KahnemanD'EverandSummary of Thinking, Fast and Slow: by Daniel KahnemanÉvaluation : 4 sur 5 étoiles4/5 (117)

- Radical Confidence: 11 Lessons on How to Get the Relationship, Career, and Life You WantD'EverandRadical Confidence: 11 Lessons on How to Get the Relationship, Career, and Life You WantÉvaluation : 5 sur 5 étoiles5/5 (52)

- Broken Money: Why Our Financial System Is Failing Us and How We Can Make It BetterD'EverandBroken Money: Why Our Financial System Is Failing Us and How We Can Make It BetterÉvaluation : 5 sur 5 étoiles5/5 (3)

- Summary of Zero to One: Notes on Startups, or How to Build the FutureD'EverandSummary of Zero to One: Notes on Startups, or How to Build the FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (100)

- The First Minute: How to start conversations that get resultsD'EverandThe First Minute: How to start conversations that get resultsÉvaluation : 4.5 sur 5 étoiles4.5/5 (57)