Vous aimerez peut-être aussi

- Ong816 Bills Nov 2022Document2 pagesOng816 Bills Nov 2022Pavan KumarPas encore d'évaluation

- Urja Mitra Application - Jharkhand Bijli Vitran Nigam LTD - PDFDocument2 pagesUrja Mitra Application - Jharkhand Bijli Vitran Nigam LTD - PDFgmatweakPas encore d'évaluation

- ACCOUNT NO: 40114640559: Mode of Payment Dishonoured ChequeDocument2 pagesACCOUNT NO: 40114640559: Mode of Payment Dishonoured Chequeshubhanshu5758Pas encore d'évaluation

- vsp635NOV17 PDFDocument2 pagesvsp635NOV17 PDFvzprelePas encore d'évaluation

- Urja Mitra Application - Jharkhand Bijli Vitran Nigam LTD PDFDocument2 pagesUrja Mitra Application - Jharkhand Bijli Vitran Nigam LTD PDFRajPas encore d'évaluation

- MP Factory License Form 4 Fill Print UseDocument3 pagesMP Factory License Form 4 Fill Print Useamiteshr100% (1)

- Property TaxDocument1 pageProperty TaxBig BossPas encore d'évaluation

- Printed by SYSUSER: Dial Toll Free 1912 For Bill & Supply ComplaintsDocument1 pagePrinted by SYSUSER: Dial Toll Free 1912 For Bill & Supply ComplaintsManish MPas encore d'évaluation

- OCI Introduction: Presented By: Rahul MiglaniDocument21 pagesOCI Introduction: Presented By: Rahul Miglanisss pppPas encore d'évaluation

- Meter Reading Details: Assam Power Distribution Company LimitedDocument1 pageMeter Reading Details: Assam Power Distribution Company LimitedParthapratim GogoiPas encore d'évaluation

- FIXED LINE Bill 08049529799 854296214Document3 pagesFIXED LINE Bill 08049529799 854296214ashutoshPas encore d'évaluation

- CA NoDocument3 pagesCA NoGrish ChandraPas encore d'évaluation

- Current Month Bill Details New (May - 2019) : Home Billing InformationDocument1 pageCurrent Month Bill Details New (May - 2019) : Home Billing Informationpyramid lavanPas encore d'évaluation

- BillDocument1 pageBillSowmya DPas encore d'évaluation

- Monthly Statement: This Month's SummaryDocument9 pagesMonthly Statement: This Month's SummaryJawedPas encore d'évaluation

- TANGEDCO Online Payment-1Document1 pageTANGEDCO Online Payment-1Dinesh GuruPas encore d'évaluation

- Urja Mitra Application - Jharkhand Bijli Vitran Nigam LTDDocument1 pageUrja Mitra Application - Jharkhand Bijli Vitran Nigam LTDBipin KumarPas encore d'évaluation

- AugTelephone BillDocument2 pagesAugTelephone BillRamesh P100% (1)

- 23010517220260948V7H626472791273BMB137076626R7Document3 pages23010517220260948V7H626472791273BMB137076626R7SiddharthPas encore d'évaluation

- KMC Tax Reciept - 2019Document1 pageKMC Tax Reciept - 2019Biswabandhu PalPas encore d'évaluation

- Urja Mitra Application - Jharkhand Bijli Vitran Nigam LTD - DumkaDocument2 pagesUrja Mitra Application - Jharkhand Bijli Vitran Nigam LTD - DumkaSaket KumarPas encore d'évaluation

- Orig 230007885568Document1 pageOrig 230007885568Shivam KhoslaPas encore d'évaluation

- View BillDocument1 pageView BillOm PrakashPas encore d'évaluation

- Printed by SYSUSER: Dial Toll Free 1912 For Bill & Supply ComplaintsDocument1 pagePrinted by SYSUSER: Dial Toll Free 1912 For Bill & Supply ComplaintsGaurav KohliPas encore d'évaluation

- 2021051722026094G76520650937278BMB137076625R7Document2 pages2021051722026094G76520650937278BMB137076625R7SiddharthPas encore d'évaluation

- PDFServlet PDFDocument1 pagePDFServlet PDFAjay SinghPas encore d'évaluation

- PSPCL Bill 3015013843 Due On 2020-JUN-08Document2 pagesPSPCL Bill 3015013843 Due On 2020-JUN-08RitishPas encore d'évaluation

- SDMC Property Tax Delhi 2018-19Document1 pageSDMC Property Tax Delhi 2018-19Dushyant HoodaPas encore d'évaluation

- View BillDocument1 pageView BillParvezPas encore d'évaluation

- SDMC Property Tax Delhi 2015-16Document1 pageSDMC Property Tax Delhi 2015-16Divyansh AgarwalPas encore d'évaluation

- HESCO ONLINE BILLL NovDocument2 pagesHESCO ONLINE BILLL NovHanif GhiranoPas encore d'évaluation

- EMS ResultDocument2 pagesEMS ResultSmeeta AralikattiPas encore d'évaluation

- Wa0001 PDFDocument1 pageWa0001 PDFKevinPas encore d'évaluation

- Compu TationDocument3 pagesCompu TationAbhilash M NairPas encore d'évaluation

- Duplicate Bill: For Any Queries On This Bill Please Contact MSEDCL CallDocument1 pageDuplicate Bill: For Any Queries On This Bill Please Contact MSEDCL CallAnonymous 2WZqzwjcHPas encore d'évaluation

- Tripura State Electricity Corporation Ltd. (A GOVT. of Tripura Enterprise)Document1 pageTripura State Electricity Corporation Ltd. (A GOVT. of Tripura Enterprise)Tanmoy ChakrabortyPas encore d'évaluation

- Duplicate Bill: For Any Queries On This Bill Please Contact MSEDCL Call Center: 1800 233Document1 pageDuplicate Bill: For Any Queries On This Bill Please Contact MSEDCL Call Center: 1800 233Arun RanaPas encore d'évaluation

- Foreclosure 12 24 05Document3 pagesForeclosure 12 24 05Sunil LaygudePas encore d'évaluation

- Tripura State Electricity Corporation Ltd. (A GOVT. of Tripura Enterprise)Document1 pageTripura State Electricity Corporation Ltd. (A GOVT. of Tripura Enterprise)Anonymous nrvHJVz9Pas encore d'évaluation

- Indian Income Tax Return: (Refer Instructions For Eligibility)Document7 pagesIndian Income Tax Return: (Refer Instructions For Eligibility)Vikas CheedellaPas encore d'évaluation

- Monthly Statement: This Month's SummaryDocument4 pagesMonthly Statement: This Month's SummaryHjPas encore d'évaluation

- Opensearch PDFDocument1 pageOpensearch PDFRazin FarookPas encore d'évaluation

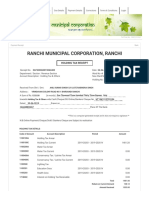

- Ranchi Municipal Corporation, Ranchi: Holding Tax ReceiptDocument2 pagesRanchi Municipal Corporation, Ranchi: Holding Tax ReceiptDurgesh Nandan Yadav0% (1)

- GHMC Tax Paid ReceiptDocument2 pagesGHMC Tax Paid ReceiptSrinivas SukhavasiPas encore d'évaluation

- Print Application FormUPPSCDocument2 pagesPrint Application FormUPPSCSayantan PaulPas encore d'évaluation

- Aadhaar Update Form: Aadhaar Enrolment Is Free & VoluntaryDocument4 pagesAadhaar Update Form: Aadhaar Enrolment Is Free & VoluntaryDIS PMJAYPas encore d'évaluation

- Passport Appointment RecieptDocument3 pagesPassport Appointment RecieptMohit ChinchkhedePas encore d'évaluation

- Computation 19-20Document2 pagesComputation 19-20madali sivareddyPas encore d'évaluation

- CSC Online Registration Process - CompressedDocument9 pagesCSC Online Registration Process - CompressedMedagam VenkateswarareddyPas encore d'évaluation

- LT Bill 57000406406 201907Document2 pagesLT Bill 57000406406 201907Faku RikiPas encore d'évaluation

- Water Bill June19 MidcDocument1 pageWater Bill June19 MidcManoj SahuPas encore d'évaluation

- GWL - Anandn - F: Carton Code Along With Plastic Bag Code PL09Document1 pageGWL - Anandn - F: Carton Code Along With Plastic Bag Code PL09RahulPas encore d'évaluation

- Property Tax AHEMDABADDocument1 pageProperty Tax AHEMDABADSatkar GarmentPas encore d'évaluation

- Bill of Supply For Electricity: Due Date: 09-10-2019Document1 pageBill of Supply For Electricity: Due Date: 09-10-2019Habeeb AlamPas encore d'évaluation

- Printed by SYSUSER: Dial Toll Free 1912 For Bill & Supply ComplaintsDocument1 pagePrinted by SYSUSER: Dial Toll Free 1912 For Bill & Supply ComplaintsAartiPas encore d'évaluation

- EDMC Property Tax Delhi 2018-19Document1 pageEDMC Property Tax Delhi 2018-19Indra MishraPas encore d'évaluation

- PAN Application Acknowledgment Receipt For Form 49A (Physical Application)Document1 pagePAN Application Acknowledgment Receipt For Form 49A (Physical Application)Niranjan KumarPas encore d'évaluation

- Uttarakhand Power Corporation Limited: ACCOUNT NO: 40103815063Document2 pagesUttarakhand Power Corporation Limited: ACCOUNT NO: 40103815063Asheesh SemwalPas encore d'évaluation

- Building and Land Valuation Formate 17.11.2021 Global VillageDocument12 pagesBuilding and Land Valuation Formate 17.11.2021 Global Villagerachana infrastructures nagendraPas encore d'évaluation

- Application Appendix A1Document6 pagesApplication Appendix A1Abhilash Mu0% (1)

- APPELANTDocument30 pagesAPPELANTTAS MUNPas encore d'évaluation

- Atlas of Pollen and Spores and Their Parent Taxa of MT Kilimanjaro and Tropical East AfricaDocument86 pagesAtlas of Pollen and Spores and Their Parent Taxa of MT Kilimanjaro and Tropical East AfricaEdilson Silva100% (1)

- ExtractedRA - CIVILENG - MANILA - Nov2017 RevDocument62 pagesExtractedRA - CIVILENG - MANILA - Nov2017 Revkelvin jake castroPas encore d'évaluation

- Bus 685 Final ReportDocument25 pagesBus 685 Final Reportabu.sakibPas encore d'évaluation

- A Multivariate Model For Analyzing Crime Scene InformationDocument26 pagesA Multivariate Model For Analyzing Crime Scene InformationNorberth Ioan OkrosPas encore d'évaluation

- Assessment of The Role of Radio in The Promotion of Community Health in Ogui Urban Area, EnuguDocument21 pagesAssessment of The Role of Radio in The Promotion of Community Health in Ogui Urban Area, EnuguPst W C PetersPas encore d'évaluation

- Against Temple Adverse Possession by Private PersonDocument12 pagesAgainst Temple Adverse Possession by Private PersonBest NiftyPas encore d'évaluation

- Section 6 Novation: Study GuideDocument11 pagesSection 6 Novation: Study GuideElsha DamoloPas encore d'évaluation

- I.I.M.U.N. Coimbatore Kids Module 2021Document7 pagesI.I.M.U.N. Coimbatore Kids Module 2021Midhun Bhuvanesh.B 7APas encore d'évaluation

- Former UM Soccer Coach Sues University For DefamationDocument12 pagesFormer UM Soccer Coach Sues University For DefamationNBC MontanaPas encore d'évaluation

- Natelco Vs CADocument10 pagesNatelco Vs CAcharmdelmoPas encore d'évaluation

- Determination of Distribution Coefficient of Iodine Between Two Immiscible SolventsDocument6 pagesDetermination of Distribution Coefficient of Iodine Between Two Immiscible SolventsRafid Jawad100% (1)

- 06 5D+TeacherEvalRubric With ObservablesDocument39 pages06 5D+TeacherEvalRubric With ObservablesKorey Bradley100% (1)

- How To Argue A CaseDocument5 pagesHow To Argue A CaseItam HillPas encore d'évaluation

- Legal AgreementDocument2 pagesLegal AgreementMohd NadeemPas encore d'évaluation

- Organization of Preschool Education in SwedenDocument2 pagesOrganization of Preschool Education in SwedenNelumi PereraPas encore d'évaluation

- M.Vikram: Department of Electronics and Communication EngineeringDocument26 pagesM.Vikram: Department of Electronics and Communication EngineeringSyed AmaanPas encore d'évaluation

- Diss PDFDocument321 pagesDiss PDFAbdullah GhannamPas encore d'évaluation

- Body Repairs - General Body RepairsDocument49 pagesBody Repairs - General Body RepairsjomialhePas encore d'évaluation

- Police Law EnforcementDocument4 pagesPolice Law EnforcementSevilla JoenardPas encore d'évaluation

- Image Saving, Processing and Name Tagging Over SDTP Using Java ScriptDocument21 pagesImage Saving, Processing and Name Tagging Over SDTP Using Java Scriptsomnath banerjeePas encore d'évaluation

- Trading With The Heikin Ashi Candlestick OscillatorDocument7 pagesTrading With The Heikin Ashi Candlestick OscillatorDarren TanPas encore d'évaluation

- MC DuroDesign EDocument8 pagesMC DuroDesign Epetronela.12Pas encore d'évaluation

- Additive ManufactDocument61 pagesAdditive ManufactAnca Maria TruscaPas encore d'évaluation

- Sri Nikunja-Keli-VirudavaliDocument12 pagesSri Nikunja-Keli-VirudavaliIronChavesPas encore d'évaluation

- Programme Guide - PGDMCH PDFDocument58 pagesProgramme Guide - PGDMCH PDFNJMU 2006Pas encore d'évaluation

- Literature Review of Quality of Healthcare Services in IndiaDocument27 pagesLiterature Review of Quality of Healthcare Services in IndiaMunnangi NagendrareddyPas encore d'évaluation

- A Financial Analysis of Alibaba Group Holding LTDDocument26 pagesA Financial Analysis of Alibaba Group Holding LTDSrinu Gattu50% (4)

- Gann Trding PDFDocument9 pagesGann Trding PDFMayur KasarPas encore d'évaluation

- Chapter 18 Metric and Imperial Measures: Scheme of WorkDocument2 pagesChapter 18 Metric and Imperial Measures: Scheme of WorkrightwayPas encore d'évaluation