Vous aimerez peut-être aussi

- Summary of Educational TourDocument14 pagesSummary of Educational TourChin Tatoy DoloricaPas encore d'évaluation

- Final Revised1 PDFDocument72 pagesFinal Revised1 PDFSarah Mae SorianoPas encore d'évaluation

- Marketing ResearchDocument62 pagesMarketing ResearchAngel Lowe Angeles BalinconganPas encore d'évaluation

- HRM ReviewerDocument9 pagesHRM ReviewerJenefer Diano100% (1)

- Research Chapter 1 To 5 Final Post-DefenseDocument36 pagesResearch Chapter 1 To 5 Final Post-DefensecharinaPas encore d'évaluation

- Chapter 2 1 PDFDocument4 pagesChapter 2 1 PDFTeamSoiraPas encore d'évaluation

- FinaLE (Financial Literacy Education) Towards Prosperity ADVOCACYDocument4 pagesFinaLE (Financial Literacy Education) Towards Prosperity ADVOCACYJowelyn CasigniaPas encore d'évaluation

- Chapter 3 External AssessmentDocument91 pagesChapter 3 External Assessmentgjzbqq9fzwPas encore d'évaluation

- Source of Ideas For Entrepreneurial VenturesDocument13 pagesSource of Ideas For Entrepreneurial VenturesKelvin Jay Sebastian SaplaPas encore d'évaluation

- Hbo - Prelim ExamDocument3 pagesHbo - Prelim Examray100% (1)

- Chapter 1Document7 pagesChapter 1Krisk TadeoPas encore d'évaluation

- FinalresearchDocument43 pagesFinalresearchJustin mae PaderesPas encore d'évaluation

- Local StudiesDocument4 pagesLocal StudiesAlexandraPas encore d'évaluation

- Chapter IDocument15 pagesChapter Icheng mercadoPas encore d'évaluation

- Lesson 4 For EntrepDocument14 pagesLesson 4 For EntrepRhea May Peduca67% (3)

- Code of Ethics and Business ConductDocument14 pagesCode of Ethics and Business ConductBlessie Coleta0% (1)

- The Six Step Process To Financial Planning PDFDocument2 pagesThe Six Step Process To Financial Planning PDFstarvindsouza91100% (1)

- CHAPTER 2 (2) PaynalDocument11 pagesCHAPTER 2 (2) PaynalKristine Joy LarderaPas encore d'évaluation

- Chapter 2 Review Related LiteratureDocument4 pagesChapter 2 Review Related LiteratureJanida Basman DalidigPas encore d'évaluation

- Group 1 ResearchDocument29 pagesGroup 1 ResearchJeann Mae CascañoPas encore d'évaluation

- BUSINESS ETHICS AND SOCIAL RESPONSIBILITY NotesDocument6 pagesBUSINESS ETHICS AND SOCIAL RESPONSIBILITY NotesMaria Shaen Villanueva50% (4)

- 1 Meaning Classification Nature and Function of CreditDocument7 pages1 Meaning Classification Nature and Function of CreditMartije MonesaPas encore d'évaluation

- Influencing Factors of Using GCASHDocument8 pagesInfluencing Factors of Using GCASHGilconedo Baya JrPas encore d'évaluation

- Module 7 Communication For Academic PurposesDocument50 pagesModule 7 Communication For Academic PurposesJoksian TrapelaPas encore d'évaluation

- The Problem and Its SettingDocument45 pagesThe Problem and Its SettingAtlas MayoPas encore d'évaluation

- Chapter 3, Lesson 3: Organizational Market SegmentationDocument12 pagesChapter 3, Lesson 3: Organizational Market SegmentationCristel TomasPas encore d'évaluation

- Chapter-2 Models of Organizational Behavior (Group-2)Document28 pagesChapter-2 Models of Organizational Behavior (Group-2)SabbirPas encore d'évaluation

- Questionnaire-Checklist "The Effects of Expensive Tricycle Fare in Antipolo, City"Document2 pagesQuestionnaire-Checklist "The Effects of Expensive Tricycle Fare in Antipolo, City"Kristle R BacolodPas encore d'évaluation

- ReviewDocument32 pagesReviewroyarvin100% (1)

- Review of Related Literature and StudiesDocument5 pagesReview of Related Literature and StudiesJianneDanaoPas encore d'évaluation

- Marketing Plan For Milk TeaDocument3 pagesMarketing Plan For Milk Teacatherine mamaclayPas encore d'évaluation

- Silvania Module 5 PR2Document3 pagesSilvania Module 5 PR2Alain Salvador0% (1)

- Title Page I Approval Sheet II III Tables of Contents IV List of Tables V List of Figures VI AcknowledgementDocument12 pagesTitle Page I Approval Sheet II III Tables of Contents IV List of Tables V List of Figures VI AcknowledgementElle SanchezPas encore d'évaluation

- A Study On Problems and Prospects of Women Fish Vendors in RamanthuraiDocument4 pagesA Study On Problems and Prospects of Women Fish Vendors in RamanthuraiInternational Journal of Application or Innovation in Engineering & Management100% (1)

- Research Plan On Efficacy of Facebook To The Online Sellers 2Document14 pagesResearch Plan On Efficacy of Facebook To The Online Sellers 2Bea OrculloPas encore d'évaluation

- Case No 2 Jollibee The Force Within The Empire2Document13 pagesCase No 2 Jollibee The Force Within The Empire2Eva DutolloPas encore d'évaluation

- Management Quiz BowlDocument53 pagesManagement Quiz BowlFaye ColasPas encore d'évaluation

- Bus Ethics AS 5 Belief SystemDocument4 pagesBus Ethics AS 5 Belief SystemEvangeline AgtarapPas encore d'évaluation

- M1Document14 pagesM1Princess SilencePas encore d'évaluation

- Las-Business-Finance-Q1 Week 1Document16 pagesLas-Business-Finance-Q1 Week 1Kinn Jay100% (1)

- Opportunities Atractiveness MatrixDocument9 pagesOpportunities Atractiveness MatrixEliPas encore d'évaluation

- Questions Bsba Quiz BeeDocument5 pagesQuestions Bsba Quiz BeeMaria Charise TongolPas encore d'évaluation

- Unwed Mothers and Illegitimate ChildrenDocument15 pagesUnwed Mothers and Illegitimate ChildrenKeith Corpuz Largo100% (1)

- Stability RatioDocument27 pagesStability RatioashokkeeliPas encore d'évaluation

- AbstractDocument1 pageAbstractEricka ChoncePas encore d'évaluation

- Bsba Theses Results 2018Document6 pagesBsba Theses Results 2018api-194241825Pas encore d'évaluation

- TricycleDocument10 pagesTricyclechancer01Pas encore d'évaluation

- MR - Loyalty-Cards-Chapter 1-4Document56 pagesMR - Loyalty-Cards-Chapter 1-4Krisel Ibanez50% (2)

- Review of Related Literature FinalDocument5 pagesReview of Related Literature Finaljazbutuyan1997100% (1)

- Bauan Technical High School Senior High School: The Study Aimed To Determine The Effects of Relationship To The AcademicDocument10 pagesBauan Technical High School Senior High School: The Study Aimed To Determine The Effects of Relationship To The AcademicPrincess Lheakyrie Casilao0% (1)

- Level of Motivation Among The Lgu Personnel in The Municipality of IguigDocument3 pagesLevel of Motivation Among The Lgu Personnel in The Municipality of IguigPrincess Liban Rumusud100% (1)

- AlfamartDocument4 pagesAlfamartYulianaXiePas encore d'évaluation

- Chapter 1 Intro Fin MGTDocument49 pagesChapter 1 Intro Fin MGTMelissa BattadPas encore d'évaluation

- Philippine Debt FPVICLARDocument15 pagesPhilippine Debt FPVICLARenaportillo13Pas encore d'évaluation

- MarketDocument30 pagesMarketFlori May Casakit100% (1)

- RRL For Students SatisfactionDocument2 pagesRRL For Students SatisfactionCamille EboraPas encore d'évaluation

- OM Narrative ReportDocument9 pagesOM Narrative ReportJinx Cyrus RodilloPas encore d'évaluation

- EFO705 Master Thesis: Multi Level Marketing Products in ThailandDocument63 pagesEFO705 Master Thesis: Multi Level Marketing Products in ThailandLindy Lou YamiloPas encore d'évaluation

- Defense Proposal Presentation GuideDocument29 pagesDefense Proposal Presentation GuideLindy Lou YamiloPas encore d'évaluation

- Eunsoo 1Document122 pagesEunsoo 1Lindy Lou YamiloPas encore d'évaluation

- Customer Satisfaction of Landbank of The Philippines and Banco de Oro in Terms of Car Loan Services in Surigao CityDocument16 pagesCustomer Satisfaction of Landbank of The Philippines and Banco de Oro in Terms of Car Loan Services in Surigao CityLindy Lou YamiloPas encore d'évaluation

- "The Research, Risks and Rewards": Multilevel MarketingDocument8 pages"The Research, Risks and Rewards": Multilevel MarketingLindy Lou YamiloPas encore d'évaluation

- Yamilo & Morial ThesisDocument30 pagesYamilo & Morial ThesisLindy Lou YamiloPas encore d'évaluation

- AARP Foundation MLM Research Study Report 10.8.18Document40 pagesAARP Foundation MLM Research Study Report 10.8.18Lindy Lou Yamilo100% (1)

- Cartus Receipt GuideDocument4 pagesCartus Receipt Guideilaria zaccagniniPas encore d'évaluation

- XXXX XXXX XXXX 5026: Han Cai Account Number: XXXX XXXX XXXX 5026 Closing Date: September 2, 2023Document4 pagesXXXX XXXX XXXX 5026: Han Cai Account Number: XXXX XXXX XXXX 5026 Closing Date: September 2, 2023finape6897Pas encore d'évaluation

- Report of The Commission of Inquiry On Mrs A. Gurib-Fakim, Former President of The RepublicDocument418 pagesReport of The Commission of Inquiry On Mrs A. Gurib-Fakim, Former President of The RepublicLe MauricienPas encore d'évaluation

- Licence Controller QualificationDocument2 pagesLicence Controller QualificationJessie Booth0% (1)

- Acs Access To Cash - Financial Services and Markets BillDocument2 pagesAcs Access To Cash - Financial Services and Markets BillAhmed EssalhiPas encore d'évaluation

- LUMS Sports VouchersDocument1 pageLUMS Sports VouchersOmer ZahidPas encore d'évaluation

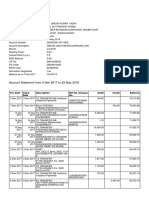

- Account Statement From 3 Nov 2017 To 23 May 2018: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument4 pagesAccount Statement From 3 Nov 2017 To 23 May 2018: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceUMESH KUMAR YadavPas encore d'évaluation

- Mju TVi 0 H RIa VPD 3 CDocument5 pagesMju TVi 0 H RIa VPD 3 CPallaviPas encore d'évaluation

- Hawaii Data PrivacyDocument52 pagesHawaii Data PrivacythecoffeecanPas encore d'évaluation

- SMTH Grade 6 AAC Public OverviewDocument14 pagesSMTH Grade 6 AAC Public OverviewAshleyPas encore d'évaluation

- Avantive Corp ERDsDocument4 pagesAvantive Corp ERDsJohn KimPas encore d'évaluation

- Credit Card Mandate FormDocument2 pagesCredit Card Mandate FormDivya SharmaPas encore d'évaluation

- Airtel Bill PDFDocument13 pagesAirtel Bill PDFsourabhPas encore d'évaluation

- PTE Repeated EssaysDocument31 pagesPTE Repeated EssaysMuhammad SohailPas encore d'évaluation

- Comparative Analysis of Direct Banking Services of Kotak With Other BanksDocument105 pagesComparative Analysis of Direct Banking Services of Kotak With Other Bankssuruchiathavale221234Pas encore d'évaluation

- Saraswat Bank Full & FinalDocument15 pagesSaraswat Bank Full & FinalPratik RevankarPas encore d'évaluation

- Key BtapDocument11 pagesKey BtapViệt Phương NguyễnPas encore d'évaluation

- CCD MID/Declaration: Application DetailsDocument1 pageCCD MID/Declaration: Application DetailsSuryateja ArangiPas encore d'évaluation

- Your 9mobile Bill Statement: MR Kpanja MichaelDocument3 pagesYour 9mobile Bill Statement: MR Kpanja MichaelSpikePas encore d'évaluation

- Experience The Luxury With Atlantis The Palm & DoubleTree by Hilton - Invoice PDFDocument6 pagesExperience The Luxury With Atlantis The Palm & DoubleTree by Hilton - Invoice PDFZesty ZeeshanPas encore d'évaluation

- PRPC Information BookletDocument21 pagesPRPC Information BookletCamille Andrea TesoroPas encore d'évaluation

- Estmt - 2016 08 31 PDFDocument4 pagesEstmt - 2016 08 31 PDFAnonymous dVQ61xYPas encore d'évaluation

- Topic 8 - Receivable Financing - Rev (Students)Document37 pagesTopic 8 - Receivable Financing - Rev (Students)Romzi100% (1)

- MAS 12 Working Capital Management MAS 12 Working Capital ManagementDocument11 pagesMAS 12 Working Capital Management MAS 12 Working Capital ManagementiBEAYPas encore d'évaluation

- About Card Payments Regulation - Questions & Answers RBADocument12 pagesAbout Card Payments Regulation - Questions & Answers RBASamPas encore d'évaluation

- Title Payment Auth FormDocument1 pageTitle Payment Auth FormSpamchurchPas encore d'évaluation

- Fictitious Business NamesDocument4 pagesFictitious Business NamesPawPaul MccoyPas encore d'évaluation

- FARAP 4702 ReceivablesDocument8 pagesFARAP 4702 Receivablesliberace cabreraPas encore d'évaluation

- E-Commerce Glossary PDFDocument5 pagesE-Commerce Glossary PDFwefWEPas encore d'évaluation

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamD'EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamPas encore d'évaluation

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialD'EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialPas encore d'évaluation

- The Value of a Whale: On the Illusions of Green CapitalismD'EverandThe Value of a Whale: On the Illusions of Green CapitalismÉvaluation : 5 sur 5 étoiles5/5 (2)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaD'EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaÉvaluation : 3.5 sur 5 étoiles3.5/5 (8)

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthD'EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthÉvaluation : 4 sur 5 étoiles4/5 (20)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSND'Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNÉvaluation : 4.5 sur 5 étoiles4.5/5 (3)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaD'EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (14)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successD'EverandReady, Set, Growth hack:: A beginners guide to growth hacking successÉvaluation : 4.5 sur 5 étoiles4.5/5 (93)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialD'EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialÉvaluation : 4.5 sur 5 étoiles4.5/5 (32)

- Creating Shareholder Value: A Guide For Managers And InvestorsD'EverandCreating Shareholder Value: A Guide For Managers And InvestorsÉvaluation : 4.5 sur 5 étoiles4.5/5 (8)

- An easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyD'EverandAn easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyÉvaluation : 3 sur 5 étoiles3/5 (1)

- Corporate Finance Formulas: A Simple IntroductionD'EverandCorporate Finance Formulas: A Simple IntroductionÉvaluation : 4 sur 5 étoiles4/5 (8)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingD'EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingÉvaluation : 4.5 sur 5 étoiles4.5/5 (17)

- The Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceD'EverandThe Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceÉvaluation : 4 sur 5 étoiles4/5 (1)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisD'EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisÉvaluation : 5 sur 5 étoiles5/5 (6)

- Mastering the VC Game: A Venture Capital Insider Reveals How to Get from Start-up to IPO on Your TermsD'EverandMastering the VC Game: A Venture Capital Insider Reveals How to Get from Start-up to IPO on Your TermsÉvaluation : 4.5 sur 5 étoiles4.5/5 (21)

- Value: The Four Cornerstones of Corporate FinanceD'EverandValue: The Four Cornerstones of Corporate FinanceÉvaluation : 5 sur 5 étoiles5/5 (2)

- Product-Led Growth: How to Build a Product That Sells ItselfD'EverandProduct-Led Growth: How to Build a Product That Sells ItselfÉvaluation : 5 sur 5 étoiles5/5 (1)

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorD'EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorPas encore d'évaluation

- Finance Basics (HBR 20-Minute Manager Series)D'EverandFinance Basics (HBR 20-Minute Manager Series)Évaluation : 4.5 sur 5 étoiles4.5/5 (32)

- Financial Leadership for Nonprofit Executives: Guiding Your Organization to Long-Term SuccessD'EverandFinancial Leadership for Nonprofit Executives: Guiding Your Organization to Long-Term SuccessÉvaluation : 4 sur 5 étoiles4/5 (2)

- Mind over Money: The Psychology of Money and How to Use It BetterD'EverandMind over Money: The Psychology of Money and How to Use It BetterÉvaluation : 4 sur 5 étoiles4/5 (24)

- YouTube Marketing: Comprehensive Beginners Guide to Learn YouTube Marketing, Tips & Secrets to Growth Hacking Your Channel and Building Profitable Passive Income Business OnlineD'EverandYouTube Marketing: Comprehensive Beginners Guide to Learn YouTube Marketing, Tips & Secrets to Growth Hacking Your Channel and Building Profitable Passive Income Business OnlineÉvaluation : 4.5 sur 5 étoiles4.5/5 (2)

- The Illusion of Innovation: Escape "Efficiency" and Unleash Radical ProgressD'EverandThe Illusion of Innovation: Escape "Efficiency" and Unleash Radical ProgressPas encore d'évaluation