Vous aimerez peut-être aussi

- Assessing The ERP-SAP Implementation Strategy From Cultural PerspectivesDocument8 pagesAssessing The ERP-SAP Implementation Strategy From Cultural PerspectivesAbad AbanasPas encore d'évaluation

- Leveraging Business ArchitecDocument15 pagesLeveraging Business ArchitecAbad Abanas100% (1)

- Designing Digital Public Service Supply Chains: Four Country-Based Cases in Criminal JusticeDocument29 pagesDesigning Digital Public Service Supply Chains: Four Country-Based Cases in Criminal JusticeAbad AbanasPas encore d'évaluation

- Programme Afrique Numerique Eng 11016Document2 pagesProgramme Afrique Numerique Eng 11016Abad AbanasPas encore d'évaluation

- Vebuka PROJECT REPORT ON RECRUITMENT AND SELECTION PROCESS IN AN IT ORGANIZATION PDFDocument102 pagesVebuka PROJECT REPORT ON RECRUITMENT AND SELECTION PROCESS IN AN IT ORGANIZATION PDFAbad AbanasPas encore d'évaluation

- Transformation On Your Terms and Your Timeline.: Wherever You Are, Wherever You Want To BeDocument1 pageTransformation On Your Terms and Your Timeline.: Wherever You Are, Wherever You Want To BeAbad AbanasPas encore d'évaluation

- Process Mapping For Risk ManagementDocument2 pagesProcess Mapping For Risk ManagementAbad AbanasPas encore d'évaluation

- Project ManagementDocument51 pagesProject ManagementAbad AbanasPas encore d'évaluation

- Machine Learning The Art and Science of AlgorithmsDocument416 pagesMachine Learning The Art and Science of AlgorithmsAbad AbanasPas encore d'évaluation

- Lean Industry4.0Document11 pagesLean Industry4.0Abad Abanas0% (1)

- Atos Look Out UtilitiesDocument8 pagesAtos Look Out UtilitiesAbad AbanasPas encore d'évaluation

- Business Intelligence: Technology and Career OptionsDocument19 pagesBusiness Intelligence: Technology and Career OptionsAbad AbanasPas encore d'évaluation

- Fraud Risk Management Strategy Prevention and DetectionDocument48 pagesFraud Risk Management Strategy Prevention and DetectionAbad AbanasPas encore d'évaluation

- BI Dashboard Design Common PitfallsDocument31 pagesBI Dashboard Design Common PitfallsnivedithPas encore d'évaluation

- Management Assessment of Internal ControlsDocument1 pageManagement Assessment of Internal ControlsAbad AbanasPas encore d'évaluation

- Tìm Hiểu Về KSNBDocument21 pagesTìm Hiểu Về KSNBTrần Văn TẹoPas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (120)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- An Assessment of Internal Control Over Inventory of Merchandizing CompanyDocument34 pagesAn Assessment of Internal Control Over Inventory of Merchandizing CompanyTamirat Hailu100% (5)

- Pelaksanaan Program Pembinaan Koperasi Usaha Mikro Kecil Dan Menengah (Umkm)Document7 pagesPelaksanaan Program Pembinaan Koperasi Usaha Mikro Kecil Dan Menengah (Umkm)Razief Firdaus 043Pas encore d'évaluation

- Avon Calls On Foreign Markets APA 3 PagesDocument6 pagesAvon Calls On Foreign Markets APA 3 PagesSabika NaqviPas encore d'évaluation

- Cost Sheet Practical ProblemsDocument2 pagesCost Sheet Practical Problemssameer_kini100% (1)

- THOUFIQ Resume MbaDocument3 pagesTHOUFIQ Resume MbanaveenPas encore d'évaluation

- Erp System Architecture PDFDocument2 pagesErp System Architecture PDFPamela0% (2)

- Exposure Management 2.0 - SAP BlogsDocument8 pagesExposure Management 2.0 - SAP Blogsapostolos thomasPas encore d'évaluation

- Capturing Marketing Insights: 1. Collecting Information and Forecasting DemandDocument64 pagesCapturing Marketing Insights: 1. Collecting Information and Forecasting DemandNandan Choudhary100% (1)

- Domestic Marketing Vs International MarketingDocument6 pagesDomestic Marketing Vs International MarketingAnju MuruganPas encore d'évaluation

- The Possibility of Getting A Job in The United Arab EmiratesDocument2 pagesThe Possibility of Getting A Job in The United Arab EmiratessuvarnarajedoliPas encore d'évaluation

- Cash Flow statement-AFMDocument27 pagesCash Flow statement-AFMRishad kPas encore d'évaluation

- BFIN300 Full Hands OutDocument46 pagesBFIN300 Full Hands OutGauray LionPas encore d'évaluation

- Online Demo Session - FICO - 14 April 2021Document48 pagesOnline Demo Session - FICO - 14 April 2021Md Mukul HossainPas encore d'évaluation

- Start Your Start Up (Answer)Document5 pagesStart Your Start Up (Answer)Kushal AgarwalPas encore d'évaluation

- Yvette Cyprian ElewaDocument5 pagesYvette Cyprian Elewaapi-535701983Pas encore d'évaluation

- 3464172Document34 pages3464172Aasri RPas encore d'évaluation

- Jill Barad's CaseDocument3 pagesJill Barad's Case{OK}Pas encore d'évaluation

- Danielle Simpson ResumeDocument1 pageDanielle Simpson Resumeapi-413439815Pas encore d'évaluation

- All VouchersDocument23 pagesAll VouchersSunandaPas encore d'évaluation

- Nike PresentationsDocument54 pagesNike PresentationsSubhan AhmedPas encore d'évaluation

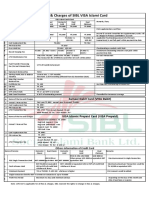

- Fees and Charges of SIBL Islami CardDocument1 pageFees and Charges of SIBL Islami CardMd YusufPas encore d'évaluation

- Accounting For Decentralized Operations: Inventory at Cost of P40,000Document6 pagesAccounting For Decentralized Operations: Inventory at Cost of P40,000Nicole Allyson AguantaPas encore d'évaluation

- OpenSAP s4h11 Week 2 TranscriptDocument34 pagesOpenSAP s4h11 Week 2 TranscriptUmar FarooqPas encore d'évaluation

- ITC PSPD, Kovai (Coimbatore) : QuestionnairesDocument4 pagesITC PSPD, Kovai (Coimbatore) : QuestionnairesJohn LukosePas encore d'évaluation

- ASSOCHAM BSDC Professional Support Memebrship - Application Form & AdvantagesDocument2 pagesASSOCHAM BSDC Professional Support Memebrship - Application Form & AdvantagesneerajPas encore d'évaluation

- Nptel: TopicDocument104 pagesNptel: TopicRAJAT . 20GSOB1010459Pas encore d'évaluation

- Chapter 8Document17 pagesChapter 8Meo XinkPas encore d'évaluation

- 2020 Walmart Annual ReportDocument88 pages2020 Walmart Annual ReportPruthviraj DhinganiPas encore d'évaluation

- P1 Exams Set ADocument10 pagesP1 Exams Set Aerica lamsenPas encore d'évaluation