Vous aimerez peut-être aussi

- ABC Additional Examples Sol.Document2 pagesABC Additional Examples Sol.Shivani MunotPas encore d'évaluation

- Data Session 6Document9 pagesData Session 6Shivani MunotPas encore d'évaluation

- NucorDocument2 pagesNucorShivani MunotPas encore d'évaluation

- Analyses of Sector-Specific Levers That Drive Company - 1556862325Document17 pagesAnalyses of Sector-Specific Levers That Drive Company - 1556862325Shivani MunotPas encore d'évaluation

- Financial Formulas - Ratios (Sheet)Document3 pagesFinancial Formulas - Ratios (Sheet)carmo-netoPas encore d'évaluation

- Sequoia Pitch Deck-1553447010 PDFDocument12 pagesSequoia Pitch Deck-1553447010 PDFLakshmi100% (3)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- CAMY - RelaunchDocument26 pagesCAMY - RelaunchHabib Ul HaquePas encore d'évaluation

- GURPS 4e - (Unofficial) Adventure Deathnight PDFDocument21 pagesGURPS 4e - (Unofficial) Adventure Deathnight PDFBruno CelhoPas encore d'évaluation

- Doddle Product Brochure - 2020 PDFDocument9 pagesDoddle Product Brochure - 2020 PDFDavor BudimirPas encore d'évaluation

- Samsung - Consumer AnalysisDocument23 pagesSamsung - Consumer Analysisgrover_swati50% (2)

- How the Marketing Mix Concept Needs to be Radically Reformed for the Digital AgeDocument68 pagesHow the Marketing Mix Concept Needs to be Radically Reformed for the Digital AgevaibhavPas encore d'évaluation

- Bi - 17ubi411 Marketing Management PDFDocument31 pagesBi - 17ubi411 Marketing Management PDFSimmiPas encore d'évaluation

- Google Glass Hbs CaseDocument3 pagesGoogle Glass Hbs CaseEric0% (1)

- Unit 5 MM Students NotesDocument26 pagesUnit 5 MM Students NotesN.NevethanPas encore d'évaluation

- B014 The Resilient EnterpriseDocument10 pagesB014 The Resilient EnterpriseShubhangi TerapanthiPas encore d'évaluation

- Case Synopsis Section-A AquatredDocument5 pagesCase Synopsis Section-A AquatredAggyapal Singh JimmyPas encore d'évaluation

- Customer Satisfaction For PantaloonsDocument13 pagesCustomer Satisfaction For PantaloonsDinesh SinghPas encore d'évaluation

- Questionnaire On Customer Satisfaction at Reliance RetailDocument4 pagesQuestionnaire On Customer Satisfaction at Reliance RetailPragya Singh Baghel100% (1)

- One Page Write Up On Recommended Strategy . .8Document8 pagesOne Page Write Up On Recommended Strategy . .8Arka BosePas encore d'évaluation

- Strategies and Practices for Loyalty ProgramsDocument32 pagesStrategies and Practices for Loyalty ProgramsShriram DawkharPas encore d'évaluation

- Case AnalysisDocument23 pagesCase AnalysisKlaus AlmesPas encore d'évaluation

- Honda Internship Report (Marketing) .Document61 pagesHonda Internship Report (Marketing) .naresh0% (2)

- Newsvendor Tackle ProblemDocument13 pagesNewsvendor Tackle ProblemPunit MaheshwariPas encore d'évaluation

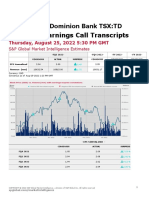

- The Toronto-Dominion Bank, Q3 2022 Earnings Call, Aug 25, 2022Document23 pagesThe Toronto-Dominion Bank, Q3 2022 Earnings Call, Aug 25, 2022Neel DoshiPas encore d'évaluation

- Start An Online Grocery StoreDocument27 pagesStart An Online Grocery StoreMuzically InspiredPas encore d'évaluation

- 1) Identify Mcdonald'S "Seven Major InnovationsDocument3 pages1) Identify Mcdonald'S "Seven Major InnovationsAh ChaiPas encore d'évaluation

- Luxury Sharing, Meet High FashionDocument16 pagesLuxury Sharing, Meet High FashionnemonPas encore d'évaluation

- The Body Shop: Mission Statement: "A Company With A Difference" and The Reason For BeingDocument10 pagesThe Body Shop: Mission Statement: "A Company With A Difference" and The Reason For BeingRijul KarkiPas encore d'évaluation

- Pune-The Leading Real Estate Destination-2012-13Document78 pagesPune-The Leading Real Estate Destination-2012-13Vishal TripathiPas encore d'évaluation

- Customer Brand Switching from OMFED MilkDocument65 pagesCustomer Brand Switching from OMFED MilkDisha ChiraniaPas encore d'évaluation

- QFD Online RetailingDocument18 pagesQFD Online RetailingChintan SinghviPas encore d'évaluation

- Toys R Us Digital Marketing AssignmentDocument28 pagesToys R Us Digital Marketing AssignmentDavid Shadrach ChandraPas encore d'évaluation

- Employee DiscountsDocument2 pagesEmployee DiscountsBlake Griffin100% (1)

- CVBK (LSE)Document178 pagesCVBK (LSE)vincentyouPas encore d'évaluation

- SMU Project GuidelinesDocument19 pagesSMU Project Guidelinesprinceramji90100% (1)

- 14.160.market Basket - Ton.Kochan - FINAL PDFDocument28 pages14.160.market Basket - Ton.Kochan - FINAL PDFPatricia CoyPas encore d'évaluation