Vous aimerez peut-être aussi

- Knowledge AAA p7Document15 pagesKnowledge AAA p7PfuhadPas encore d'évaluation

- AAA Pass 68% 05122022Document74 pagesAAA Pass 68% 05122022Financial ConsultingPas encore d'évaluation

- Contoh SoalDocument4 pagesContoh SoalRico Danu JatmikoPas encore d'évaluation

- Name: Christine Ndanu ADMISSION NO: BBM/2041 /18 Unit: Total Quality in Supply Chain Management Unit Code: BBM 445 Assignment: CatDocument4 pagesName: Christine Ndanu ADMISSION NO: BBM/2041 /18 Unit: Total Quality in Supply Chain Management Unit Code: BBM 445 Assignment: CatHashi MohamedPas encore d'évaluation

- MGT Op Audit, Internal AuditDocument4 pagesMGT Op Audit, Internal AuditNiket SharmaPas encore d'évaluation

- Answers To Workshop 1Document5 pagesAnswers To Workshop 1Nur Elina YurnalisPas encore d'évaluation

- Quality Management (QM) : The 4 Assignment of Acting As A T.LDocument36 pagesQuality Management (QM) : The 4 Assignment of Acting As A T.Lbajista0127Pas encore d'évaluation

- Benefits of An Audit System QARDocument6 pagesBenefits of An Audit System QARMarynissa CatibogPas encore d'évaluation

- Webinar 1: Planning The Audit in The Pandemic Environment: Summary of Key TakeawaysDocument5 pagesWebinar 1: Planning The Audit in The Pandemic Environment: Summary of Key TakeawaysSandro BonillaPas encore d'évaluation

- Summative 1 - 94 Over 100Document9 pagesSummative 1 - 94 Over 100Von Andrei MedinaPas encore d'évaluation

- Audit and Assurance ReportDocument4 pagesAudit and Assurance ReportLovely Jane Raut CabiltoPas encore d'évaluation

- Acct 151Document44 pagesAcct 151Justin RoisPas encore d'évaluation

- 7.QA MaintainanceDocument17 pages7.QA MaintainancePrincy PandeyPas encore d'évaluation

- New 27456Document60 pagesNew 27456Lovely Jane Raut CabiltoPas encore d'évaluation

- Quality Control P7Document37 pagesQuality Control P7Godfrey AlemaoPas encore d'évaluation

- Auditing Theory Answer Key 1Document197 pagesAuditing Theory Answer Key 1AngelUmayam100% (2)

- QADocument117 pagesQANikhil ArtPas encore d'évaluation

- Group 2 A1 Audit Process Accepting An EngagementDocument17 pagesGroup 2 A1 Audit Process Accepting An EngagementGlenn AnitanPas encore d'évaluation

- Chapter 6 - Stages of An Audit - AppointmentDocument5 pagesChapter 6 - Stages of An Audit - AppointmentTalamoon NishaPas encore d'évaluation

- What Is An Audit Committee? Discuss Its Value in An OrganizationDocument6 pagesWhat Is An Audit Committee? Discuss Its Value in An Organizationjoyce KimPas encore d'évaluation

- Guidance On INTERNAL AUDITSDocument7 pagesGuidance On INTERNAL AUDITSdhir.ankurPas encore d'évaluation

- Assigment QMSADocument3 pagesAssigment QMSAuya lyaaPas encore d'évaluation

- Module 4 - Business Management Techniques and Impact On ControlDocument4 pagesModule 4 - Business Management Techniques and Impact On ControlLysss EpssssPas encore d'évaluation

- Ac19 Module 4 - DGCDocument19 pagesAc19 Module 4 - DGCMaricar PinedaPas encore d'évaluation

- Ass CH02Document20 pagesAss CH02shah newazPas encore d'évaluation

- Services Marketing Unit Iv-Part-1Document23 pagesServices Marketing Unit Iv-Part-1vikramadk1404Pas encore d'évaluation

- FINAL - Audit Report - RAJEEV KUMARDocument4 pagesFINAL - Audit Report - RAJEEV KUMARRajeev KumarPas encore d'évaluation

- Auditing Theory (Cabrera) Answer KeyDocument198 pagesAuditing Theory (Cabrera) Answer KeyCazia Mei Jover83% (12)

- Client Acceptance and ContinuanceDocument7 pagesClient Acceptance and ContinuanceGina100% (1)

- Managing The Quality of Consulting EngagementsDocument32 pagesManaging The Quality of Consulting EngagementsCedric Legaspi TagalaPas encore d'évaluation

- 004 - CAASSST07 - CH02 - Amndd Final BW+HS - RP2 - Sec - noPWDocument20 pages004 - CAASSST07 - CH02 - Amndd Final BW+HS - RP2 - Sec - noPWMahediPas encore d'évaluation

- Lesson Number: 01 Topic: Fundamentals of Assurance Services Learning ObjectivesDocument19 pagesLesson Number: 01 Topic: Fundamentals of Assurance Services Learning ObjectivesDavid alfonsoPas encore d'évaluation

- Information Systems Auditing: The IS Audit Follow-up ProcessD'EverandInformation Systems Auditing: The IS Audit Follow-up ProcessÉvaluation : 2 sur 5 étoiles2/5 (1)

- Notes For Part 6Document5 pagesNotes For Part 6Anonymous smFxIR07Pas encore d'évaluation

- Resource Tool Customer Care FinalDocument6 pagesResource Tool Customer Care FinalMohammed Abdul MukarramPas encore d'évaluation

- Comprehensive Manual of Internal Audit Practice and Guide: The Most Practical Guide to Internal Auditing PracticeD'EverandComprehensive Manual of Internal Audit Practice and Guide: The Most Practical Guide to Internal Auditing PracticeÉvaluation : 5 sur 5 étoiles5/5 (1)

- Awareness Session On ISO 9001-2015 (1) .PpsDocument22 pagesAwareness Session On ISO 9001-2015 (1) .Ppssumana paul50% (2)

- OMNI Newsletter IV 2020Document4 pagesOMNI Newsletter IV 2020Fernando MariñoPas encore d'évaluation

- APPLIED AUDITING Module 1Document3 pagesAPPLIED AUDITING Module 1Paul Fajardo CanoyPas encore d'évaluation

- Business Front To Back Process and ControlsDocument12 pagesBusiness Front To Back Process and ControlsCharles SantosPas encore d'évaluation

- Jawaban CG TM 7Document11 pagesJawaban CG TM 7Krisna ArisaPas encore d'évaluation

- FOURDocument4 pagesFOURRandy ManzanoPas encore d'évaluation

- Quality ManagementDocument5 pagesQuality ManagementLarain MirandaPas encore d'évaluation

- Audit Cover Summary PageDocument12 pagesAudit Cover Summary PageJoe EleanPas encore d'évaluation

- During My Training PeriodDocument5 pagesDuring My Training PeriodVijay BhattaraiPas encore d'évaluation

- Auditing and Assurance Services 4th Edition Louwers Solutions ManualDocument35 pagesAuditing and Assurance Services 4th Edition Louwers Solutions Manualepithiteadulatoryxrams0100% (34)

- Quality Management System ModuleDocument181 pagesQuality Management System ModuleJhonrick MagtibayPas encore d'évaluation

- Dwnload Full Auditing and Assurance Services 4th Edition Louwers Solutions Manual PDFDocument35 pagesDwnload Full Auditing and Assurance Services 4th Edition Louwers Solutions Manual PDFmutevssarahm100% (14)

- XXX AT ExxM ACTIVITYDocument2 pagesXXX AT ExxM ACTIVITYDiane LorenzoPas encore d'évaluation

- ACTIVITY 6-Paghid, Avelino Jr.-Pcbet-20-501eDocument4 pagesACTIVITY 6-Paghid, Avelino Jr.-Pcbet-20-501eChesca GonzalesPas encore d'évaluation

- CH 01 PARAMDocument14 pagesCH 01 PARAMpankajgopalsharmaPas encore d'évaluation

- Exam by MuhammadDocument8 pagesExam by Muhammadazhar ishaqPas encore d'évaluation

- Audit ReportsDocument64 pagesAudit ReportsNatali SanchezPas encore d'évaluation

- Basic Concepts of QualityDocument34 pagesBasic Concepts of QualityrohitcshettyPas encore d'évaluation

- Written ReportDocument10 pagesWritten ReportPenamante EvitaPas encore d'évaluation

- (REPORT) CHAPTER 9 - Risk Assessment Part 1Document12 pages(REPORT) CHAPTER 9 - Risk Assessment Part 1Jnn Cyc100% (1)

- PSBA - GAAS and System of Quality ControlDocument10 pagesPSBA - GAAS and System of Quality ControlephraimPas encore d'évaluation

- Auditing and Assurance Services 15th Edition Arens Solutions ManualDocument35 pagesAuditing and Assurance Services 15th Edition Arens Solutions Manualepithiteadulatoryxrams0100% (13)

- Cash ReviewerDocument35 pagesCash ReviewerAprile AnonuevoPas encore d'évaluation

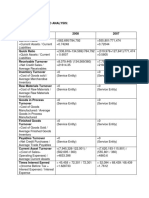

- Ratio Analysis SampleDocument3 pagesRatio Analysis SampleAprile AnonuevoPas encore d'évaluation

- Literature in The PhilippinesDocument9 pagesLiterature in The PhilippinesAprile AnonuevoPas encore d'évaluation

- 3) Psa 210 - Agreeing The Terms of Audit EngagementsDocument1 page3) Psa 210 - Agreeing The Terms of Audit EngagementsAprile AnonuevoPas encore d'évaluation

- Cost Concepts and TerminologiesDocument13 pagesCost Concepts and TerminologiesAprile AnonuevoPas encore d'évaluation

- Accountancy LawDocument6 pagesAccountancy LawAprile AnonuevoPas encore d'évaluation

- Assertion SummaryDocument3 pagesAssertion SummaryAprile AnonuevoPas encore d'évaluation

- Tower and TowerDocument6 pagesTower and TowerAprile AnonuevoPas encore d'évaluation

- 07 Test ADocument24 pages07 Test ARashmin ShetPas encore d'évaluation

- Managerial LEADERSHIP P WrightDocument5 pagesManagerial LEADERSHIP P WrighttomorPas encore d'évaluation

- Ei GSM IcbDocument11 pagesEi GSM IcbwimaxaaabglPas encore d'évaluation

- Computer ProfessionalDocument185 pagesComputer ProfessionalSHAHSYADPas encore d'évaluation

- Glor - Io Wall HackDocument889 pagesGlor - Io Wall HackAnonymous z3tLNO0TqH50% (8)

- Communication Skills For Doctors PDFDocument2 pagesCommunication Skills For Doctors PDFJenny50% (2)

- Parts of The Microscope Quiz PDFDocument2 pagesParts of The Microscope Quiz PDFEnriele De GuzmanPas encore d'évaluation

- 2nd Summative Test - Org'n & Mgt. 2nd SemesterDocument4 pages2nd Summative Test - Org'n & Mgt. 2nd SemesterDo FernanPas encore d'évaluation

- Elementary Statistics A Step by Step Approach 7th Edition Bluman Test BankDocument14 pagesElementary Statistics A Step by Step Approach 7th Edition Bluman Test Bankfelicitycurtis9fhmt7100% (33)

- AA Metatron The Rays of Atlantian Knowledge and Rays of Healing Through Jim SelfDocument14 pagesAA Metatron The Rays of Atlantian Knowledge and Rays of Healing Through Jim SelfMeaghan Mathews100% (1)

- Maths Assessment Year 3 Term 3: Addition and Subtraction: NameDocument4 pagesMaths Assessment Year 3 Term 3: Addition and Subtraction: NamebayaPas encore d'évaluation

- Computer Graphics Lab Introduction To Opengl and Glut PrerequisitesDocument6 pagesComputer Graphics Lab Introduction To Opengl and Glut PrerequisitesNourhan M. NahnoushPas encore d'évaluation

- P6 Set Up Performance %Document10 pagesP6 Set Up Performance %Bryan JacksonPas encore d'évaluation

- Safety Training For The Oil and Gas Worker: WhitepaperDocument6 pagesSafety Training For The Oil and Gas Worker: WhitepaperfahdPas encore d'évaluation

- Course Outline BA301-2Document4 pagesCourse Outline BA301-2drugs_182Pas encore d'évaluation

- Bridge Embankment FailuresDocument13 pagesBridge Embankment Failuresirmreza68Pas encore d'évaluation

- Superconductivity - V. Ginzburg, E. Andryushin (World, 1994) WWDocument100 pagesSuperconductivity - V. Ginzburg, E. Andryushin (World, 1994) WWPhilip Ngem50% (2)

- The Machine Stops - The New YorkerDocument8 pagesThe Machine Stops - The New YorkermalvinaPas encore d'évaluation

- 2016/2017 Master Timetable (Tentative) : Published: May 2016Document19 pages2016/2017 Master Timetable (Tentative) : Published: May 2016Ken StaynerPas encore d'évaluation

- Keshav Mohaneesh Aumeer 16549793 Assignment 2 Case Study Managing Change 3002Document12 pagesKeshav Mohaneesh Aumeer 16549793 Assignment 2 Case Study Managing Change 3002pri demonPas encore d'évaluation

- Idemitsu - Super Multi Oil SeriesDocument2 pagesIdemitsu - Super Multi Oil SeriesarieprachmanPas encore d'évaluation

- Chapter-Wise Suggestion Paper: M201 MathematicsDocument6 pagesChapter-Wise Suggestion Paper: M201 MathematicsSoumodip ChakrabortyPas encore d'évaluation

- AR0001 Concept Design Rev ADocument28 pagesAR0001 Concept Design Rev AJulian JuniorPas encore d'évaluation

- Traditions of The North American Indians, Vol. 1 (Of 3) by Jones, James AthearnDocument125 pagesTraditions of The North American Indians, Vol. 1 (Of 3) by Jones, James AthearnGutenberg.org100% (2)

- Design of Machine Members - Syllabus PDFDocument3 pagesDesign of Machine Members - Syllabus PDFVAIBHAV TIWARIPas encore d'évaluation

- Hemu Kharel Kafle Paper On Drought in Mid and Far Western Nepal NASTDocument12 pagesHemu Kharel Kafle Paper On Drought in Mid and Far Western Nepal NASTArbind ShresthaPas encore d'évaluation

- Course 1 Unit 1 SEDocument80 pagesCourse 1 Unit 1 SEPrashant DhamdherePas encore d'évaluation

- English 9 DLPDocument6 pagesEnglish 9 DLPbeb100% (1)

- Them As Foreigners': Theme 2: OtherizationDocument3 pagesThem As Foreigners': Theme 2: OtherizationNastjaPas encore d'évaluation

- MSO EnglishDocument8 pagesMSO EnglishAgautam Agagan100% (1)