Vous aimerez peut-être aussi

- A) Commonly Used TDS Provision For Payments Made To Persons Resident in India (Individuals, Firms, Companies, Etc.)Document17 pagesA) Commonly Used TDS Provision For Payments Made To Persons Resident in India (Individuals, Firms, Companies, Etc.)Sonika GuptaPas encore d'évaluation

- TDS 3Document16 pagesTDS 3payal AgrawalPas encore d'évaluation

- Revised TDS Wef 14.05.20Document7 pagesRevised TDS Wef 14.05.20MANAN KOTHARIPas encore d'évaluation

- Accounts & Taxations Interview Related NotesDocument5 pagesAccounts & Taxations Interview Related NotesRahul Baburao AbhalePas encore d'évaluation

- Tds BookletDocument22 pagesTds BookletSanjayThakkarPas encore d'évaluation

- TDS - and - TCS Rate Chart 2024Document5 pagesTDS - and - TCS Rate Chart 2024Taxation KTPL (Kalyani Techpark Taxation)Pas encore d'évaluation

- TDS ChartDocument4 pagesTDS ChartjaoceelectricalPas encore d'évaluation

- TDS Rate Chart - FY 2021-22Document3 pagesTDS Rate Chart - FY 2021-22Ram YadavPas encore d'évaluation

- TDS (Tax Deducted at Source) Rate Chart For Financial Year 2010-11Document13 pagesTDS (Tax Deducted at Source) Rate Chart For Financial Year 2010-11av_meshramPas encore d'évaluation

- Tds Income Tax Rates Fy 2010-11Document13 pagesTds Income Tax Rates Fy 2010-11Surender KumarPas encore d'évaluation

- Tds Rate ChartDocument49 pagesTds Rate ChartSANJEEVPas encore d'évaluation

- TDS and TCS Rate Chart 2023Document5 pagesTDS and TCS Rate Chart 2023DEEPAK SHARMAPas encore d'évaluation

- TDS and TCS-rate-chart-2023 RemovedDocument4 pagesTDS and TCS-rate-chart-2023 Removeddurgeshsonawane65Pas encore d'évaluation

- TDS Rate ChartDocument2 pagesTDS Rate Chartshashi370Pas encore d'évaluation

- Tax Deducted at Source (TDS)Document7 pagesTax Deducted at Source (TDS)Rupali SinghPas encore d'évaluation

- Tax Deducted at Source UnitDocument13 pagesTax Deducted at Source Unitsatyanarayan dashPas encore d'évaluation

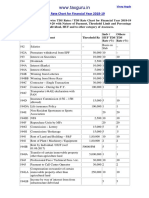

- WWW - Taxguru.in: TDS Rate Chart For Financial Year 2018-19Document1 pageWWW - Taxguru.in: TDS Rate Chart For Financial Year 2018-19Sunny NarangPas encore d'évaluation

- C.H. Padliya & Co.: Chartered AccountantsDocument11 pagesC.H. Padliya & Co.: Chartered AccountantsSarat KumarPas encore d'évaluation

- TDS Rates On Payments Other Than Salary and Wages To Residents (Including Domestic Companies)Document3 pagesTDS Rates On Payments Other Than Salary and Wages To Residents (Including Domestic Companies)Prince RaichandPas encore d'évaluation

- C.H. Padliya & Co.: Chartered AccountantsDocument6 pagesC.H. Padliya & Co.: Chartered AccountantsSarat KumarPas encore d'évaluation

- Tds - and - Tcs Rate Chart Fy 2019 20 TdsmanDocument2 pagesTds - and - Tcs Rate Chart Fy 2019 20 Tdsmankumar45caPas encore d'évaluation

- TDS - and - TCS Rate Chart 2025Document5 pagesTDS - and - TCS Rate Chart 2025jsparakhPas encore d'évaluation

- TdsPac RateCard 0910Document2 pagesTdsPac RateCard 0910Ebanezer PaulrajPas encore d'évaluation

- Rates of TDSDocument30 pagesRates of TDSsudhanshu88g1Pas encore d'évaluation

- C.H. Padliya & Co.: Chartered AccountantsDocument5 pagesC.H. Padliya & Co.: Chartered AccountantsSarat KumarPas encore d'évaluation

- TDS Rates and ReturnsDocument4 pagesTDS Rates and ReturnsMohanlal BishnoiPas encore d'évaluation

- Group 3 (Pallavi Sood)Document12 pagesGroup 3 (Pallavi Sood)abhimanyu_nikam6353Pas encore d'évaluation

- Changes in TDS Limits - F Y 2010-11Document1 pageChanges in TDS Limits - F Y 2010-11Ronak RanaPas encore d'évaluation

- What Is Tax Deducted at Source?Document5 pagesWhat Is Tax Deducted at Source?Bhagyashree SondagarPas encore d'évaluation

- 1.Tds, Tcs SummaryDocument5 pages1.Tds, Tcs SummaryKishore HariPas encore d'évaluation

- TDS (Tax Deducted at Source) Rate Chart For Financial Year 2010-11Document1 pageTDS (Tax Deducted at Source) Rate Chart For Financial Year 2010-11Shwetta GogawalePas encore d'évaluation

- Hand BookDocument82 pagesHand Booknmshamim7750Pas encore d'évaluation

- Ssra Tds Rates 2021-2022Document10 pagesSsra Tds Rates 2021-2022deepu kPas encore d'évaluation

- TDS Rate Chart For FY 2022-2023 (AY 2023-2024) Including Budget 2022 Amendments - Taxguru - inDocument15 pagesTDS Rate Chart For FY 2022-2023 (AY 2023-2024) Including Budget 2022 Amendments - Taxguru - inSachin GuptaPas encore d'évaluation

- TDS Rate Chart FY 2021-2022: Section Code Nature of Payment Threshold (In RS.) TDS Rate (In %) Indv/HUF OthersDocument7 pagesTDS Rate Chart FY 2021-2022: Section Code Nature of Payment Threshold (In RS.) TDS Rate (In %) Indv/HUF OthersRajPas encore d'évaluation

- Tax Deducted at Source - I: KPPM & AssociatesDocument63 pagesTax Deducted at Source - I: KPPM & AssociatesSaksham JoshiPas encore d'évaluation

- What Is TDS?: Tax Deducted at Source (TDS)Document8 pagesWhat Is TDS?: Tax Deducted at Source (TDS)Sandeep RajpootPas encore d'évaluation

- Tax Deducted at SourceDocument29 pagesTax Deducted at SourceChaitany Joshi0% (2)

- TDS Rate Chart 1Document1 pageTDS Rate Chart 1bulu1987Pas encore d'évaluation

- Form PDF 710378520091120Document7 pagesForm PDF 710378520091120asmita196Pas encore d'évaluation

- AX Educted at Ource - I: KPPM & AssociatesDocument67 pagesAX Educted at Ource - I: KPPM & AssociatesSaksham JoshiPas encore d'évaluation

- TDS TCSDocument231 pagesTDS TCSNarinderpal SinghPas encore d'évaluation

- Tds Calculator W.E.F. 1.10.09Document1 pageTds Calculator W.E.F. 1.10.09rajesh_vajjasPas encore d'évaluation

- Income TaxDocument77 pagesIncome TaxSachin KumarPas encore d'évaluation

- Tds Rate Chart Fy 2018-19 Ay 2019-20 Tds Deposit-Return Due Dates-Interest-PenaltyDocument2 pagesTds Rate Chart Fy 2018-19 Ay 2019-20 Tds Deposit-Return Due Dates-Interest-PenaltyNarayanakrishnan RPas encore d'évaluation

- C.H. Padliya & Co.: Chartered AccountantsDocument13 pagesC.H. Padliya & Co.: Chartered AccountantsSarat KumarPas encore d'évaluation

- TDS and TCS Rate Chart 2023Document3 pagesTDS and TCS Rate Chart 2023praveenPas encore d'évaluation

- All About TDS Part 2Document9 pagesAll About TDS Part 2Animesh Kumar TilakPas encore d'évaluation

- Tds Rate ChartDocument15 pagesTds Rate ChartJain MjPas encore d'évaluation

- Bhubaneswar 08112015 Session I PDFDocument42 pagesBhubaneswar 08112015 Session I PDFsachin NegiPas encore d'évaluation

- TDS Summary May 24Document2 pagesTDS Summary May 24Akil MalekPas encore d'évaluation

- TDS Rates Chart For Financial Year 2021 22 Assessment Year 2022 23 1Document5 pagesTDS Rates Chart For Financial Year 2021 22 Assessment Year 2022 23 1Audit ManifestPas encore d'évaluation

- Current Changes of TDS: Presented By, Ghanshyam WatekarDocument10 pagesCurrent Changes of TDS: Presented By, Ghanshyam Watekarpraful_watekarPas encore d'évaluation

- Intro of TdsDocument6 pagesIntro of Tdsshivani singhPas encore d'évaluation

- 1040 Exam Prep Module V: Adjustments to Income or DeductionsD'Everand1040 Exam Prep Module V: Adjustments to Income or DeductionsPas encore d'évaluation

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineD'EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LinePas encore d'évaluation

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesD'EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesPas encore d'évaluation

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisD'EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisPas encore d'évaluation

- Anti Money Laundering Policy 2016-17Document30 pagesAnti Money Laundering Policy 2016-17nagallanraoPas encore d'évaluation

- Settlemnt of Death Claims BoiDocument33 pagesSettlemnt of Death Claims BoinagallanraoPas encore d'évaluation

- Accounting Concepts & PrinciplesDocument29 pagesAccounting Concepts & PrinciplesnagallanraoPas encore d'évaluation

- D1 Explanatory NotesDocument11 pagesD1 Explanatory NotesnagallanraoPas encore d'évaluation

- Payment and Settlement System1Document6 pagesPayment and Settlement System1nagallanraoPas encore d'évaluation

- Profit and Loss Acccount Study MaterialDocument103 pagesProfit and Loss Acccount Study MaterialnagallanraoPas encore d'évaluation

- PML Act 2002Document8 pagesPML Act 2002nagallanraoPas encore d'évaluation

- Capital Expenditure & Revenue ExpenditureDocument5 pagesCapital Expenditure & Revenue ExpenditurenagallanraoPas encore d'évaluation

- Anti Money Laundering Policy 2016-17Document30 pagesAnti Money Laundering Policy 2016-17nagallanraoPas encore d'évaluation

- Mudra BankDocument26 pagesMudra BanknagallanraoPas encore d'évaluation

- Financing and Supporting Producer OrganisationsDocument12 pagesFinancing and Supporting Producer OrganisationsnagallanraoPas encore d'évaluation

- Prudential Systematic Withdrawal FormDocument6 pagesPrudential Systematic Withdrawal FormlukenowackiPas encore d'évaluation

- Billing Summary Customer Details: Total Amount Due (PKR) : 2,896Document1 pageBilling Summary Customer Details: Total Amount Due (PKR) : 2,896Rooh UllahPas encore d'évaluation

- Sample Exam QuestionsDocument7 pagesSample Exam QuestionsQian LuPas encore d'évaluation

- Ella Lyman Cabot Trust Question ListDocument2 pagesElla Lyman Cabot Trust Question ListAdeyemi Oluwaseun JohnPas encore d'évaluation

- PIN Certificate: This Is To Certify That Taxpayer Shown Herein Has Been Registered With Kenya Revenue AuthorityDocument1 pagePIN Certificate: This Is To Certify That Taxpayer Shown Herein Has Been Registered With Kenya Revenue AuthorityphillipPas encore d'évaluation

- Paywithtaxslip 102324 PDFDocument1 pagePaywithtaxslip 102324 PDFamitshrivastava154218Pas encore d'évaluation

- Wa0006.Document1 pageWa0006.Aun M RizviPas encore d'évaluation

- Module 1 - Transfer and Business Taxation - v.1Document30 pagesModule 1 - Transfer and Business Taxation - v.1John Vincent ManuelPas encore d'évaluation

- Kalyan Cost SheetDocument32 pagesKalyan Cost Sheetkjoshi_3Pas encore d'évaluation

- Practical Aspects - GST Annual ReturnDocument26 pagesPractical Aspects - GST Annual ReturnCA Shubhank SharmaPas encore d'évaluation

- Estimate / Quotation: Activity - Window CostingDocument1 pageEstimate / Quotation: Activity - Window CostingM.K. JaiswalPas encore d'évaluation

- 2022 TaxReturnDocument6 pages2022 TaxReturnLALLOUS KHOURY100% (3)

- Rann Utsav BrochureDocument11 pagesRann Utsav BrochureBhavin MehtaPas encore d'évaluation

- Salary Slip AprilDocument1 pageSalary Slip AprilDaya Shankar100% (2)

- Annex A - Format of Notice of Discrepancy - RMC 102-2020 1Document2 pagesAnnex A - Format of Notice of Discrepancy - RMC 102-2020 1Joanna AbañoPas encore d'évaluation

- PaybilldetailsDocument135 pagesPaybilldetailsSyed Hazrath babaPas encore d'évaluation

- Billing Address: Tax InvoiceDocument1 pageBilling Address: Tax InvoiceGame FreakPas encore d'évaluation

- July 2022 PayslipDocument1 pageJuly 2022 Payslipalumi ghodPas encore d'évaluation

- TDS Final May 24Document1 pageTDS Final May 24Kochu KuchuPas encore d'évaluation

- Solved David Is On The Audit Staff of A National AccountingDocument1 pageSolved David Is On The Audit Staff of A National AccountingAnbu jaromiaPas encore d'évaluation

- Tax Invoice: Name Address State State Code Description AmountDocument1 pageTax Invoice: Name Address State State Code Description AmountvinaygaddamPas encore d'évaluation

- DigestDocument2 pagesDigestAnonymous V0JQmPJcPas encore d'évaluation

- Goods and Service Tax (GST) Presentation: by Kunal Gupta BBA (G) 2 Shift 5 Semester Section BDocument8 pagesGoods and Service Tax (GST) Presentation: by Kunal Gupta BBA (G) 2 Shift 5 Semester Section BAnnu KashyapPas encore d'évaluation

- GST ChallanDocument1 pageGST Challanshaan creationPas encore d'évaluation

- Employment: Complete An Employment' Page For Each Employment or DirectorshipDocument2 pagesEmployment: Complete An Employment' Page For Each Employment or DirectorshipDick WilliamsPas encore d'évaluation

- CIR v. Bank of CommerceDocument6 pagesCIR v. Bank of Commerceamareia yapPas encore d'évaluation

- Fast-Isd 0169007900148617 Fast-Isd 0169007900148617 Fast-Isd 0169007900148617 Fast-Isd 0169007900148617Document1 pageFast-Isd 0169007900148617 Fast-Isd 0169007900148617 Fast-Isd 0169007900148617 Fast-Isd 0169007900148617Tariz ShahidPas encore d'évaluation

- Invoice 9Document1 pageInvoice 9QusaiPas encore d'évaluation

- Annex C RR 11-2018Document1 pageAnnex C RR 11-2018grecelyn bianesPas encore d'évaluation

- US 1040 Main Information Sheet 2021: Email Taxpayer Occupation Spouse Occupation Filing StatusDocument7 pagesUS 1040 Main Information Sheet 2021: Email Taxpayer Occupation Spouse Occupation Filing StatusRaquel Carrero100% (2)