Vous aimerez peut-être aussi

- Accounting Formulas 1 PDFDocument5 pagesAccounting Formulas 1 PDFmianmobeenaslam80% (5)

- Therese Zyra Lipang - Worksheet Activity - 10 Column WsDocument4 pagesTherese Zyra Lipang - Worksheet Activity - 10 Column WsJuvelyn Repaso100% (1)

- Comparative Income Statement, Common Size Statement and Trend AnalysisDocument16 pagesComparative Income Statement, Common Size Statement and Trend Analysisswatitikku69% (26)

- TWO (2) Questions in SECTION B in The Answer Booklet Provided. SECTION A: Answer ALL Questions in This SectionDocument6 pagesTWO (2) Questions in SECTION B in The Answer Booklet Provided. SECTION A: Answer ALL Questions in This SectionRebecca TeoPas encore d'évaluation

- Interpretation of Financial Statements - IntroductionDocument19 pagesInterpretation of Financial Statements - Introductionsazid9Pas encore d'évaluation

- Financial Statements Analysis - An IntroductionDocument19 pagesFinancial Statements Analysis - An Introductionbiniam meazanehPas encore d'évaluation

- FS AnalysisDocument22 pagesFS AnalysissheetaljerryPas encore d'évaluation

- A Study On Fiancial Statement and Analysis at BMTC BangaloreDocument28 pagesA Study On Fiancial Statement and Analysis at BMTC BangaloreSanjay Sanju0% (1)

- Historical Background of Finance:-: DefinitionsDocument28 pagesHistorical Background of Finance:-: DefinitionsApoorva A NPas encore d'évaluation

- Fin Statement AnalysisDocument26 pagesFin Statement AnalysisBhagaban DasPas encore d'évaluation

- BHARATH R Final Report 15-11-18Document63 pagesBHARATH R Final Report 15-11-18aurorashiva1Pas encore d'évaluation

- A Study On Financial Performance For Axis BankDocument20 pagesA Study On Financial Performance For Axis BankJayaprabhu PrabhuPas encore d'évaluation

- Leac204 PDFDocument22 pagesLeac204 PDFIsIs DronePas encore d'évaluation

- 169 Analysis of Financial StatementsDocument29 pages169 Analysis of Financial StatementsPathan KausarPas encore d'évaluation

- Module 2Document45 pagesModule 2Lucksnie LovePas encore d'évaluation

- Chapter 2 (New)Document31 pagesChapter 2 (New)Safuan JaafarPas encore d'évaluation

- Executive SummaryDocument34 pagesExecutive SummaryRachit KharePas encore d'évaluation

- Analysis of Financial StatementsDocument37 pagesAnalysis of Financial StatementsApollo Institute of Hospital Administration100% (5)

- CH - 4 Analysis of Financial StatementsDocument22 pagesCH - 4 Analysis of Financial StatementsKetan RavalPas encore d'évaluation

- 4.1 Meaning of Analysis of Financial Statements L ODocument23 pages4.1 Meaning of Analysis of Financial Statements L OmaxPas encore d'évaluation

- BHARATH SfinalDocument66 pagesBHARATH Sfinalaurorashiva1Pas encore d'évaluation

- "Financial Statment Analysis": Dessrtion Report OnDocument51 pages"Financial Statment Analysis": Dessrtion Report Onpunny27100% (1)

- Class-12 CH-1& 2 Notes-1Document9 pagesClass-12 CH-1& 2 Notes-1uphighdownhardshowtimePas encore d'évaluation

- Aom AssignmentDocument7 pagesAom AssignmentAkanksha PalPas encore d'évaluation

- Analysis of Financial StatementDocument28 pagesAnalysis of Financial Statementbijay bhandariPas encore d'évaluation

- Module 3 Analysis and Interpretation of Financial StatementsDocument23 pagesModule 3 Analysis and Interpretation of Financial StatementsRonald Torres100% (1)

- Financial Analysis of InfosysDocument51 pagesFinancial Analysis of InfosysRahul RajuPas encore d'évaluation

- 1.1 Introduction To Financial StatementsDocument21 pages1.1 Introduction To Financial StatementsPRIYAM XEROXPas encore d'évaluation

- Vijaya Bank Project 007Document60 pagesVijaya Bank Project 007singrahul52Pas encore d'évaluation

- Pre Test: Biliran Province State UniversityDocument6 pagesPre Test: Biliran Province State Universitymichi100% (1)

- Lecture-1&2 - Introduction of Financial Statement AnalysisDocument23 pagesLecture-1&2 - Introduction of Financial Statement AnalysisPrabjot SinghPas encore d'évaluation

- Accounts Part-II 4 PDFDocument26 pagesAccounts Part-II 4 PDFjibin samuelPas encore d'évaluation

- Chapter 1Document7 pagesChapter 1Resueno, Ma. ShainaPas encore d'évaluation

- Financial Statement AnalysisDocument7 pagesFinancial Statement AnalysisResueno, Ma. ShainaPas encore d'évaluation

- 5th Sem Last LongDocument2 pages5th Sem Last Longmdanss1244Pas encore d'évaluation

- Mahindra and MahindraDocument60 pagesMahindra and MahindraAparna TumbarePas encore d'évaluation

- ProjectDocument45 pagesProjectRamakrishna UtukuruPas encore d'évaluation

- Financial Statement AnalysisDocument110 pagesFinancial Statement AnalysisvidhyabalajiPas encore d'évaluation

- Financial Statement AnalysisDocument87 pagesFinancial Statement AnalysisShreyaSinglaPas encore d'évaluation

- Financial Analysis ProjectDocument60 pagesFinancial Analysis ProjectSree GaneshPas encore d'évaluation

- Confidential NotesDocument35 pagesConfidential Noteskamaljit kaushikPas encore d'évaluation

- Financial Statement Analysis of OSCBDocument55 pagesFinancial Statement Analysis of OSCBSunil ShekharPas encore d'évaluation

- Docdownloader Com Comparative Income Statementcommon Size Statement and Trend AnalysisDocument14 pagesDocdownloader Com Comparative Income Statementcommon Size Statement and Trend AnalysisSushant ChoudharyPas encore d'évaluation

- Leac 205Document47 pagesLeac 205Harish Singh NegiPas encore d'évaluation

- CMA (Unit 3)Document16 pagesCMA (Unit 3)Ramakrishna RoshanPas encore d'évaluation

- A Study On Financial PerformanceDocument73 pagesA Study On Financial PerformanceDr Linda Mary Simon100% (2)

- Analysis of Financial StatementDocument51 pagesAnalysis of Financial StatementSumit Rp100% (4)

- Financial: StatementDocument31 pagesFinancial: StatementGrace Joy100% (1)

- Final AccountsDocument91 pagesFinal AccountsKartikey swami0% (1)

- Financial AnalysisDocument7 pagesFinancial AnalysisVishal PatilPas encore d'évaluation

- Ratio AnalysisDocument38 pagesRatio AnalysisMoses FernandesPas encore d'évaluation

- Financial Accounting ReportDocument11 pagesFinancial Accounting Reportthu thienPas encore d'évaluation

- FMA (Comperative Statement Analysis As A Managerial Tool)Document13 pagesFMA (Comperative Statement Analysis As A Managerial Tool)PowerPoint GoPas encore d'évaluation

- 7998 Topper 21 101 504 551 9837 Analysis of Financial Statements Up201904241124 1556085290 1129Document16 pages7998 Topper 21 101 504 551 9837 Analysis of Financial Statements Up201904241124 1556085290 1129Mahmoud ZizoPas encore d'évaluation

- Financial Ratio Interpretation (ITC)Document12 pagesFinancial Ratio Interpretation (ITC)Gorantla SindhujaPas encore d'évaluation

- Finman2 Module 2Document17 pagesFinman2 Module 2Franz Ervy MallariPas encore d'évaluation

- Valuation of Finacial Statment PDFDocument50 pagesValuation of Finacial Statment PDFhindustani888Pas encore d'évaluation

- From Data to Decisions: Harnessing FP&A for Financial Leadership: FP&A Mastery Series, #1D'EverandFrom Data to Decisions: Harnessing FP&A for Financial Leadership: FP&A Mastery Series, #1Pas encore d'évaluation

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"D'Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"Pas encore d'évaluation

- The Balanced Scorecard: Turn your data into a roadmap to successD'EverandThe Balanced Scorecard: Turn your data into a roadmap to successÉvaluation : 3.5 sur 5 étoiles3.5/5 (4)

- 629b9final Placement - Greenlam Industries LTDDocument4 pages629b9final Placement - Greenlam Industries LTDsachin choudharyPas encore d'évaluation

- Syllabus Wealth ManagementDocument4 pagesSyllabus Wealth Managementsachin choudharyPas encore d'évaluation

- Course Title: Marketing Management Course Code: MKTG601 Credit Units: TWODocument4 pagesCourse Title: Marketing Management Course Code: MKTG601 Credit Units: TWOsachin choudharyPas encore d'évaluation

- Memo ClassDocument7 pagesMemo Classsachin choudharyPas encore d'évaluation

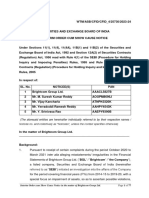

- Notice For StudentsDocument2 pagesNotice For Studentssachin choudharyPas encore d'évaluation

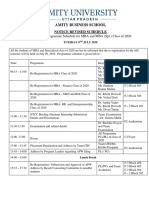

- Amity Business School: Orientation Programme Schedule For MBA and MBA (SPL.) Class of 2020Document2 pagesAmity Business School: Orientation Programme Schedule For MBA and MBA (SPL.) Class of 2020sachin choudharyPas encore d'évaluation

- 41ab8NOTICE FOR STUDENTSDocument1 page41ab8NOTICE FOR STUDENTSsachin choudharyPas encore d'évaluation

- INDIAN CONTRACT ACT CASE STUDIES FOR CA FOUNDATION UPLOADED ON 7th April 2018 636587145256888474 PDFDocument5 pagesINDIAN CONTRACT ACT CASE STUDIES FOR CA FOUNDATION UPLOADED ON 7th April 2018 636587145256888474 PDFsachin choudhary100% (1)

- 065ccrevised Notice - NulearnDocument2 pages065ccrevised Notice - Nulearnsachin choudharyPas encore d'évaluation

- Bfa 80 NoticeDocument1 pageBfa 80 Noticesachin choudharyPas encore d'évaluation

- Brand Factory (Future Group in Retain Co) : Stages in Developing An Incentive SchemeDocument5 pagesBrand Factory (Future Group in Retain Co) : Stages in Developing An Incentive Schemesachin choudharyPas encore d'évaluation

- CHAPTER 17 Borrowing Cost Problem 17-1 To 17-9 CFAS 2020 EditionDocument4 pagesCHAPTER 17 Borrowing Cost Problem 17-1 To 17-9 CFAS 2020 EditionMeljenice Closa PoloniaPas encore d'évaluation

- Forecasting ProblemsDocument3 pagesForecasting ProblemsJimmyChaoPas encore d'évaluation

- Dell's Working Capital SolutionDocument22 pagesDell's Working Capital SolutionShaikh Saifullah KhalidPas encore d'évaluation

- Long Term Construction Quiz PDF FreeDocument4 pagesLong Term Construction Quiz PDF FreeMichael Brian TorresPas encore d'évaluation

- FAR460 - S - June 2018 - StudentsDocument6 pagesFAR460 - S - June 2018 - StudentsRuzaikha razaliPas encore d'évaluation

- Learning Activity 8 BEP Sales With ProfitDocument4 pagesLearning Activity 8 BEP Sales With ProfitEnergy Trading QUEZELCO 1Pas encore d'évaluation

- 2014 IFRS Financial Statements Def CarrefourDocument80 pages2014 IFRS Financial Statements Def CarrefourawangPas encore d'évaluation

- Abc CostingDocument82 pagesAbc Costingradha gregorioPas encore d'évaluation

- CH 14Document16 pagesCH 14جمالعبدالحميدالبرباويPas encore d'évaluation

- Financial Accounting TheoryDocument14 pagesFinancial Accounting TheoryNimalanPas encore d'évaluation

- Ebook Cornerstones of Managerial Accounting Canadian 3Rd Edition Mowen Solutions Manual Full Chapter PDFDocument51 pagesEbook Cornerstones of Managerial Accounting Canadian 3Rd Edition Mowen Solutions Manual Full Chapter PDFxaviaalexandrawp86i100% (12)

- Topic:: Accounts of Holding CompaniesDocument19 pagesTopic:: Accounts of Holding CompaniesCharu LataPas encore d'évaluation

- Basic Cost Management ConceptsDocument33 pagesBasic Cost Management ConceptsMarcela Nichol RaymundoPas encore d'évaluation

- Chapter 5 - Ia3Document3 pagesChapter 5 - Ia3Xynith Nicole RamosPas encore d'évaluation

- Barth, M.E., Landsman, W.R. & Wahlen, J.M. (1995). Fair value accounting: Effects on banks’ earnings volatility, regulatory capital and value of contractual cash flows. Journal of Banking and Finance, 19, 577-605.Document29 pagesBarth, M.E., Landsman, W.R. & Wahlen, J.M. (1995). Fair value accounting: Effects on banks’ earnings volatility, regulatory capital and value of contractual cash flows. Journal of Banking and Finance, 19, 577-605.Marchelyn PongsapanPas encore d'évaluation

- 2018 AFR Local Govt Volume I PDFDocument453 pages2018 AFR Local Govt Volume I PDFRhuejane Gay Maquiling0% (1)

- Jawaban LKS Nasional 2017 PDFDocument13 pagesJawaban LKS Nasional 2017 PDFadebsb100% (2)

- Ch02 Beams12ge SMDocument27 pagesCh02 Beams12ge SMWira Moki100% (3)

- ch14 Kieso IFRS4 PPTDocument75 pagesch14 Kieso IFRS4 PPT1234778Pas encore d'évaluation

- Theory of AccountsDocument4 pagesTheory of AccountsROB101512Pas encore d'évaluation

- Advanced Accounting - Dayag 2015 - Chapter 15 - Multiple Choice Solution (26-28)Document1 pageAdvanced Accounting - Dayag 2015 - Chapter 15 - Multiple Choice Solution (26-28)John Carlos DoringoPas encore d'évaluation

- 8 PDFDocument77 pages8 PDFHemanthThotaPas encore d'évaluation

- Inventories and Biological Assets: Topic List Syllabus ReferenceDocument6 pagesInventories and Biological Assets: Topic List Syllabus ReferenceMaaz QaisraniPas encore d'évaluation

- LECTURE NOTES FOR Revaluation Model PDFDocument10 pagesLECTURE NOTES FOR Revaluation Model PDFFilip SlavchevPas encore d'évaluation

- Advance Accounts Ca Inter by Raj K AgarwalDocument2 pagesAdvance Accounts Ca Inter by Raj K Agarwalashish.jhaa756Pas encore d'évaluation

- Beta Watches Completed The Following Selected Transactions During 2016 andDocument1 pageBeta Watches Completed The Following Selected Transactions During 2016 andhassan taimourPas encore d'évaluation

- Performance Profiles of Major Energy Producers 020605Document110 pagesPerformance Profiles of Major Energy Producers 020605mmvvvPas encore d'évaluation