Vous aimerez peut-être aussi

- Super PaperDocument11 pagesSuper Paperrathish14uPas encore d'évaluation

- Synopsis of ProjectDocument6 pagesSynopsis of Projecthirak_buronPas encore d'évaluation

- Standard Costing and Its Role in Today's Manufacturing EnvironmentDocument10 pagesStandard Costing and Its Role in Today's Manufacturing Environmentsuraj5726100% (2)

- Cost of Poor Quality 1Document7 pagesCost of Poor Quality 1Shavin AvinPas encore d'évaluation

- ABC ArticleDocument7 pagesABC ArticleSamuel Osarose OjomoPas encore d'évaluation

- Cost of Quality As A Driver For Continuous Improvement - Case Study - Company XDocument8 pagesCost of Quality As A Driver For Continuous Improvement - Case Study - Company XAbdur Rahman UsamaPas encore d'évaluation

- An Initiative To Practice Total Quality Management in Aircraft Maintenance SOSSSS PHD OKDocument6 pagesAn Initiative To Practice Total Quality Management in Aircraft Maintenance SOSSSS PHD OKchrysobergiPas encore d'évaluation

- Caso Fase 2 GestionDocument22 pagesCaso Fase 2 Gestionpedluis3Pas encore d'évaluation

- Analysis of Cost Estimating Through Concurrent Engineering Environment Through Life Cycle AnalysisDocument10 pagesAnalysis of Cost Estimating Through Concurrent Engineering Environment Through Life Cycle AnalysisEmdad YusufPas encore d'évaluation

- Ijmet: ©iaemeDocument10 pagesIjmet: ©iaemeIAEME PublicationPas encore d'évaluation

- Capacity Cost Management: MonographDocument10 pagesCapacity Cost Management: Monographsilver_oak123Pas encore d'évaluation

- Quality Costs in A Manufacturing Industry: A Gateway For ImprovementDocument11 pagesQuality Costs in A Manufacturing Industry: A Gateway For ImprovementDih LimaPas encore d'évaluation

- 8 - Lean Production Management Model For SME Waste Reduction in The Processed Food Sector PeruDocument10 pages8 - Lean Production Management Model For SME Waste Reduction in The Processed Food Sector PerualenstercvPas encore d'évaluation

- Managing Cost of Quality Insight Into Industry PracticeDocument9 pagesManaging Cost of Quality Insight Into Industry PracticeJamal IsmailPas encore d'évaluation

- 1991 Quality Costing (Dale, Plunkett) - Páginas-104-125Document22 pages1991 Quality Costing (Dale, Plunkett) - Páginas-104-125Renzo Presbitero AmpueroPas encore d'évaluation

- Cost of Quality, Group-6Document21 pagesCost of Quality, Group-6AarushiPas encore d'évaluation

- International Management JournalsDocument24 pagesInternational Management JournalsYatendra VarmaPas encore d'évaluation

- 7 Usefulness of Traditional and New PerformanceDocument16 pages7 Usefulness of Traditional and New PerformanceChintan JoshiPas encore d'évaluation

- Quality Is The Key1Document12 pagesQuality Is The Key1PappuRamaSubramaniamPas encore d'évaluation

- Lean Maintenance Pfizer Case StudyDocument6 pagesLean Maintenance Pfizer Case StudydenerspPas encore d'évaluation

- Research Papers On TQM ImplementationDocument8 pagesResearch Papers On TQM Implementationsrxzjavkg100% (1)

- Strategic Development in Hospitality: Lesson 1Document26 pagesStrategic Development in Hospitality: Lesson 1Yeunna LaurenPas encore d'évaluation

- 18-Quality Costing An Effecient Measurement For ImprovementDocument8 pages18-Quality Costing An Effecient Measurement For ImprovementIslamSharafPas encore d'évaluation

- Chapter - 2: Quality and Cost: Economic Balance Total CostDocument6 pagesChapter - 2: Quality and Cost: Economic Balance Total Costrajeshsapkota123Pas encore d'évaluation

- Six Sigma in Service OrganisationsDocument18 pagesSix Sigma in Service OrganisationsJosh PintoPas encore d'évaluation

- How to Enhance Productivity Under Cost Control, Quality Control as Well as Time, in a Private or Public OrganizationD'EverandHow to Enhance Productivity Under Cost Control, Quality Control as Well as Time, in a Private or Public OrganizationPas encore d'évaluation

- TQM Chapter 5Document4 pagesTQM Chapter 5Khel PinedaPas encore d'évaluation

- Contemporary Management Philosophies and ToolsDocument11 pagesContemporary Management Philosophies and ToolsYula ParkPas encore d'évaluation

- Accenture Outperforming Competition Execution Excellence SteelDocument16 pagesAccenture Outperforming Competition Execution Excellence Steelmujtabakhan07Pas encore d'évaluation

- Hidden Costs of Quality: Measurement & Analysis: Sailaja A, P C Basak and K G ViswanadhanDocument13 pagesHidden Costs of Quality: Measurement & Analysis: Sailaja A, P C Basak and K G ViswanadhanAmit PaulPas encore d'évaluation

- Cost of Quality 623 1909 1 PBDocument12 pagesCost of Quality 623 1909 1 PBsefriansyah alwi,Pas encore d'évaluation

- 1-Ans. Competitiveness Is at The Core of All Strategies. Even Among Them, Priorities Tend ToDocument5 pages1-Ans. Competitiveness Is at The Core of All Strategies. Even Among Them, Priorities Tend Toajayabhi21Pas encore d'évaluation

- Evaluating Management Practices Through Performance ManagementDocument12 pagesEvaluating Management Practices Through Performance Managementhkhan88Pas encore d'évaluation

- Quality Management in TourismDocument10 pagesQuality Management in TourismJa NicePas encore d'évaluation

- 2016 - CoQ Implementation Methodology-A Case Study in Medium Size MFG Enterprise - PRINTDocument6 pages2016 - CoQ Implementation Methodology-A Case Study in Medium Size MFG Enterprise - PRINTwuri rahardjoPas encore d'évaluation

- Section A P1 Q& ADocument12 pagesSection A P1 Q& AAnisah HabibPas encore d'évaluation

- Poster 2021 MM 33Document4 pagesPoster 2021 MM 33Hassan bhattiPas encore d'évaluation

- Activated 19 Evidence 7 Talking About Logistics, Workshop" Claudia Robayo Gestion Logistica SENA 2020Document11 pagesActivated 19 Evidence 7 Talking About Logistics, Workshop" Claudia Robayo Gestion Logistica SENA 2020claudia gomezPas encore d'évaluation

- Research Article Improving Quality, Productivity, and Cost Aspects of A Sewing Line of Apparel Industry Using TQM ApproachDocument13 pagesResearch Article Improving Quality, Productivity, and Cost Aspects of A Sewing Line of Apparel Industry Using TQM Approachtahmidmuntasir69Pas encore d'évaluation

- Chapter Five Quality Management and Control 5.1. Overview of Total Quality Management and Quality SpecificationDocument7 pagesChapter Five Quality Management and Control 5.1. Overview of Total Quality Management and Quality SpecificationGebrekiros ArayaPas encore d'évaluation

- Application of BPR in HealthcareDocument3 pagesApplication of BPR in Healthcarepeednask75% (4)

- Learning Objectives:: Chapter SixteenDocument4 pagesLearning Objectives:: Chapter Sixteenhardeep bhatiaPas encore d'évaluation

- Mtech Cost Management of Engineering Projects L N Ce r18 0Document118 pagesMtech Cost Management of Engineering Projects L N Ce r18 0Gopikrishnan100% (1)

- Process Flow and Operations Management Within Food-Processing Factories (E-Track)Document6 pagesProcess Flow and Operations Management Within Food-Processing Factories (E-Track)LoganGunasekaranPas encore d'évaluation

- Report Journal ofDocument10 pagesReport Journal ofAmin RamliPas encore d'évaluation

- Rithwik Wip Project 2018Document69 pagesRithwik Wip Project 2018vipinPas encore d'évaluation

- Production Operations Management Muhammad Hammad Alam Bs64 8004 Capacity PlanningDocument2 pagesProduction Operations Management Muhammad Hammad Alam Bs64 8004 Capacity PlanningHammad AlamPas encore d'évaluation

- Basic Concept of TQMDocument33 pagesBasic Concept of TQMFurqan AzizPas encore d'évaluation

- Tqm-Important Tool in Engineering EducationDocument4 pagesTqm-Important Tool in Engineering EducationInternational Journal of Application or Innovation in Engineering & ManagementPas encore d'évaluation

- Quality Systems For Garment ManufactureDocument80 pagesQuality Systems For Garment ManufactureBoroBethaMonePas encore d'évaluation

- Assignment 1 6331Document4 pagesAssignment 1 6331ALIKNFPas encore d'évaluation

- Operations Management Gyan CapsuleDocument6 pagesOperations Management Gyan CapsuleAnandbabu RadhakrishnanPas encore d'évaluation

- Statistical Process Control: An Essential Ingredient For Improving Service and Manufacuring QualityDocument6 pagesStatistical Process Control: An Essential Ingredient For Improving Service and Manufacuring QualityNilakshi RathnayakePas encore d'évaluation

- Hidden Costs of QualityDocument13 pagesHidden Costs of QualityWilliam ScottPas encore d'évaluation

- Total Productive Maintenance For Organisational EffectivenessD'EverandTotal Productive Maintenance For Organisational EffectivenessÉvaluation : 4 sur 5 étoiles4/5 (4)

- Guide for Asset Integrity Managers: A Comprehensive Guide to Strategies, Practices and BenchmarkingD'EverandGuide for Asset Integrity Managers: A Comprehensive Guide to Strategies, Practices and BenchmarkingPas encore d'évaluation

- A Study Of Performance Measurement In The Outsourcing DecisionD'EverandA Study Of Performance Measurement In The Outsourcing DecisionPas encore d'évaluation

- Cost Management: A Case for Business Process Re-engineeringD'EverandCost Management: A Case for Business Process Re-engineeringPas encore d'évaluation

- Workflows: How to Design, Improve and Automate High Performance Processes.D'EverandWorkflows: How to Design, Improve and Automate High Performance Processes.Pas encore d'évaluation

- Supply Chain Performance of Sugar Industry Using Regression AnalysisDocument8 pagesSupply Chain Performance of Sugar Industry Using Regression AnalysisVittal SBPas encore d'évaluation

- Consumer Buying Behaviour in Smartphones Shaikh Farheen: Journal of Management/ShowtocDocument10 pagesConsumer Buying Behaviour in Smartphones Shaikh Farheen: Journal of Management/ShowtocVittal SBPas encore d'évaluation

- Digital Marketing Plan PDFDocument24 pagesDigital Marketing Plan PDFVittal SB100% (2)

- HiDocument7 pagesHiVittal SBPas encore d'évaluation

- Characteristics of The Buying Decision Process For Japanese Products - A European Customer'S Market PerspectiveDocument12 pagesCharacteristics of The Buying Decision Process For Japanese Products - A European Customer'S Market PerspectiveVittal SBPas encore d'évaluation

- 7979 PDFDocument79 pages7979 PDFVittal SBPas encore d'évaluation

- Bibliography Books: (New York: Lexington Books)Document14 pagesBibliography Books: (New York: Lexington Books)Vittal SBPas encore d'évaluation

- An Analytical Study of Consumer Buying Behavior Towards Fashion Apparels in LudhianaDocument13 pagesAn Analytical Study of Consumer Buying Behavior Towards Fashion Apparels in LudhianaVittal SBPas encore d'évaluation

- 11 Chapter 2Document32 pages11 Chapter 2Vittal SBPas encore d'évaluation

- National Conference Papers Published:: TH THDocument2 pagesNational Conference Papers Published:: TH THVittal SBPas encore d'évaluation

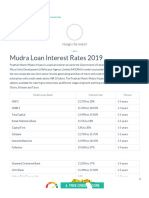

- Mudra Loan Interest Rates in India - 22 May 2019 (Updated)Document10 pagesMudra Loan Interest Rates in India - 22 May 2019 (Updated)Vittal SBPas encore d'évaluation

- A Supply Chain Perspective On Initiatives in The Casting IndustryDocument10 pagesA Supply Chain Perspective On Initiatives in The Casting IndustryVittal SBPas encore d'évaluation

- Customer SatisfactionDocument6 pagesCustomer SatisfactionVittal SBPas encore d'évaluation

- Career Objective: 24-12 A, Shenbaganur, Kodaikanal - 624101. Tamilnadu, INDIA Mobie: +91-9710241182Document7 pagesCareer Objective: 24-12 A, Shenbaganur, Kodaikanal - 624101. Tamilnadu, INDIA Mobie: +91-9710241182Vittal SBPas encore d'évaluation

- Éäã° À Àgà, Sá Àavàæ Àävàäû À Àj ð À Áv C Àåuà Àä Àj Ägàävàû É. ( Àa Ãpàëpàgà À Àävàäû Áapà) Àjãpáë Éã É Àjãpáë ÁapàDocument2 pagesÉäã° À Àgà, Sá Àavàæ Àävàäû À Àj ð À Áv C Àåuà Àä Àj Ägàävàû É. ( Àa Ãpàëpàgà À Àävàäû Áapà) Àjãpáë Éã É Àjãpáë ÁapàVittal SBPas encore d'évaluation

- Casting Blemishes and Supply Chain Relationship in Cast Iron FoundryDocument8 pagesCasting Blemishes and Supply Chain Relationship in Cast Iron FoundryVittal SBPas encore d'évaluation

- Materials ManagementDocument41 pagesMaterials ManagementVaishnavi KrushakthiPas encore d'évaluation

- HR Valuation and AccountingDocument10 pagesHR Valuation and AccountingSanskar YadavPas encore d'évaluation

- Cost Accounting Chapter5 Exercise1 7Document16 pagesCost Accounting Chapter5 Exercise1 7Baby MushroomPas encore d'évaluation

- Financial Aspects of MarketingDocument428 pagesFinancial Aspects of MarketingAnonymous 1NnelvPl100% (2)

- IAS-23 (Borrowing Costs)Document5 pagesIAS-23 (Borrowing Costs)Nazmul HaquePas encore d'évaluation

- Diease LossDocument10 pagesDiease LossGeetha EconomistPas encore d'évaluation

- LECT # 3 - Cost Flow & COGSDocument35 pagesLECT # 3 - Cost Flow & COGSmuhammad.16483.acPas encore d'évaluation

- Cost Solution (Sir Jawad)Document11 pagesCost Solution (Sir Jawad)Tooba MaqboolPas encore d'évaluation

- Quiz 3Document2 pagesQuiz 3shi shiiisshhPas encore d'évaluation

- Managerial Accounting Tools For Business Decision Making 7th Edition Weygandt Solutions ManualDocument42 pagesManagerial Accounting Tools For Business Decision Making 7th Edition Weygandt Solutions Manualvictorialuyen8ggqg100% (25)

- Some Basic Theory For Cost AccountingDocument16 pagesSome Basic Theory For Cost AccountingNaeem KhanPas encore d'évaluation

- Chapter 7 Equipment Sizing and CostingDocument56 pagesChapter 7 Equipment Sizing and CostingDhayalan RamachandranPas encore d'évaluation

- Cost Acctg 1617 2ndsem CE AKDocument10 pagesCost Acctg 1617 2ndsem CE AKanon_684731700% (1)

- Excel Template Inventory ControlDocument27 pagesExcel Template Inventory ControlMC Mejia100% (1)

- 3.5 Inventory Management: Meaning and Nature of InventoryDocument9 pages3.5 Inventory Management: Meaning and Nature of Inventorymantina123Pas encore d'évaluation

- Test Bank For Cost Management A Strategic Emphasis 7th EditionDocument38 pagesTest Bank For Cost Management A Strategic Emphasis 7th EditionSamuelMcclurectgji100% (11)

- Accounting Concepts & ConventionsDocument2 pagesAccounting Concepts & ConventionsDaNeShPas encore d'évaluation

- Study ProbesDocument48 pagesStudy ProbesRose VeePas encore d'évaluation

- Weighted-Average Unit Cost of Completed Leather Belts: $6.10 Total Cost of October 31 Work in Process: $4,700Document1 pageWeighted-Average Unit Cost of Completed Leather Belts: $6.10 Total Cost of October 31 Work in Process: $4,700KamruzzamanPas encore d'évaluation

- HW2 Worksheet Ch09-2Document6 pagesHW2 Worksheet Ch09-2cyc135790cycPas encore d'évaluation

- Management Advisory Services Cpa ReviewDocument30 pagesManagement Advisory Services Cpa ReviewRyan PedroPas encore d'évaluation

- Session 7 & Ic - PGDM 2021 - 23Document28 pagesSession 7 & Ic - PGDM 2021 - 23Krishnapriya NairPas encore d'évaluation

- Fundamentals of Variance Analysis: True / False QuestionsDocument297 pagesFundamentals of Variance Analysis: True / False QuestionsBruce SolanoPas encore d'évaluation

- Cost Accounting: The Institute of Chartered Accountants of PakistanDocument4 pagesCost Accounting: The Institute of Chartered Accountants of PakistanShehrozSTPas encore d'évaluation

- Main Features of Projects, Project Resource Statements and Financial StatementsDocument18 pagesMain Features of Projects, Project Resource Statements and Financial StatementsAsma ZeeshanPas encore d'évaluation

- Manufacturing Financial CostingDocument15 pagesManufacturing Financial CostingJoeFSabaterPas encore d'évaluation

- Paper - 3: Cost and Management Accounting: © The Institute of Chartered Accountants of IndiaDocument24 pagesPaper - 3: Cost and Management Accounting: © The Institute of Chartered Accountants of IndiaUdaykiran BheemaganiPas encore d'évaluation

- Week 8 Quiz SolutionsDocument10 pagesWeek 8 Quiz SolutionsMehwish Pervaiz100% (2)

- PROCESSDocument16 pagesPROCESSAsmita RangariPas encore d'évaluation

- Business Studies Formula Sheet - AS PDFDocument4 pagesBusiness Studies Formula Sheet - AS PDFAdnan Haider NoorPas encore d'évaluation