Vous aimerez peut-être aussi

- Running Head: A Financial Forecast For New World Chemicals IncDocument9 pagesRunning Head: A Financial Forecast For New World Chemicals IncTimPas encore d'évaluation

- Chap 009Document51 pagesChap 009kmillatPas encore d'évaluation

- World Bank - ADB-MOF Report On Philippines PEPFMRDocument224 pagesWorld Bank - ADB-MOF Report On Philippines PEPFMRProfessor Tarun DasPas encore d'évaluation

- Certificate of Employers ' Liability Insurance (A)Document1 pageCertificate of Employers ' Liability Insurance (A)Vincent JohnPas encore d'évaluation

- Chapter 6 - Dynamics of Financial Crises in Advanced EconomiesDocument60 pagesChapter 6 - Dynamics of Financial Crises in Advanced EconomiesJane KotaishPas encore d'évaluation

- Emerging Challenges in Financial Regulation in Context of Financial CrisisDocument23 pagesEmerging Challenges in Financial Regulation in Context of Financial Crisisaks_9886378Pas encore d'évaluation

- Financial Crises ReportDocument14 pagesFinancial Crises ReportClaire VillaceranPas encore d'évaluation

- Financial Crisis, Causes and ReformsDocument18 pagesFinancial Crisis, Causes and ReformsMohammed JavedPas encore d'évaluation

- Financial Crisis, Causes and ReformsDocument17 pagesFinancial Crisis, Causes and Reformsasd_123qwePas encore d'évaluation

- 1.1 What Is Subprime Crisis ?: "SUB PIME CRISIS" This Word Look Small But Not Only The US But The WholeDocument50 pages1.1 What Is Subprime Crisis ?: "SUB PIME CRISIS" This Word Look Small But Not Only The US But The WholeSafiek MeeranPas encore d'évaluation

- FI - M Lecture 7-Why Do Financial Crises Occur - PartialDocument37 pagesFI - M Lecture 7-Why Do Financial Crises Occur - PartialMoazzam ShahPas encore d'évaluation

- 02 Chapter 9 Financial Crises and The Subprime MeltdownDocument29 pages02 Chapter 9 Financial Crises and The Subprime MeltdownDarmawansyahPas encore d'évaluation

- Global Financial CrisesDocument11 pagesGlobal Financial CrisesokashaPas encore d'évaluation

- Financial Crisis PPT FMS 1Document48 pagesFinancial Crisis PPT FMS 1Manoj K Singh100% (1)

- Causes and Effects of The Sub Prime Mortgage CrisisDocument5 pagesCauses and Effects of The Sub Prime Mortgage CrisisRayan RehmanPas encore d'évaluation

- Financial Crisis PPT FMS 1Document48 pagesFinancial Crisis PPT FMS 1Vikas JaiswalPas encore d'évaluation

- 29 - Mishkin - Is Monetary Policy EffectiveDocument18 pages29 - Mishkin - Is Monetary Policy EffectiveAlex PopaPas encore d'évaluation

- A Study On Economic CrisisDocument12 pagesA Study On Economic CrisisShelby ShajahanPas encore d'évaluation

- Global CrisisDocument21 pagesGlobal Crisishema sri mediPas encore d'évaluation

- Financial Crisis in 2007-2008 & It's Impact in BangladeshDocument34 pagesFinancial Crisis in 2007-2008 & It's Impact in Bangladeshjahid.coolPas encore d'évaluation

- Financial Crisis and Its RemediesDocument4 pagesFinancial Crisis and Its RemediesremivictorinPas encore d'évaluation

- Current Issues in Financial MarketsDocument5 pagesCurrent Issues in Financial Marketsreb_nicolePas encore d'évaluation

- Criza Economica Si Financiara in RomaniaDocument5 pagesCriza Economica Si Financiara in RomaniaDana NiculescuPas encore d'évaluation

- 6 - Trần Thị Thu Trang - E4Document17 pages6 - Trần Thị Thu Trang - E4Trang TrầnPas encore d'évaluation

- Apuntes Chapter 7Document6 pagesApuntes Chapter 7Jaime Ruiz-SalinasPas encore d'évaluation

- RGE Monitor Vitoria SaddiDocument27 pagesRGE Monitor Vitoria SaddisagarmaniarPas encore d'évaluation

- Financial Crisis: (Type The Company Name)Document5 pagesFinancial Crisis: (Type The Company Name)Rahul KrishnaPas encore d'évaluation

- Group Assignment ZCMC6142 - CrisisDocument9 pagesGroup Assignment ZCMC6142 - CrisisKok Wai YapPas encore d'évaluation

- Global Financial Crisis (Edited)Document7 pagesGlobal Financial Crisis (Edited)AngelicaP.Ordonia100% (1)

- Financial Markets Final SubmissionDocument10 pagesFinancial Markets Final Submissionabhishek kumarPas encore d'évaluation

- Financial MarketDocument10 pagesFinancial MarketwildahPas encore d'évaluation

- Content: The Economics of Money, Banking, and Financial MarketsDocument14 pagesContent: The Economics of Money, Banking, and Financial MarketsDung ThùyPas encore d'évaluation

- Study of Financial CrisisDocument71 pagesStudy of Financial CrisisAmar Rajput100% (1)

- The Global Financial Crisis::Created byDocument22 pagesThe Global Financial Crisis::Created byĒsrar BalócPas encore d'évaluation

- Economic Recession PresentationDocument16 pagesEconomic Recession Presentationira_mishra_30% (1)

- Financial Crisis of 2007-2010 in US: Evolution of Economic SystemsDocument24 pagesFinancial Crisis of 2007-2010 in US: Evolution of Economic Systemsanca_giorgiana01Pas encore d'évaluation

- Impact of Global Financial Crisis (2007-2008) : ON The Indian EconomyDocument48 pagesImpact of Global Financial Crisis (2007-2008) : ON The Indian EconomyDiksha PrajapatiPas encore d'évaluation

- Topic: The 2008 Recession, Bailout and ConclusionDocument9 pagesTopic: The 2008 Recession, Bailout and ConclusionmeritaaaaPas encore d'évaluation

- AssignmentDocument7 pagesAssignmentTabish KhanPas encore d'évaluation

- Global Financial Crisis During 2008-2010Document12 pagesGlobal Financial Crisis During 2008-2010Mega Pop LockerPas encore d'évaluation

- Great DepressionDocument25 pagesGreat DepressionSmita SinghPas encore d'évaluation

- The Global Financial Crisis 2007-2009Document6 pagesThe Global Financial Crisis 2007-2009Jacques OwokelPas encore d'évaluation

- Financial Crisis ReportDocument8 pagesFinancial Crisis ReportImran CheemaPas encore d'évaluation

- Financial Crisis Money and Banking AssignmentDocument8 pagesFinancial Crisis Money and Banking Assignmentjaguark2210Pas encore d'évaluation

- MONEY AND BANKING (School Work)Document9 pagesMONEY AND BANKING (School Work)Lan Mr-aPas encore d'évaluation

- EconomicDocument5 pagesEconomicVaibhav MishraPas encore d'évaluation

- Financial CrisisDocument5 pagesFinancial CrisisUstaad GPas encore d'évaluation

- Subprime Crisis and Its Impact On The Indian Economy: Macroeconomic EnvironmentDocument24 pagesSubprime Crisis and Its Impact On The Indian Economy: Macroeconomic EnvironmentSadasivuni007Pas encore d'évaluation

- Crisis of CreditDocument4 pagesCrisis of CreditRaven PicorroPas encore d'évaluation

- Application of Agency Theory in Financial CrisesDocument6 pagesApplication of Agency Theory in Financial CrisesHassaan QaziPas encore d'évaluation

- Economic Recession in India: A Net Based Commentary: What The Issue Is All About?Document9 pagesEconomic Recession in India: A Net Based Commentary: What The Issue Is All About?Anshu ManzPas encore d'évaluation

- Group-07 - Sec A PDFDocument22 pagesGroup-07 - Sec A PDFSadasivuni007Pas encore d'évaluation

- Course File 3 Major AssessmentDocument6 pagesCourse File 3 Major AssessmentErnie AbePas encore d'évaluation

- Financial Crisis and Its Effect On BanksDocument5 pagesFinancial Crisis and Its Effect On BanksTejo SajjaPas encore d'évaluation

- The Financial Crisis and Its Impact To The US Economy-FinalVDocument19 pagesThe Financial Crisis and Its Impact To The US Economy-FinalVGlenn MöllerPas encore d'évaluation

- Reinventing Banking: Capitalizing On CrisisDocument28 pagesReinventing Banking: Capitalizing On Crisisworrl samPas encore d'évaluation

- Group Assignment M3 Q1-3Document6 pagesGroup Assignment M3 Q1-3Muhammad Salman ShahPas encore d'évaluation

- Apuntes Chapter 6Document5 pagesApuntes Chapter 6Jaime Ruiz-SalinasPas encore d'évaluation

- Economics AssignmentDocument14 pagesEconomics AssignmentSamvid ShettyPas encore d'évaluation

- Crisis Management in Global BusinessDocument9 pagesCrisis Management in Global BusinessTaneesha RathiPas encore d'évaluation

- The Stability of Financial SystemDocument25 pagesThe Stability of Financial SystemNiraj ShresthaPas encore d'évaluation

- Economics of Business and Finance: Financial CrisesDocument60 pagesEconomics of Business and Finance: Financial CrisesCh MoonPas encore d'évaluation

- Financial Crises in Advanced EconomiesDocument29 pagesFinancial Crises in Advanced EconomiesZeeruanPas encore d'évaluation

- Big5personalitymodel 160530163824Document25 pagesBig5personalitymodel 16053016382406162kPas encore d'évaluation

- Relevant Costing or Incremental AnalysisDocument48 pagesRelevant Costing or Incremental Analysis06162kPas encore d'évaluation

- Present Value of 1 Tabl1Document4 pagesPresent Value of 1 Tabl106162kPas encore d'évaluation

- The Foreign Exchange Market: Manalaysay, Rochelle S. Gatmaitan, Lorraine Aimer Mariano, Patrick Ortega, Jan Rei NielDocument9 pagesThe Foreign Exchange Market: Manalaysay, Rochelle S. Gatmaitan, Lorraine Aimer Mariano, Patrick Ortega, Jan Rei Niel06162kPas encore d'évaluation

- Cash FlowDocument5 pagesCash FlowgarhgelhPas encore d'évaluation

- Business Expenses PDFDocument53 pagesBusiness Expenses PDFSniPas encore d'évaluation

- FMA - Tutorial 8 - Capital BudgetingDocument4 pagesFMA - Tutorial 8 - Capital BudgetingPhuong VuongPas encore d'évaluation

- A Note On Tax ResearchDocument4 pagesA Note On Tax ResearchLeonel FerreiraPas encore d'évaluation

- Professional Money LaunderingDocument53 pagesProfessional Money LaunderingMR. KPas encore d'évaluation

- 1.omc JR - Assistance PDFDocument384 pages1.omc JR - Assistance PDFNaresh Kumar BeheraPas encore d'évaluation

- Partnership FormationDocument5 pagesPartnership FormationAra AlcantaraPas encore d'évaluation

- What Is Insolvency and Bankruptcy CodeDocument9 pagesWhat Is Insolvency and Bankruptcy CodeJosef AnthonyPas encore d'évaluation

- Lecture 11 - Getting Funding of FinancingDocument18 pagesLecture 11 - Getting Funding of FinancingMaryam AslamPas encore d'évaluation

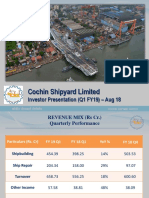

- CSL Investor Presentation Aug 18Document21 pagesCSL Investor Presentation Aug 18gopalptkssPas encore d'évaluation

- IAPMDocument1 pageIAPMSAI SHRIYA NYASAVAJHULAPas encore d'évaluation

- Shivam Popat CBMR SAPM RetailDocument4 pagesShivam Popat CBMR SAPM Retailshivampopat7658Pas encore d'évaluation

- OpportunitiesSWOT ANALYSISDocument6 pagesOpportunitiesSWOT ANALYSISTuico Panlilio Wilbert ImbePas encore d'évaluation

- Sources of FinanceDocument10 pagesSources of FinanceOmer UddinPas encore d'évaluation

- Period End ClosingDocument4 pagesPeriod End ClosingJose Luis Becerril BurgosPas encore d'évaluation

- Afar - MQB Fifth Year Mock Quiz Bee #1 - AFAR: Easy - Question #1 Good Luck!Document7 pagesAfar - MQB Fifth Year Mock Quiz Bee #1 - AFAR: Easy - Question #1 Good Luck!RonPas encore d'évaluation

- Comparative Performance Study of Conventional and Islamic Banking in EgyptDocument14 pagesComparative Performance Study of Conventional and Islamic Banking in EgyptSayed Sharif HashimiPas encore d'évaluation

- 0452 s17 Ms 23Document12 pages0452 s17 Ms 23Vyakt MehtaPas encore d'évaluation

- Solución de Problemas Planteados PresupuestosDocument13 pagesSolución de Problemas Planteados PresupuestosAndre AliagaPas encore d'évaluation

- Valuation of BondsDocument7 pagesValuation of BondsHannah Louise Gutang PortilloPas encore d'évaluation

- Fintech - Did Someone Cancel The Revolution?Document16 pagesFintech - Did Someone Cancel The Revolution?Dominic PaolinoPas encore d'évaluation

- Corporate Strategy A Lecture 1Document64 pagesCorporate Strategy A Lecture 1Falak ShaikhaniPas encore d'évaluation

- How To Pass The 2017 FRM ExamDocument10 pagesHow To Pass The 2017 FRM ExamkrishnPas encore d'évaluation

- IFT Assignment 1 (Akhilesh Jajee)Document3 pagesIFT Assignment 1 (Akhilesh Jajee)anushaPas encore d'évaluation

- An Overview of Basel III: An Evolving Framework For BanksDocument17 pagesAn Overview of Basel III: An Evolving Framework For BanksNikunj NagarPas encore d'évaluation

- 12 - Duty To Account For Secret Profits - JuliaDocument6 pages12 - Duty To Account For Secret Profits - JuliaJulia IliagouevaPas encore d'évaluation