Vous aimerez peut-être aussi

- Case Music MartDocument23 pagesCase Music MartDarwin Dionisio Clemente75% (4)

- Problem 2-2: J.L. Gregory CompanyDocument5 pagesProblem 2-2: J.L. Gregory CompanyKAPIL MBA 2021-23 (Delhi)Pas encore d'évaluation

- Balance Sheet and Transactions Analysis for Charles CompanyDocument14 pagesBalance Sheet and Transactions Analysis for Charles CompanyArunesh SN100% (1)

- Case Study15Document6 pagesCase Study15Arpita SahuPas encore d'évaluation

- Case 2-2 Music Mart Balance Sheet 1 OctDocument5 pagesCase 2-2 Music Mart Balance Sheet 1 OctAnubhav Jha100% (3)

- Ribbons an’ Bows case analysisDocument4 pagesRibbons an’ Bows case analysisShivam Kanojia100% (2)

- Q3 Navin PackagingDocument3 pagesQ3 Navin PackagingRishabh ChawlaPas encore d'évaluation

- Dispensers of CaliforniaDocument4 pagesDispensers of CaliforniaShweta GautamPas encore d'évaluation

- Maynard Company Balance Sheets"TITLE "TITLE Maynard Company June Income StatementDocument2 pagesMaynard Company Balance Sheets"TITLE "TITLE Maynard Company June Income Statementriya lakhotiaPas encore d'évaluation

- Maynard CompanyDocument5 pagesMaynard CompanyNikitha Andrea SaldanhaPas encore d'évaluation

- Assumptions - : Cash Flow From Operations $ 0Document4 pagesAssumptions - : Cash Flow From Operations $ 0Krish HegdePas encore d'évaluation

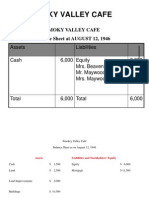

- Smokey Valley Cafe Balance Sheets 1946Document3 pagesSmokey Valley Cafe Balance Sheets 1946mohit_namanPas encore d'évaluation

- Ram Traders - NidhiDocument5 pagesRam Traders - NidhinidhidPas encore d'évaluation

- Problems On Profitable Product MixDocument9 pagesProblems On Profitable Product MixUdita DasPas encore d'évaluation

- WCM QuestionsDocument5 pagesWCM QuestionsBhavin BaxiPas encore d'évaluation

- AHM13e - Chapter - 06 Solution To Problems and Key To CasesDocument26 pagesAHM13e - Chapter - 06 Solution To Problems and Key To CasesGaurav ManiyarPas encore d'évaluation

- Chapter 6 Cost of Sales and Inventories GuideDocument62 pagesChapter 6 Cost of Sales and Inventories GuideRosedel Rosas100% (2)

- Maynard Company (A & B)Document9 pagesMaynard Company (A & B)akashnathgarg0% (1)

- Chapter 7Document19 pagesChapter 7Arun Kumar SatapathyPas encore d'évaluation

- Lone Pine Cafe Balance Sheets Case StudyDocument13 pagesLone Pine Cafe Balance Sheets Case StudyCynthia Anggi Maulina100% (1)

- Mansa Building Case Study AnalysisDocument14 pagesMansa Building Case Study AnalysisRikki DasPas encore d'évaluation

- Modern Pharma SolnDocument3 pagesModern Pharma SolnSakshiPas encore d'évaluation

- Campus PizzeriaDocument12 pagesCampus PizzeriaSHIVAM SRIVASTAVAPas encore d'évaluation

- Stock Valuation Problems SolvedDocument6 pagesStock Valuation Problems SolvedShubham Aggarwal100% (1)

- Industrial Relations at Asian Paints - ePGPX03 - Group - 9Document13 pagesIndustrial Relations at Asian Paints - ePGPX03 - Group - 9manik singh0% (2)

- Spencer Tire PurchaseDocument28 pagesSpencer Tire PurchaseJitendra Choudhary0% (2)

- Case Analysis American University of Beirut Medical Centre (AUBMC) PACADI FrameworkDocument7 pagesCase Analysis American University of Beirut Medical Centre (AUBMC) PACADI FrameworkAdarsh Nayan100% (1)

- Thumbs-Up Inc.Document4 pagesThumbs-Up Inc.Rakshit Chandra Shekhar JoshiPas encore d'évaluation

- Boardroom GameDocument12 pagesBoardroom GameShivam SomaniPas encore d'évaluation

- Question: Erika and Kitty, Who Are Twins, Just Received $30,000 Each For Their 25th Birthday. They Both Hav..Document4 pagesQuestion: Erika and Kitty, Who Are Twins, Just Received $30,000 Each For Their 25th Birthday. They Both Hav..Malik AsadPas encore d'évaluation

- Problems & Solutions - RNSDocument28 pagesProblems & Solutions - RNSAyushi0% (1)

- Ikea-Case-Analysis 2Document10 pagesIkea-Case-Analysis 2Nicole ClianoPas encore d'évaluation

- Sharma Industries structural dilemma case studyDocument7 pagesSharma Industries structural dilemma case studyRohanPas encore d'évaluation

- Managers We Are Katti With You - PPL - Group-4Document11 pagesManagers We Are Katti With You - PPL - Group-4kjhathiPas encore d'évaluation

- Problem 3-1Document2 pagesProblem 3-1Omar CirunayPas encore d'évaluation

- Hamilton - Case BDocument8 pagesHamilton - Case BJayash KaushalPas encore d'évaluation

- Chemalite Inc Cash Flow AnalysisDocument2 pagesChemalite Inc Cash Flow AnalysisAnuragPas encore d'évaluation

- Lori Crump Accounting Case StudyDocument1 pageLori Crump Accounting Case StudyHarsh Anchalia100% (1)

- Lone Pine Cafe-CaseDocument28 pagesLone Pine Cafe-CaseNadya Rizkita100% (2)

- HDFC Bank SWOT Analysis and Management InsightDocument9 pagesHDFC Bank SWOT Analysis and Management InsightDumb LittyPas encore d'évaluation

- EZ Trailers Production OptimizationDocument3 pagesEZ Trailers Production OptimizationSomething ChicPas encore d'évaluation

- Somany Ceramics Recruitment Case StudyDocument5 pagesSomany Ceramics Recruitment Case StudyTUSAR singhPas encore d'évaluation

- Statement of Profit and Loss, Balance Sheet and Cash Flow Analysis for 1999Document4 pagesStatement of Profit and Loss, Balance Sheet and Cash Flow Analysis for 1999Jayash KaushalPas encore d'évaluation

- Income Statements 2010Document10 pagesIncome Statements 2010Shivam GoelPas encore d'évaluation

- Making A Tough Personnel Decision at Nova Waterfront HotelDocument11 pagesMaking A Tough Personnel Decision at Nova Waterfront HotelSiddharthPas encore d'évaluation

- Manager We Are Katti With YouDocument6 pagesManager We Are Katti With Youmanik singhPas encore d'évaluation

- Clinical Cost Classification and Break-Even AnalysisDocument9 pagesClinical Cost Classification and Break-Even AnalysisKristal Fialho Costa JolyPas encore d'évaluation

- Case Analysis - Nitish@Solutions Unlimited 1Document5 pagesCase Analysis - Nitish@Solutions Unlimited 1Piyush SahaPas encore d'évaluation

- Northboro Machine Tools CorporationDocument9 pagesNorthboro Machine Tools Corporationsheersha kkPas encore d'évaluation

- Case Report - Grenell FarmDocument5 pagesCase Report - Grenell Farmajsibal100% (1)

- Assignment 3 Mismanagement of Fiscal Policy Greece's Achilles' HeelDocument6 pagesAssignment 3 Mismanagement of Fiscal Policy Greece's Achilles' HeelYash Aggarwal100% (1)

- Lewis Corporation case study: Analysis of inventory valuation methodsDocument7 pagesLewis Corporation case study: Analysis of inventory valuation methodsSudeep ShahPas encore d'évaluation

- Forest City Tennis Club General Ledger and Financial StatementsDocument9 pagesForest City Tennis Club General Ledger and Financial StatementsAhmedNiaz100% (1)

- ICICI Bank's Strategy to Capture Untapped Retail MarketDocument13 pagesICICI Bank's Strategy to Capture Untapped Retail MarketSonaldeep100% (1)

- Fra Mid-Term Pgp13Document3 pagesFra Mid-Term Pgp13Gauri AgarwalPas encore d'évaluation

- 704Document3 pages704Bhoomi GhariwalaPas encore d'évaluation

- 704Document5 pages704Bhoomi GhariwalaPas encore d'évaluation

- Accounting Exams - 1Document2 pagesAccounting Exams - 1MachelMDotAlexanderPas encore d'évaluation

- Instructions: 2-36 CHAPTERDocument4 pagesInstructions: 2-36 CHAPTERahmad Fauzani MuslimPas encore d'évaluation

- Group assignment: Financial accountingDocument4 pagesGroup assignment: Financial accountingNguyen HuongPas encore d'évaluation

- 560289Document20 pages560289Stranger SinhaPas encore d'évaluation

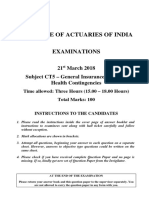

- Actuarial Society of India: ExaminationsDocument5 pagesActuarial Society of India: ExaminationsStranger SinhaPas encore d'évaluation

- Case Method of LearningDocument8 pagesCase Method of LearningStranger SinhaPas encore d'évaluation

- Maynard A SolutionDocument3 pagesMaynard A SolutionStranger SinhaPas encore d'évaluation

- Institute of Actuaries of India: ExaminationsDocument7 pagesInstitute of Actuaries of India: ExaminationsStranger SinhaPas encore d'évaluation

- Current Assets: Asofjunei As of June 30Document3 pagesCurrent Assets: Asofjunei As of June 30Stranger SinhaPas encore d'évaluation

- JPMorgan Chase Organisational Behaviour StrategiesDocument3 pagesJPMorgan Chase Organisational Behaviour StrategiesStranger SinhaPas encore d'évaluation

- Analyzing Business Markets Chapter 7 OutlineDocument21 pagesAnalyzing Business Markets Chapter 7 OutlineStranger SinhaPas encore d'évaluation

- Usin Activity-Based Costing (ABC) To Measure Profitability On A Commercial Loan Portfolio - Mehmet C. KocakulahDocument19 pagesUsin Activity-Based Costing (ABC) To Measure Profitability On A Commercial Loan Portfolio - Mehmet C. KocakulahUmar Farooq Attari100% (2)

- The Investment Function in Banking and Financial-Services ManagementDocument18 pagesThe Investment Function in Banking and Financial-Services ManagementHaris FadžanPas encore d'évaluation

- Product MarketingDocument2 pagesProduct MarketingAmirul AzwanPas encore d'évaluation

- Presentation On Attrition Rate of DeloitteDocument13 pagesPresentation On Attrition Rate of DeloitteRohit GuptaPas encore d'évaluation

- Engagements To Review Financial Statements PSRE 2400Document13 pagesEngagements To Review Financial Statements PSRE 2400ChristineThereseBrazulaPas encore d'évaluation

- Quality Improvement With Statistical Process Control in The Automotive IndustryDocument8 pagesQuality Improvement With Statistical Process Control in The Automotive Industryonii96Pas encore d'évaluation

- Supply Chain-Case Study of DellDocument3 pagesSupply Chain-Case Study of DellSafijo Alphons100% (1)

- Hygienic Chappathi Business Loan ReportDocument13 pagesHygienic Chappathi Business Loan ReportJose PiusPas encore d'évaluation

- Water and Diamond ParadoxDocument19 pagesWater and Diamond ParadoxDevraj100% (1)

- Lecture7 - Equipment and Material HandlingDocument52 pagesLecture7 - Equipment and Material HandlingAkimBiPas encore d'évaluation

- The Cost of Capital, Corporate Finance and The Theory of Investment-Modigliani MillerDocument38 pagesThe Cost of Capital, Corporate Finance and The Theory of Investment-Modigliani MillerArdi GunardiPas encore d'évaluation

- LC Financial Report & Google Drive Link: Aiesec Delhi IitDocument6 pagesLC Financial Report & Google Drive Link: Aiesec Delhi IitCIM_DelhiIITPas encore d'évaluation

- Business PlanDocument31 pagesBusiness PlanBabasab Patil (Karrisatte)100% (1)

- Annual Training Calendar 2011-2012Document10 pagesAnnual Training Calendar 2011-2012krovvidiprasadaraoPas encore d'évaluation

- SAP Project Systems OverviewDocument6 pagesSAP Project Systems OverviewkhanmdPas encore d'évaluation

- E-Challan CCMT ChallanDocument2 pagesE-Challan CCMT ChallanSingh KDPas encore d'évaluation

- Advanced Accounting Part 2 Dayag 2015 Chapter 12Document17 pagesAdvanced Accounting Part 2 Dayag 2015 Chapter 12crispyy turon100% (1)

- Ch. 13 Leverage and Capital Structure AnswersDocument23 pagesCh. 13 Leverage and Capital Structure Answersbetl89% (27)

- E-Business Tax Application SetupDocument25 pagesE-Business Tax Application Setuprasemahe4100% (1)

- Cash Inflow and OutflowDocument6 pagesCash Inflow and OutflowMubeenPas encore d'évaluation

- c19b - Cash Flow To Equity - ModelDocument6 pagesc19b - Cash Flow To Equity - ModelaluiscgPas encore d'évaluation

- AU Small Finance Bank LTD.: General OverviewDocument3 pagesAU Small Finance Bank LTD.: General Overviewdarshan jainPas encore d'évaluation

- Main Theories of FDIDocument22 pagesMain Theories of FDIThu TrangPas encore d'évaluation

- Afghan Rose Project - Some More DetailsDocument4 pagesAfghan Rose Project - Some More DetailsShrinkhala JainPas encore d'évaluation

- Hygeia International: I. Title of The CaseDocument7 pagesHygeia International: I. Title of The CaseDan GabonPas encore d'évaluation

- Term Paper-IMCDocument9 pagesTerm Paper-IMCMazharul Islam AnikPas encore d'évaluation

- BDW94CDocument7 pagesBDW94CWalter FabianPas encore d'évaluation

- Finals Quiz #2 Soce, Soci, Ahfs and Do Multiple Choice: Account Title AmountDocument3 pagesFinals Quiz #2 Soce, Soci, Ahfs and Do Multiple Choice: Account Title AmountNew TonPas encore d'évaluation

- Ravikumar S: Specialties: Pre-Opening, Procurement, Implementing Best Practices, Budgets, CostDocument2 pagesRavikumar S: Specialties: Pre-Opening, Procurement, Implementing Best Practices, Budgets, CostMurthy BanagarPas encore d'évaluation

- Idea Bridge - 100 Success Plan For Crisis Recovery & New CeoDocument6 pagesIdea Bridge - 100 Success Plan For Crisis Recovery & New CeoJairo H Pinzón CastroPas encore d'évaluation