Vous aimerez peut-être aussi

- Business Ethics - CEC 3 - Group 1Document10 pagesBusiness Ethics - CEC 3 - Group 1Avinaba GuhaPas encore d'évaluation

- ZERO TO MASTERY IN CORPORATE GOVERNANCE: Become Zero To Hero In Corporate Governance, This Book Covers A-Z Corporate Governance Concepts, 2022 Latest EditionD'EverandZERO TO MASTERY IN CORPORATE GOVERNANCE: Become Zero To Hero In Corporate Governance, This Book Covers A-Z Corporate Governance Concepts, 2022 Latest EditionPas encore d'évaluation

- CG International PerspectiveDocument6 pagesCG International PerspectiveAayushiPas encore d'évaluation

- Corporate Governance: A practical guide for accountantsD'EverandCorporate Governance: A practical guide for accountantsÉvaluation : 5 sur 5 étoiles5/5 (1)

- Corporate Governance and EthicsDocument6 pagesCorporate Governance and EthicspremcheePas encore d'évaluation

- Corporate Governance - Quantity Versus Quality - Middle Eastern PerspectiveD'EverandCorporate Governance - Quantity Versus Quality - Middle Eastern PerspectivePas encore d'évaluation

- ON Corporate Governance IN India": A On "Oecd RecommendationsDocument25 pagesON Corporate Governance IN India": A On "Oecd RecommendationsUrvesh ParmarPas encore d'évaluation

- Corporate Governance: Ensuring Accountability and TransparencyD'EverandCorporate Governance: Ensuring Accountability and TransparencyPas encore d'évaluation

- Proposed Research Work For Major Research Project On: "A Study On Indian Corporate Governance Practices"Document11 pagesProposed Research Work For Major Research Project On: "A Study On Indian Corporate Governance Practices"Yepuru ChaithanyaPas encore d'évaluation

- Corporate GovernanceDocument100 pagesCorporate GovernanceGerald MagaitaPas encore d'évaluation

- CG and Business EthicsDocument28 pagesCG and Business EthicsabhshekPas encore d'évaluation

- Corporate Governance - Presentation-12Document53 pagesCorporate Governance - Presentation-12Puneet MittalPas encore d'évaluation

- Governance Is That Separate Process or Certain Part of Management or LeadershipDocument4 pagesGovernance Is That Separate Process or Certain Part of Management or Leadershipk gowtham kumarPas encore d'évaluation

- Project 2Document61 pagesProject 2Krishna ThapaPas encore d'évaluation

- Role of Audit in Corporate GovernanceDocument22 pagesRole of Audit in Corporate GovernancelikepopularPas encore d'évaluation

- Emerging Trends in Corporate GovernanceDocument16 pagesEmerging Trends in Corporate GovernanceSaifu KhanPas encore d'évaluation

- Business Ethics and Corporate GovernanceDocument29 pagesBusiness Ethics and Corporate GovernanceNeeraj SharmaPas encore d'évaluation

- (2010 Rev Jan 19 Teehankee) Corporate GovernanceDocument19 pages(2010 Rev Jan 19 Teehankee) Corporate GovernanceRaymond Pacaldo100% (2)

- 25 - Evolution of Corporate Governance in India and AbroadDocument9 pages25 - Evolution of Corporate Governance in India and AbroadArunima SarkarPas encore d'évaluation

- Corporate Governance.....Document10 pagesCorporate Governance.....jyotsana vermaPas encore d'évaluation

- Corporate Governance From A Global Perspective: SSRN Electronic Journal April 2011Document18 pagesCorporate Governance From A Global Perspective: SSRN Electronic Journal April 2011Tehsemut AntPas encore d'évaluation

- GGSR ch3Document29 pagesGGSR ch3Bryan DialingPas encore d'évaluation

- Copy (3) of Copy of Corporate Governance 1Document20 pagesCopy (3) of Copy of Corporate Governance 1bappa85Pas encore d'évaluation

- Becg M 6Document20 pagesBecg M 6CH ANIL VARMAPas encore d'évaluation

- Corporate Governance Practices of Listed Companies in India.Document11 pagesCorporate Governance Practices of Listed Companies in India.Om Pratik MishraPas encore d'évaluation

- Corporate Governance and Leadership:Is There A Nexus?: Nwosu M. Eze, Eze-Nwosu P. ChiamakaDocument8 pagesCorporate Governance and Leadership:Is There A Nexus?: Nwosu M. Eze, Eze-Nwosu P. Chiamakamanishaamba7547Pas encore d'évaluation

- Corporate Governance, AnalysesDocument15 pagesCorporate Governance, AnalysesPavithra GopalakrishnanPas encore d'évaluation

- Total ProjectDocument78 pagesTotal ProjectChandra Sekhar JujjuvarapuPas encore d'évaluation

- Project ReportDocument22 pagesProject ReportDhruvi KothariPas encore d'évaluation

- Corporate Governance - MODULEDocument127 pagesCorporate Governance - MODULEIness KyapwanyamaPas encore d'évaluation

- Introduction: An Overview of Telecommunication CompaniesDocument27 pagesIntroduction: An Overview of Telecommunication CompaniesSri VarshiniPas encore d'évaluation

- Company Secretaryship Training: Submitted By: Rashmi Rekha Bora Registration Number: 120330769/08/2009Document28 pagesCompany Secretaryship Training: Submitted By: Rashmi Rekha Bora Registration Number: 120330769/08/2009RashmiPas encore d'évaluation

- UNIT 4 Part 1Document3 pagesUNIT 4 Part 1Astik TripathiPas encore d'évaluation

- Guideline Corporate GovernanceDocument6 pagesGuideline Corporate GovernanceSukh BrarPas encore d'évaluation

- Corporate Governance ModelsDocument11 pagesCorporate Governance ModelsNajmah Siddiqua NaazPas encore d'évaluation

- Corporate Governance in InsuranceDocument95 pagesCorporate Governance in Insurancemohyeb50% (4)

- Corporate Governance & Insurance Industry.Document42 pagesCorporate Governance & Insurance Industry.Parag MorePas encore d'évaluation

- Corporate GovernanceDocument25 pagesCorporate GovernanceRa VanaPas encore d'évaluation

- Corporate Governanace in MNCsDocument61 pagesCorporate Governanace in MNCsnitin0010Pas encore d'évaluation

- Becg M 6Document20 pagesBecg M 6CH ANIL VARMAPas encore d'évaluation

- Corporate Governance in The 21st CenturyDocument8 pagesCorporate Governance in The 21st CenturymayhemclubPas encore d'évaluation

- Corporate Ethics From Global PerspectiveDocument18 pagesCorporate Ethics From Global PerspectiveDooms 001Pas encore d'évaluation

- Project Report On CGDocument25 pagesProject Report On CGRa VanaPas encore d'évaluation

- Corporate GovernanceDocument19 pagesCorporate GovernanceShubham Dhimaan100% (1)

- CORPORATE GovernanceDocument62 pagesCORPORATE Governanceaurorashiva1Pas encore d'évaluation

- Corporate GovernanceDocument16 pagesCorporate GovernanceAishDPas encore d'évaluation

- The Japanese ModelDocument3 pagesThe Japanese ModelSiva Prasad PasupuletiPas encore d'évaluation

- Corporate Governance (Law 506) Models of Corporate Governance: Japanese Model and German ModelDocument18 pagesCorporate Governance (Law 506) Models of Corporate Governance: Japanese Model and German Modelprabhat chaudharyPas encore d'évaluation

- Challenges and Concerns in The Progressive Regulatory Structure For Corporate Governance in IndiaDocument7 pagesChallenges and Concerns in The Progressive Regulatory Structure For Corporate Governance in IndiaInternational Journal of Innovative Science and Research TechnologyPas encore d'évaluation

- Corporate Governance From A Global PerspectiveDocument18 pagesCorporate Governance From A Global PerspectiveAsham SharmaPas encore d'évaluation

- Corporate GovernanceDocument29 pagesCorporate GovernanceBrandi Pruitt75% (4)

- BJP Becg Mba 4th SemDocument63 pagesBJP Becg Mba 4th Semabhiiktaadas50% (2)

- Corporate Governance MAINDocument25 pagesCorporate Governance MAINprashantgorulePas encore d'évaluation

- Good Governance IcedDocument5 pagesGood Governance IcedKurt CaneroPas encore d'évaluation

- Ch.1 Introduction: Taxmann's Company Law, Kapoor G.K., 20 EdnDocument16 pagesCh.1 Introduction: Taxmann's Company Law, Kapoor G.K., 20 Ednnirshan rajPas encore d'évaluation

- Unit - 3 Auditing and Corporate Governance.Document20 pagesUnit - 3 Auditing and Corporate Governance.laxmisruti123Pas encore d'évaluation

- The OECD Principles of Corporate GovernanceDocument12 pagesThe OECD Principles of Corporate GovernanceAlex Stefan100% (2)

- Corporate GovernanceDocument3 pagesCorporate GovernanceShahidul Hoque FaisalPas encore d'évaluation

- Corporate Governance in IndiaDocument9 pagesCorporate Governance in IndiaRama KrishnanPas encore d'évaluation

- Contractual IndemnitiesDocument481 pagesContractual IndemnitiesUrvashi JaswaniPas encore d'évaluation

- Far Week 6 Investment Properties RevieweesDocument4 pagesFar Week 6 Investment Properties RevieweesAdan NadaPas encore d'évaluation

- Chapter 8Document3 pagesChapter 8kish MishPas encore d'évaluation

- LAW 20013 Law On Obligations and Contracts Midterm ReviewDocument14 pagesLAW 20013 Law On Obligations and Contracts Midterm ReviewNila Francia100% (1)

- Investor Relations Presentation May 2019Document65 pagesInvestor Relations Presentation May 2019Manuel BertlPas encore d'évaluation

- Iip FinalDocument57 pagesIip FinalNagireddy KalluriPas encore d'évaluation

- 18.marginal Absorption NewDocument17 pages18.marginal Absorption NewMuhammad EjazPas encore d'évaluation

- Annexure 19 For Central ExciseDocument5 pagesAnnexure 19 For Central ExciseStephen Hale0% (1)

- Breach of Obligation - Vasquez V Ayala Corporation Case DigestDocument2 pagesBreach of Obligation - Vasquez V Ayala Corporation Case DigestKyra Sy-Santos100% (2)

- Week 12: Chapter 17-Banking and Management of Financial InstitutionsDocument4 pagesWeek 12: Chapter 17-Banking and Management of Financial InstitutionsJay Ann DomePas encore d'évaluation

- How To Get Rich (Without Getting Lucky)Document36 pagesHow To Get Rich (Without Getting Lucky)Maxim Averin100% (3)

- Transfer Pricing: Acc 7 - Management Consultancy Test BankDocument14 pagesTransfer Pricing: Acc 7 - Management Consultancy Test BankHiraya ManawariPas encore d'évaluation

- Proceeding UGEFIC 2021Document552 pagesProceeding UGEFIC 2021Saya100% (1)

- Analysis of Annual Report:: AbstractDocument6 pagesAnalysis of Annual Report:: Abstractapi-301617324Pas encore d'évaluation

- The PPDA Act 2003 (Uganda)Document32 pagesThe PPDA Act 2003 (Uganda)Eric Akena100% (5)

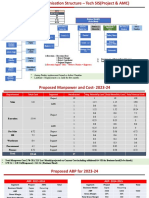

- Proposed Org Chart - Tech SIS.Document5 pagesProposed Org Chart - Tech SIS.Santosh KumarPas encore d'évaluation

- CitiBank ScamsDocument28 pagesCitiBank ScamsAeman WaghooPas encore d'évaluation

- Cost Accounting - Job CostingDocument6 pagesCost Accounting - Job CostingPamela WilliamsPas encore d'évaluation

- Stephen Beach IFRS Lae PDFDocument1 pageStephen Beach IFRS Lae PDFGikamo GasingPas encore d'évaluation

- Part A-GEN: (See Instructions) (See Instructions)Document22 pagesPart A-GEN: (See Instructions) (See Instructions)Syed Faisal AhsanPas encore d'évaluation

- 11 NIQ Soil Testing PatharkandiDocument2 pages11 NIQ Soil Testing Patharkandiexecutive engineer1Pas encore d'évaluation

- December 2012 With WatermarkDocument175 pagesDecember 2012 With WatermarkNageswaran GopuPas encore d'évaluation

- Fundamental RulesDocument41 pagesFundamental RulesSrikanth KovurPas encore d'évaluation

- GWERU RESIDENTS AND RATESPAYERS ASSOCIATION - AmendedDocument16 pagesGWERU RESIDENTS AND RATESPAYERS ASSOCIATION - AmendedClive MakumbePas encore d'évaluation

- Steps To Set Up An Industry in Khed CityDocument2 pagesSteps To Set Up An Industry in Khed CityRush DivPas encore d'évaluation

- BKM CH 06 Answers W CFADocument11 pagesBKM CH 06 Answers W CFAKyThoaiPas encore d'évaluation

- SAP MM Inventory Accounting EntriesDocument17 pagesSAP MM Inventory Accounting EntriesKrishna Akula100% (1)

- BAFS SAMPLE - SMEs Mangement (Partial)Document11 pagesBAFS SAMPLE - SMEs Mangement (Partial)Phoebe WangPas encore d'évaluation

- Apino Jan Dave T. BSA 4-1 QuizDocument14 pagesApino Jan Dave T. BSA 4-1 QuizRosemarie RamosPas encore d'évaluation

- Fania Qinthara Azka - Case Chapter 2Document3 pagesFania Qinthara Azka - Case Chapter 2Fania AzkaPas encore d'évaluation

- Summary: Trading in the Zone: Trading in the Zone: Master the Market with Confidence, Discipline, and a Winning Attitude by Mark Douglas: Key Takeaways, Summary & AnalysisD'EverandSummary: Trading in the Zone: Trading in the Zone: Master the Market with Confidence, Discipline, and a Winning Attitude by Mark Douglas: Key Takeaways, Summary & AnalysisÉvaluation : 5 sur 5 étoiles5/5 (15)

- Summary: The Gap and the Gain: The High Achievers' Guide to Happiness, Confidence, and Success by Dan Sullivan and Dr. Benjamin Hardy: Key Takeaways, Summary & AnalysisD'EverandSummary: The Gap and the Gain: The High Achievers' Guide to Happiness, Confidence, and Success by Dan Sullivan and Dr. Benjamin Hardy: Key Takeaways, Summary & AnalysisÉvaluation : 5 sur 5 étoiles5/5 (4)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)D'EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Évaluation : 4.5 sur 5 étoiles4.5/5 (13)

- The Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeD'EverandThe Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeÉvaluation : 4.5 sur 5 étoiles4.5/5 (90)

- Summary: The Psychology of Money: Timeless Lessons on Wealth, Greed, and Happiness by Morgan Housel: Key Takeaways, Summary & Analysis IncludedD'EverandSummary: The Psychology of Money: Timeless Lessons on Wealth, Greed, and Happiness by Morgan Housel: Key Takeaways, Summary & Analysis IncludedÉvaluation : 5 sur 5 étoiles5/5 (81)

- Broken Money: Why Our Financial System Is Failing Us and How We Can Make It BetterD'EverandBroken Money: Why Our Financial System Is Failing Us and How We Can Make It BetterÉvaluation : 5 sur 5 étoiles5/5 (3)

- Financial Intelligence: How to To Be Smart with Your Money and Your LifeD'EverandFinancial Intelligence: How to To Be Smart with Your Money and Your LifeÉvaluation : 4.5 sur 5 étoiles4.5/5 (540)

- Summary of 10x Is Easier than 2x: How World-Class Entrepreneurs Achieve More by Doing Less by Dan Sullivan & Dr. Benjamin Hardy: Key Takeaways, Summary & AnalysisD'EverandSummary of 10x Is Easier than 2x: How World-Class Entrepreneurs Achieve More by Doing Less by Dan Sullivan & Dr. Benjamin Hardy: Key Takeaways, Summary & AnalysisÉvaluation : 4.5 sur 5 étoiles4.5/5 (24)

- The Millionaire Fastlane: Crack the Code to Wealth and Live Rich for a LifetimeD'EverandThe Millionaire Fastlane: Crack the Code to Wealth and Live Rich for a LifetimeÉvaluation : 4.5 sur 5 étoiles4.5/5 (2)

- Quotex Success Blueprint: The Ultimate Guide to Forex and QuotexD'EverandQuotex Success Blueprint: The Ultimate Guide to Forex and QuotexPas encore d'évaluation

- Rich Bitch: A Simple 12-Step Plan for Getting Your Financial Life Together . . . FinallyD'EverandRich Bitch: A Simple 12-Step Plan for Getting Your Financial Life Together . . . FinallyÉvaluation : 4 sur 5 étoiles4/5 (8)

- Rich Dad Poor Dad: What the Rich Teach Their Kids About Money That the Poor and Middle Class Do NotD'EverandRich Dad Poor Dad: What the Rich Teach Their Kids About Money That the Poor and Middle Class Do NotPas encore d'évaluation

- Bitter Brew: The Rise and Fall of Anheuser-Busch and America's Kings of BeerD'EverandBitter Brew: The Rise and Fall of Anheuser-Busch and America's Kings of BeerÉvaluation : 4 sur 5 étoiles4/5 (52)

- Sleep And Grow Rich: Guided Sleep Meditation with Affirmations For Wealth & AbundanceD'EverandSleep And Grow Rich: Guided Sleep Meditation with Affirmations For Wealth & AbundanceÉvaluation : 4.5 sur 5 étoiles4.5/5 (105)

- A Happy Pocket Full of Money: Your Quantum Leap Into The Understanding, Having And Enjoying Of Immense Abundance And HappinessD'EverandA Happy Pocket Full of Money: Your Quantum Leap Into The Understanding, Having And Enjoying Of Immense Abundance And HappinessÉvaluation : 5 sur 5 étoiles5/5 (159)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindD'EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindÉvaluation : 5 sur 5 étoiles5/5 (231)

- Fluke: Chance, Chaos, and Why Everything We Do MattersD'EverandFluke: Chance, Chaos, and Why Everything We Do MattersÉvaluation : 4.5 sur 5 étoiles4.5/5 (20)

- Baby Steps Millionaires: How Ordinary People Built Extraordinary Wealth--and How You Can TooD'EverandBaby Steps Millionaires: How Ordinary People Built Extraordinary Wealth--and How You Can TooÉvaluation : 5 sur 5 étoiles5/5 (324)

- Meet the Frugalwoods: Achieving Financial Independence Through Simple LivingD'EverandMeet the Frugalwoods: Achieving Financial Independence Through Simple LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (67)

- Unshakeable: Your Financial Freedom PlaybookD'EverandUnshakeable: Your Financial Freedom PlaybookÉvaluation : 4.5 sur 5 étoiles4.5/5 (618)

- The Holy Grail of Investing: The World's Greatest Investors Reveal Their Ultimate Strategies for Financial FreedomD'EverandThe Holy Grail of Investing: The World's Greatest Investors Reveal Their Ultimate Strategies for Financial FreedomÉvaluation : 5 sur 5 étoiles5/5 (7)

- The 4 Laws of Financial Prosperity: Get Conrtol of Your Money Now!D'EverandThe 4 Laws of Financial Prosperity: Get Conrtol of Your Money Now!Évaluation : 5 sur 5 étoiles5/5 (389)

- Look Again: The Power of Noticing What Was Always ThereD'EverandLook Again: The Power of Noticing What Was Always ThereÉvaluation : 5 sur 5 étoiles5/5 (3)

- Rich Dad's Cashflow Quadrant: Guide to Financial FreedomD'EverandRich Dad's Cashflow Quadrant: Guide to Financial FreedomÉvaluation : 4.5 sur 5 étoiles4.5/5 (1387)

- Psychology of Money: The Essential Guide to Building Your Wealth , Discover All the Important Information And Useful Strategies in the Pursuit of WealthD'EverandPsychology of Money: The Essential Guide to Building Your Wealth , Discover All the Important Information And Useful Strategies in the Pursuit of WealthÉvaluation : 4.5 sur 5 étoiles4.5/5 (69)

- The Millionaire Next Door: The Surprising Secrets Of Americas WealthyD'EverandThe Millionaire Next Door: The Surprising Secrets Of Americas WealthyÉvaluation : 4.5 sur 5 étoiles4.5/5 (949)