Vous aimerez peut-être aussi

- 6 Top Trends For Ambulatory Surgery Centers in 2018 PDFDocument3 pages6 Top Trends For Ambulatory Surgery Centers in 2018 PDFJuan A. SanchezPas encore d'évaluation

- The Future of Us Healthcare Whats Next For The Industry Post Covid 19Document13 pagesThe Future of Us Healthcare Whats Next For The Industry Post Covid 19miltechinsightsPas encore d'évaluation

- Team Health Stock ReportDocument59 pagesTeam Health Stock ReportDennis LiPas encore d'évaluation

- Running Head: HEALTHCARE 1Document8 pagesRunning Head: HEALTHCARE 1Eli KoechPas encore d'évaluation

- HospitalDocument32 pagesHospitalSrikanth Salvatore100% (3)

- Projected Medicare Expenditures Under An Illustrative Scenario With Alternative Payment Updates To Medicare ProvidersDocument18 pagesProjected Medicare Expenditures Under An Illustrative Scenario With Alternative Payment Updates To Medicare ProvidersTed OkonPas encore d'évaluation

- 63e64c8c4452468714ce2e3d - Strategy and Budgeting in HealthCare - ClearPoint StrategyDocument14 pages63e64c8c4452468714ce2e3d - Strategy and Budgeting in HealthCare - ClearPoint StrategySema Sadullayeva02Pas encore d'évaluation

- 7 Market Access Trends For 2027Document14 pages7 Market Access Trends For 2027Anshuman BudhirajaPas encore d'évaluation

- Robert BerensonDocument29 pagesRobert Berensonapi-239368329Pas encore d'évaluation

- Optum solutions help health plans address cost quality and revenueDocument12 pagesOptum solutions help health plans address cost quality and revenueantonettereynoldsPas encore d'évaluation

- Do You Know The Fair Market Value of Quality?: Jen JohnsonDocument8 pagesDo You Know The Fair Market Value of Quality?: Jen JohnsonG Mohan Kumar100% (1)

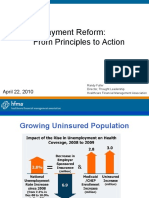

- Payment Reform: From Principles to ActionDocument34 pagesPayment Reform: From Principles to Actionibson045001256Pas encore d'évaluation

- Abstract - Jaipuria2 - Re-Engineering The Revenue CycleDocument2 pagesAbstract - Jaipuria2 - Re-Engineering The Revenue Cyclemunish_tiwari2007Pas encore d'évaluation

- LDI Issue Brief 2020 Vol. 23 No. 4 - 12Document11 pagesLDI Issue Brief 2020 Vol. 23 No. 4 - 12hamzatamer.88.10Pas encore d'évaluation

- CHG-MERIDIAN USA Whitepaper Financial Challenges For Hospital CFOsDocument8 pagesCHG-MERIDIAN USA Whitepaper Financial Challenges For Hospital CFOsApu LahiriPas encore d'évaluation

- Medical HealthDocument50 pagesMedical HealthHihiPas encore d'évaluation

- Effective Hospital Pricing StrategyDocument13 pagesEffective Hospital Pricing StrategyKaustubh SardesaiPas encore d'évaluation

- Business Proposal FinalDocument19 pagesBusiness Proposal Finalapi-408489180Pas encore d'évaluation

- MIS PricesDocument50 pagesMIS PricesAndy GuraPas encore d'évaluation

- CT Somatom Go Top Brochures Stand Out in Advanced CT Procedures Hood05162002856838 152099932Document56 pagesCT Somatom Go Top Brochures Stand Out in Advanced CT Procedures Hood05162002856838 152099932service iyadMedicalPas encore d'évaluation

- Introduction To Us Healthcare System: Trends in Premiums and Cost Sharing and Its Reasons and ImplicationsDocument9 pagesIntroduction To Us Healthcare System: Trends in Premiums and Cost Sharing and Its Reasons and ImplicationsShruti SinghPas encore d'évaluation

- 2015 Health Care Providers Outlook: United StatesDocument5 pages2015 Health Care Providers Outlook: United StatesEmma Hinchliffe100% (1)

- Data Driven Healthcare For PayersDocument24 pagesData Driven Healthcare For PayersLinda WatsonPas encore d'évaluation

- U.S. Employers Expect Health Care Costs To Rise 4% in 2015: SEPTEMBER 2014Document4 pagesU.S. Employers Expect Health Care Costs To Rise 4% in 2015: SEPTEMBER 2014Automotive Wholesalers Association of New EnglandPas encore d'évaluation

- EBOOK HEALTHCARE INTEGRATION PRESCRIPTION FOR DISRUPTIONDocument32 pagesEBOOK HEALTHCARE INTEGRATION PRESCRIPTION FOR DISRUPTIONMark ChernPas encore d'évaluation

- UnitedHealth Group, Inc. Initiating Coverage ReportDocument10 pagesUnitedHealth Group, Inc. Initiating Coverage Reportmikielam23Pas encore d'évaluation

- Ib 33 PDFDocument12 pagesIb 33 PDFLatinos Ready To VotePas encore d'évaluation

- MCO Three-Year Cost ReportDocument28 pagesMCO Three-Year Cost Reporttinareedreporter100% (1)

- Budget Negotiations and Communication Strategic PlanDocument8 pagesBudget Negotiations and Communication Strategic PlanNbiPas encore d'évaluation

- DUP436 Big Pharma2 PDFDocument16 pagesDUP436 Big Pharma2 PDFJose CMPas encore d'évaluation

- DUP436 Big Pharma2 PDFDocument16 pagesDUP436 Big Pharma2 PDFHITESH MAKHIJAPas encore d'évaluation

- Journal of Operations Management: Deepa Wani, Manoj Malhotra, Sriram VenkataramanDocument13 pagesJournal of Operations Management: Deepa Wani, Manoj Malhotra, Sriram VenkataramanSarah WaichertPas encore d'évaluation

- Value Based ProgramsDocument8 pagesValue Based ProgramsPremium GeeksPas encore d'évaluation

- Medicare Physician Pricing Objectives Evolve Toward Economic EfficiencyDocument16 pagesMedicare Physician Pricing Objectives Evolve Toward Economic EfficiencyMohammad Rusdy Al KarofiPas encore d'évaluation

- Trends in Healthcare Payments Annual Report 2015 PDFDocument38 pagesTrends in Healthcare Payments Annual Report 2015 PDFAnonymous Feglbx5Pas encore d'évaluation

- Health Insurance Trends 2020 PDFDocument28 pagesHealth Insurance Trends 2020 PDFdrarunoncoPas encore d'évaluation

- 1991 - 5 - 31 - CopieDocument20 pages1991 - 5 - 31 - CopiehakimPas encore d'évaluation

- An Empirical Analysis of Cash Flow, Working Capital, and The Stability of Financial Ratio Groups in The Hospital IndustryDocument20 pagesAn Empirical Analysis of Cash Flow, Working Capital, and The Stability of Financial Ratio Groups in The Hospital IndustryhakimPas encore d'évaluation

- Operating Budget of Healthcare OrganizationDocument15 pagesOperating Budget of Healthcare OrganizationAchacha Jr El PatronPas encore d'évaluation

- Nejmp 1312654Document2 pagesNejmp 1312654Greg GelembiukPas encore d'évaluation

- Expert Systems With Applications: Roya Gholami, Dolores Añón Higón, Ali EmrouznejadDocument11 pagesExpert Systems With Applications: Roya Gholami, Dolores Añón Higón, Ali Emrouznejadismail ajiPas encore d'évaluation

- GS China Hospitals Jan2014Document31 pagesGS China Hospitals Jan2014Sanghoon JiPas encore d'évaluation

- Critical Factors of Hospital Adoption On CRM System - Organizational and Information System PerspectivesDocument12 pagesCritical Factors of Hospital Adoption On CRM System - Organizational and Information System Perspectivesnajeeb_at_scribd100% (1)

- Strategic Management Processes in Healthcare Organizations: Abdulaziz Saddique Pharm.D., CPHQ, CSSMBBDocument10 pagesStrategic Management Processes in Healthcare Organizations: Abdulaziz Saddique Pharm.D., CPHQ, CSSMBBtheresia anggitaPas encore d'évaluation

- Business Proposal For Heartland HealthDocument20 pagesBusiness Proposal For Heartland Healthapi-3942622340% (1)

- Healthcare Trends and IssuesDocument5 pagesHealthcare Trends and IssuesAlex MunyaoPas encore d'évaluation

- Lean Management and U.S. Public Hospital Performance Results From A National SurveyDocument17 pagesLean Management and U.S. Public Hospital Performance Results From A National SurveyArnoldYRPPas encore d'évaluation

- Digital Transformation of Healthcare Industry Liquid Hub WhitepaperDocument14 pagesDigital Transformation of Healthcare Industry Liquid Hub WhitepaperNitin AmesurPas encore d'évaluation

- Letter of Support For ACOs and MSSP NPRM Sign On 09202018Document3 pagesLetter of Support For ACOs and MSSP NPRM Sign On 09202018HLMeditPas encore d'évaluation

- J - Labour EconomicsDocument8 pagesJ - Labour EconomicsTWINKLE GARGPas encore d'évaluation

- The Use and Impact of Six Sigma in Health 2Document34 pagesThe Use and Impact of Six Sigma in Health 2Georgina SulePas encore d'évaluation

- The Changing Landscape Is Good For Patients & Health Care: HospitalsDocument3 pagesThe Changing Landscape Is Good For Patients & Health Care: HospitalsGeLo L. OgadPas encore d'évaluation

- The Effects of Benefit Design and Managed Care On Care CostsDocument18 pagesThe Effects of Benefit Design and Managed Care On Care CostsKuttiyar YeamsriPas encore d'évaluation

- ACOS An Eye On Washington Quarterly (SGR)Document3 pagesACOS An Eye On Washington Quarterly (SGR)acosurgeryPas encore d'évaluation

- Hwang Health Care Cost Growth 10 ProfilesDocument38 pagesHwang Health Care Cost Growth 10 ProfilesBruhan KaggwaPas encore d'évaluation

- Healthcare Whitepaper 2013Document15 pagesHealthcare Whitepaper 2013Fouad LfnPas encore d'évaluation

- Cost ContainmentDocument52 pagesCost ContainmentAthanassios VozikisPas encore d'évaluation

- Cortana Analytics in Healthcare White PaperDocument16 pagesCortana Analytics in Healthcare White PaperDeyverson Costa100% (1)

- Leadership Skills for the New Health Economy a 5Q© ApproachD'EverandLeadership Skills for the New Health Economy a 5Q© ApproachPas encore d'évaluation

- The Art of the Heal: A Health Executive’s Guide to Innovating HospitalsD'EverandThe Art of the Heal: A Health Executive’s Guide to Innovating HospitalsPas encore d'évaluation

- $@!!@$1 NotificationDocument9 pages$@!!@$1 NotificationGade NareshPas encore d'évaluation

- GR1 150 PreambleDocument100 pagesGR1 150 PreambleGade NareshPas encore d'évaluation

- TSPSC Telangana Govt Jobs: Senior & Junior Assistant VacanciesDocument23 pagesTSPSC Telangana Govt Jobs: Senior & Junior Assistant VacanciesGade NareshPas encore d'évaluation

- Candlestick Patterns Trading GuideDocument19 pagesCandlestick Patterns Trading GuideleylPas encore d'évaluation

- Protect yourself from COVID-19Document1 pageProtect yourself from COVID-19skarthiphdPas encore d'évaluation

- 3 New Books:: Trading Price Action Trading Price Action Trading Price ActionDocument53 pages3 New Books:: Trading Price Action Trading Price Action Trading Price ActionLeszekPas encore d'évaluation

- Introduction To India PDFDocument33 pagesIntroduction To India PDFNayann NarnoliPas encore d'évaluation

- Notification SBI Sector Credit Specialist VacancyDocument2 pagesNotification SBI Sector Credit Specialist VacancyGade NareshPas encore d'évaluation

- Class 10 Mental Ability Competitive ExamsDocument160 pagesClass 10 Mental Ability Competitive Examsashish kumarPas encore d'évaluation

- 3 New Books:: Trading Price Action Trading Price Action Trading Price ActionDocument53 pages3 New Books:: Trading Price Action Trading Price Action Trading Price ActionLeszekPas encore d'évaluation

- Coronavirus Guidance Update ENGLISHDocument49 pagesCoronavirus Guidance Update ENGLISH123krishnendurayPas encore d'évaluation

- Ts 138300v150301p PDFDocument90 pagesTs 138300v150301p PDFGade NareshPas encore d'évaluation

- Candlestick DescriptionsDocument14 pagesCandlestick Descriptionsflakeman100% (3)

- Protect yourself from COVID-19Document1 pageProtect yourself from COVID-19skarthiphdPas encore d'évaluation

- 06 - Chapter 1 PDFDocument30 pages06 - Chapter 1 PDFPIYUSH KUMARPas encore d'évaluation

- Rpotc070513fl PDFDocument102 pagesRpotc070513fl PDFMahesh Shankar BorePas encore d'évaluation

- History of Mobile TelephonyDocument25 pagesHistory of Mobile Telephonyapi-424696656Pas encore d'évaluation

- Ts 138300v150301p PDFDocument90 pagesTs 138300v150301p PDFGade NareshPas encore d'évaluation

- Monthly New Residential Construction, July 2019Document7 pagesMonthly New Residential Construction, July 2019Gade NareshPas encore d'évaluation

- List of Regular VerbsDocument6 pagesList of Regular Verbsdai_anef100% (1)

- U.S. Travel and Tourism: Industry Trends and Policy Issues For CongressDocument21 pagesU.S. Travel and Tourism: Industry Trends and Policy Issues For CongressZoran H. VukchichPas encore d'évaluation

- Japan Vistor's GuideDocument64 pagesJapan Vistor's GuideMGPas encore d'évaluation

- U.S. Travel and Tourism: Industry Trends and Policy Issues For CongressDocument21 pagesU.S. Travel and Tourism: Industry Trends and Policy Issues For CongressZoran H. VukchichPas encore d'évaluation

- Overseas Visitation Estimates For U.S. States, Cities, and Census RegionsDocument6 pagesOverseas Visitation Estimates For U.S. States, Cities, and Census RegionsGade NareshPas encore d'évaluation

- ISGGEBDocument14 pagesISGGEBGade NareshPas encore d'évaluation

- American Stock Exchange Historical TimelineDocument4 pagesAmerican Stock Exchange Historical TimelineGade NareshPas encore d'évaluation

- U.S. Travel and Tourism: Industry Trends and Policy Issues For CongressDocument21 pagesU.S. Travel and Tourism: Industry Trends and Policy Issues For CongressZoran H. VukchichPas encore d'évaluation

- American Stock Exchange Historical TimelineDocument4 pagesAmerican Stock Exchange Historical TimelineGade NareshPas encore d'évaluation

- Understanding the Market for U.S. Equity Market DataDocument52 pagesUnderstanding the Market for U.S. Equity Market DataGade NareshPas encore d'évaluation

- Modbus Communication ProtocolDocument80 pagesModbus Communication ProtocolAlejandro B.Pas encore d'évaluation

- XXXXX XXXXXXXX XXX Jean-Michel Jarre: Revealed ReviewsDocument52 pagesXXXXX XXXXXXXX XXX Jean-Michel Jarre: Revealed ReviewsJennifer McdonaldPas encore d'évaluation

- BEA 242 Introduction To Econometrics Group Assignment (Updated On 10 May 2012: The Change in Highlighted)Document4 pagesBEA 242 Introduction To Econometrics Group Assignment (Updated On 10 May 2012: The Change in Highlighted)Reza Riantono SukarnoPas encore d'évaluation

- A User Guide Advanced Diagnostic Tools ADT View Software ENDocument43 pagesA User Guide Advanced Diagnostic Tools ADT View Software ENAlex ZXPas encore d'évaluation

- 16 Set 1 b2 08.06 Listening Answer KeyDocument6 pages16 Set 1 b2 08.06 Listening Answer KeyKocsisAndrásPas encore d'évaluation

- Metro Service Schedule InsightsDocument16 pagesMetro Service Schedule InsightsAtul KumarPas encore d'évaluation

- MCS in NepalDocument8 pagesMCS in NepalSourabh InaniPas encore d'évaluation

- REIT Industry OutlookDocument49 pagesREIT Industry OutlookNicholas FrenchPas encore d'évaluation

- Data Man 200 Reader COGNEXDocument22 pagesData Man 200 Reader COGNEXadelbzhPas encore d'évaluation

- RM Question and AnswerDocument19 pagesRM Question and AnswerPadmavathiPas encore d'évaluation

- The Tamil Nadu Dr. M.G.R. Medical University - MSC Nursing Second YrDocument10 pagesThe Tamil Nadu Dr. M.G.R. Medical University - MSC Nursing Second YrNoufal100% (1)

- KPSC Assistant Professor in CS Question PaperDocument22 pagesKPSC Assistant Professor in CS Question PaperBabaPas encore d'évaluation

- Ista 2BDocument5 pagesIsta 2Bduygu9merve100% (1)

- NPT 1200 - R1 NotesDocument28 pagesNPT 1200 - R1 NotesJaime Garcia De Paredes100% (4)

- Vat AssDocument6 pagesVat AssRhanda BernardoPas encore d'évaluation

- Test 1Document12 pagesTest 1kashif aliPas encore d'évaluation

- GIS Midterm Exam for AB Engineering StudentsDocument1 pageGIS Midterm Exam for AB Engineering StudentsKristeen PrusiaPas encore d'évaluation

- ASSIGNMENT Drug AbuseDocument28 pagesASSIGNMENT Drug Abuseknj210110318Pas encore d'évaluation

- Data Flow Diagrams - Set 2Document72 pagesData Flow Diagrams - Set 2Blessing MotaungPas encore d'évaluation

- Clerical Model Solved Paper 1Document15 pagesClerical Model Solved Paper 1himita desaiPas encore d'évaluation

- LKPD ApplicationLetterDocument5 pagesLKPD ApplicationLetterDheaPas encore d'évaluation

- Suon Bai S WDocument1 pageSuon Bai S WNgoc ThanhPas encore d'évaluation

- SB66JRT English Hoogwerker Aerial Lift SnorkelDocument2 pagesSB66JRT English Hoogwerker Aerial Lift Snorkelhoogwerker0% (1)

- Bar Bending Schedule for Duct Bank EDB-068001Document7 pagesBar Bending Schedule for Duct Bank EDB-068001costonzPas encore d'évaluation

- CH 3030 Applications of Mass Transfer: 4 August 2020Document17 pagesCH 3030 Applications of Mass Transfer: 4 August 2020Ram Lakhan MeenaPas encore d'évaluation

- Focus Plastics Case StudyDocument8 pagesFocus Plastics Case StudyraiaPas encore d'évaluation

- OBR Assignment 2 Team D 1Document5 pagesOBR Assignment 2 Team D 1kazi noor ahmedPas encore d'évaluation

- If TRLDocument38 pagesIf TRLbdPas encore d'évaluation

- Astm C31-C31M-23Document7 pagesAstm C31-C31M-23mustafa97a141Pas encore d'évaluation

- ICAR Annual Report-2017-18 - (English) PDFDocument205 pagesICAR Annual Report-2017-18 - (English) PDFgautamcsg100% (1)