Vous aimerez peut-être aussi

- Understanding the BSP's Authority to Suspend Interest Rate CeilingsDocument3 pagesUnderstanding the BSP's Authority to Suspend Interest Rate Ceilingsrobby100% (1)

- 123 VICTORIANO vs. ELIZALDE ROPE WORKERS' UNIONDocument4 pages123 VICTORIANO vs. ELIZALDE ROPE WORKERS' UNIONrobbyPas encore d'évaluation

- 123 VICTORIANO vs. ELIZALDE ROPE WORKERS' UNIONDocument4 pages123 VICTORIANO vs. ELIZALDE ROPE WORKERS' UNIONrobbyPas encore d'évaluation

- Mod1 - 5 - G.R. No. L-19342 Ona V CIRDocument2 pagesMod1 - 5 - G.R. No. L-19342 Ona V CIROjie SantillanPas encore d'évaluation

- Organization and Environmental Factors: S.Bharathi Mca, Mba., M.Phil, PGDPM&LLDocument25 pagesOrganization and Environmental Factors: S.Bharathi Mca, Mba., M.Phil, PGDPM&LLbharathimanian100% (1)

- CIR v. San Miguel CorporationDocument1 pageCIR v. San Miguel CorporationKym AlgarmePas encore d'évaluation

- Administrative Remedies of The GovernmentDocument5 pagesAdministrative Remedies of The GovernmentrobbyPas encore d'évaluation

- HOLIDAY INN MANILA v. NLRCDocument2 pagesHOLIDAY INN MANILA v. NLRCrobbyPas encore d'évaluation

- Mactan Cebu International Airport Authority v. MarcosDocument2 pagesMactan Cebu International Airport Authority v. MarcosKabataan Party-List100% (5)

- 045 - Shell Co V Vano (1954) - SubidoDocument2 pages045 - Shell Co V Vano (1954) - SubidoFrancis Kyle Cagalingan Subido100% (1)

- Limpan Investment Corp v. CIR, 17 SCRA 703Document2 pagesLimpan Investment Corp v. CIR, 17 SCRA 703Gabriel Hernandez100% (1)

- 3.4 Victoriano V Elizalde Rope Workers' UnionDocument3 pages3.4 Victoriano V Elizalde Rope Workers' UnionrobbyPas encore d'évaluation

- 07 DELPHER-TRADES V IACDocument4 pages07 DELPHER-TRADES V IACElla CanuelPas encore d'évaluation

- Phil. Guaranty Co. v. CIRDocument2 pagesPhil. Guaranty Co. v. CIRIshPas encore d'évaluation

- Delpher Trades Corp. v. IAC ruling on alter ego statusDocument2 pagesDelpher Trades Corp. v. IAC ruling on alter ego statusBingoheartPas encore d'évaluation

- The Payment of The Bonus Act 1965Document28 pagesThe Payment of The Bonus Act 1965Arpita Acharjya100% (1)

- Republic Bank v. CTA DigestDocument3 pagesRepublic Bank v. CTA DigestKaren Panisales100% (2)

- Corporate Law ProjectDocument15 pagesCorporate Law Projectbhargavi mishraPas encore d'évaluation

- Chamber of Real Estate and Builders' Assoc. Vs Hon. Exec. Sec. Alberto RomuloDocument2 pagesChamber of Real Estate and Builders' Assoc. Vs Hon. Exec. Sec. Alberto RomuloRhea Mae Lasay-Sumpiao100% (1)

- Government Tax Claims Exempt from Non-Claims StatuteDocument1 pageGovernment Tax Claims Exempt from Non-Claims StatuteIshPas encore d'évaluation

- XDocument2 pagesXSophiaFrancescaEspinosaPas encore d'évaluation

- 01 Rivera v. ChuaDocument1 page01 Rivera v. ChuarobbyPas encore d'évaluation

- FAR Assignment 1Document3 pagesFAR Assignment 1Abegail Marababol50% (12)

- Finals DigestDocument172 pagesFinals DigestMarco MarianoPas encore d'évaluation

- Delpher Trades Corporation v. Iac Case DigestDocument3 pagesDelpher Trades Corporation v. Iac Case DigestHappy Damasing67% (3)

- CIR vs. PNB 736 SCRA 609 2014 VELOSODocument2 pagesCIR vs. PNB 736 SCRA 609 2014 VELOSOAnonymous MikI28PkJc100% (2)

- Affidavit of Proof of DebtDocument2 pagesAffidavit of Proof of DebtFahim KhanPas encore d'évaluation

- CIR Vs PLDT DigestDocument3 pagesCIR Vs PLDT DigestKath Leen100% (3)

- Domingo vs. GarlitosDocument2 pagesDomingo vs. GarlitosMichellePas encore d'évaluation

- Caltex v. COA DigestDocument2 pagesCaltex v. COA Digestpinkblush717100% (1)

- 02 de Leon v. RodriguezDocument2 pages02 de Leon v. Rodriguezrobby100% (2)

- Commissioner of Internal Revenue v. Manila Jockey Club, 108 Phil 281Document2 pagesCommissioner of Internal Revenue v. Manila Jockey Club, 108 Phil 281Charles Roger Raya100% (1)

- CIR Vs The Estate of TodaDocument3 pagesCIR Vs The Estate of TodaLDPas encore d'évaluation

- CIR vs. Goodyear 216130Document1 pageCIR vs. Goodyear 216130magenPas encore d'évaluation

- What This Is For:: BIR Form 1905Document7 pagesWhat This Is For:: BIR Form 1905shfskjdgbPas encore d'évaluation

- Fisher V Trinidad DigestDocument1 pageFisher V Trinidad DigestDario G. TorresPas encore d'évaluation

- 2008 Bar Questions and AnswersDocument15 pages2008 Bar Questions and AnswersimoymitoPas encore d'évaluation

- Tax deduction for unpaid war damage claim deniedDocument2 pagesTax deduction for unpaid war damage claim deniedAlan Gultia100% (1)

- Atlas Consolidated Mining Development Corp. v. CIRDocument1 pageAtlas Consolidated Mining Development Corp. v. CIRIshPas encore d'évaluation

- Nike FinalDocument24 pagesNike FinalShivayu VaidPas encore d'évaluation

- Marcos II V CADocument3 pagesMarcos II V CArobbyPas encore d'évaluation

- Eisner v. Macomber, 252 US 89, SupraDocument2 pagesEisner v. Macomber, 252 US 89, SupraMaria Fiona Duran Merquita100% (1)

- Arturo M. Tolentino Vs Secretary of Finance DigestDocument4 pagesArturo M. Tolentino Vs Secretary of Finance DigestAbilene Joy Dela Cruz0% (1)

- Serafica v. City Treasurer of OrmocDocument1 pageSerafica v. City Treasurer of OrmocEarl LarroderPas encore d'évaluation

- Dna ModuleDocument8 pagesDna ModulerobbyPas encore d'évaluation

- TAX 2: Digest - Winebrenner & Iñigo Insurance Brokers, Inc. v. CIRDocument2 pagesTAX 2: Digest - Winebrenner & Iñigo Insurance Brokers, Inc. v. CIRFaith Marie Borden100% (2)

- MTBC VS JMCDocument4 pagesMTBC VS JMCRichelle CartinPas encore d'évaluation

- ANPC vs. BIRDocument2 pagesANPC vs. BIRAnnePas encore d'évaluation

- Ona Vs CIR DigestDocument2 pagesOna Vs CIR Digestannamariepagtabunan86% (7)

- 03 Jao vs. CADocument2 pages03 Jao vs. CArobbyPas encore d'évaluation

- 03 Jao vs. CADocument2 pages03 Jao vs. CArobbyPas encore d'évaluation

- Calalang v. LorenzoDocument1 pageCalalang v. LorenzoJay-ar Rivera BadulisPas encore d'évaluation

- CIR v. CADocument2 pagesCIR v. CAKristina Karen100% (1)

- LG Electronics V CIRDocument2 pagesLG Electronics V CIRCarla CucuecoPas encore d'évaluation

- Domingo vs. Garlitos (8 SCRA 443, G.R. No. L-18994, June 29, 1963)Document1 pageDomingo vs. Garlitos (8 SCRA 443, G.R. No. L-18994, June 29, 1963)Jennilyn Gulfan YasePas encore d'évaluation

- Aznar Vs CtaDocument2 pagesAznar Vs CtarobbyPas encore d'évaluation

- Madrigal Vs RaffertyDocument2 pagesMadrigal Vs RaffertyKirs Tie100% (1)

- Madrigal Vs RaffertyDocument3 pagesMadrigal Vs RaffertyMJ BautistaPas encore d'évaluation

- Taxation of Gain from Sale of Nasugbu Farm LandsDocument1 pageTaxation of Gain from Sale of Nasugbu Farm LandsJoshua Erik Madria100% (1)

- Abscbn Broadcasting Corp. v. Cta DigestDocument3 pagesAbscbn Broadcasting Corp. v. Cta DigestkathrynmaydevezaPas encore d'évaluation

- TAN Vs DEL ROSARIODocument3 pagesTAN Vs DEL ROSARIOKath LeenPas encore d'évaluation

- Maloles II vs Phillips | Jurisdiction over probate proceedingsDocument4 pagesMaloles II vs Phillips | Jurisdiction over probate proceedingsrobbyPas encore d'évaluation

- Javier vs. Commissioner Ancheta: CTA CASE NO 3393 JULY 27, 1983 Rean GonzalesDocument7 pagesJavier vs. Commissioner Ancheta: CTA CASE NO 3393 JULY 27, 1983 Rean GonzalesRean Raphaelle GonzalesPas encore d'évaluation

- Judge fined for acting as real estate brokerDocument3 pagesJudge fined for acting as real estate brokerilovetwentyonepilots100% (1)

- Reyes v. AlmanzorDocument5 pagesReyes v. AlmanzorPatricia BautistaPas encore d'évaluation

- Surety Company Deduction CaseDocument1 pageSurety Company Deduction CaseKyle DionisioPas encore d'évaluation

- Malayan Insurance Company, Inc., vs. St. Francis Square Realty CorporationDocument2 pagesMalayan Insurance Company, Inc., vs. St. Francis Square Realty CorporationnanyerPas encore d'évaluation

- II. INCOME - Bir Rulings Revenue Regulations: in General Statutory "Inclusions"Document37 pagesII. INCOME - Bir Rulings Revenue Regulations: in General Statutory "Inclusions"Polo MartinezPas encore d'évaluation

- Aguinaldo Industries Corporation vs. Commissioner of Internal Revenue Services Actually RenderedDocument2 pagesAguinaldo Industries Corporation vs. Commissioner of Internal Revenue Services Actually RenderedCharmila SiplonPas encore d'évaluation

- PEOPLE v. MENDEZ, G.R. No. 208310-11Document4 pagesPEOPLE v. MENDEZ, G.R. No. 208310-11ohohmaddiPas encore d'évaluation

- Ong Chua V. Edward Carr Et AlDocument4 pagesOng Chua V. Edward Carr Et AlrobbyPas encore d'évaluation

- Bpi V Cir DigestDocument3 pagesBpi V Cir DigestkathrynmaydevezaPas encore d'évaluation

- Delpher Trades Corporation vs. IACDocument1 pageDelpher Trades Corporation vs. IACGeoanne Battad Beringuela100% (1)

- Raytheon Settlement Deemed Taxable IncomeDocument2 pagesRaytheon Settlement Deemed Taxable IncomeCharles Roger RayaPas encore d'évaluation

- Southern Cross Cement v. Cement Manufacturer's Assoc., G.R. No. 158540, 2005Document2 pagesSouthern Cross Cement v. Cement Manufacturer's Assoc., G.R. No. 158540, 2005JMae Magat100% (1)

- COMMISSIONER OF INTERNAL REVENUE, Petitioner, vs. CITYTRUST INVESTMENT PHILS., INC., Respondent.Document1 pageCOMMISSIONER OF INTERNAL REVENUE, Petitioner, vs. CITYTRUST INVESTMENT PHILS., INC., Respondent.Charles Roger Raya100% (1)

- Philex Mining Vs Cir DigestDocument3 pagesPhilex Mining Vs Cir DigestRyan Acosta100% (2)

- Pelizloy Realty Corp. Vs Province of Benguet, GR No. 183137, 10 April 2013Document2 pagesPelizloy Realty Corp. Vs Province of Benguet, GR No. 183137, 10 April 2013Catherine Dawn Maunes100% (1)

- (Digest) Obillos V CIRDocument2 pages(Digest) Obillos V CIRGR100% (3)

- YMCA v. CIR, 298 SCRA - THE LIFEBLOOD DOCTRINE - DigestDocument2 pagesYMCA v. CIR, 298 SCRA - THE LIFEBLOOD DOCTRINE - DigestKate GaroPas encore d'évaluation

- The City of Iloilo Vs Smart Communications, Inc. Taxation 2 DigestDocument3 pagesThe City of Iloilo Vs Smart Communications, Inc. Taxation 2 DigestEllen Glae DaquipilPas encore d'évaluation

- AFISCO v. CADocument2 pagesAFISCO v. CASophiaFrancescaEspinosa100% (1)

- Delpher Trades Corporation v. IACDocument2 pagesDelpher Trades Corporation v. IACMirellaPas encore d'évaluation

- Right of First Refusal CaseDocument4 pagesRight of First Refusal Casejames lebronPas encore d'évaluation

- 5. Delpher Trades and Pacheco v. IAC (1)Document1 page5. Delpher Trades and Pacheco v. IAC (1)AdrianPas encore d'évaluation

- Foreign Investments Act of 1991Document5 pagesForeign Investments Act of 1991Marien Gonzales LopezPas encore d'évaluation

- SPECPRO Week 1 CompilationDocument26 pagesSPECPRO Week 1 CompilationrobbyPas encore d'évaluation

- OXALES v. UNITED LABORATORIESDocument2 pagesOXALES v. UNITED LABORATORIESrobbyPas encore d'évaluation

- Invit. Letter of Army & ResponseDocument3 pagesInvit. Letter of Army & ResponserobbyPas encore d'évaluation

- University of The Philippines Diliman: Check With Respective CollegesDocument1 pageUniversity of The Philippines Diliman: Check With Respective CollegesMeowthemathicianPas encore d'évaluation

- Q & A On Batas Kasambahay (RA No 10361) PDFDocument8 pagesQ & A On Batas Kasambahay (RA No 10361) PDFchristimyvPas encore d'évaluation

- PRIL DigestsDocument12 pagesPRIL DigestsrobbyPas encore d'évaluation

- Malcolm Cup 2019 PDFDocument5 pagesMalcolm Cup 2019 PDFrobbyPas encore d'évaluation

- The Federalist Paper 78Document5 pagesThe Federalist Paper 78robbyPas encore d'évaluation

- PRIL DigestsDocument14 pagesPRIL DigestsrobbyPas encore d'évaluation

- Malcolm Cup 2019 PDFDocument5 pagesMalcolm Cup 2019 PDFrobbyPas encore d'évaluation

- Malcolm Cup 2019 PDFDocument5 pagesMalcolm Cup 2019 PDFrobbyPas encore d'évaluation

- Sidel RulingDocument6 pagesSidel RulingMarc Exequiel TeodoroPas encore d'évaluation

- Ayala CirDocument1 pageAyala CirrobbyPas encore d'évaluation

- California Corporate Formation QuestionnaireDocument6 pagesCalifornia Corporate Formation QuestionnaireDavid OshinskyPas encore d'évaluation

- Expedicao Continua 12.1.33 Backoffice ContentsDocument122 pagesExpedicao Continua 12.1.33 Backoffice ContentsAlexandre ZennaroPas encore d'évaluation

- SERVICE Excellence Kang DedeDocument38 pagesSERVICE Excellence Kang Dededede muharramPas encore d'évaluation

- Plastic Money in IndiaDocument71 pagesPlastic Money in IndiaDexter LoboPas encore d'évaluation

- 321.carole Ann AinioDocument2 pages321.carole Ann AinioFlinders TrusteesPas encore d'évaluation

- Empresa ILEDocument6 pagesEmpresa ILEVerónica AlcívarPas encore d'évaluation

- SA220Document22 pagesSA220Laura D'souza0% (1)

- Tax Manager Job Description ExpertiseDocument1 pageTax Manager Job Description Expertisetino mediamudaPas encore d'évaluation

- New York State Urban Development Corporation D/b/a Empire State DevelopmentDocument166 pagesNew York State Urban Development Corporation D/b/a Empire State DevelopmentjspectorPas encore d'évaluation

- Catherine A. Rojo Commission # Notary Public - California Comm Exres Jun 26201 Los Angeles CountyDocument3 pagesCatherine A. Rojo Commission # Notary Public - California Comm Exres Jun 26201 Los Angeles CountyChapter 11 DocketsPas encore d'évaluation

- Principal Adviser Principal Adviser Principal Adviser Principal Adviser Principal AdviserDocument74 pagesPrincipal Adviser Principal Adviser Principal Adviser Principal Adviser Principal AdviserCheong Wei HaoPas encore d'évaluation

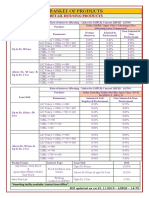

- BASKET OF RETAIL PRODUCTS RATESDocument3 pagesBASKET OF RETAIL PRODUCTS RATESVirendra K VermaPas encore d'évaluation

- Mergers and AcquisitionsDocument4 pagesMergers and AcquisitionsАлина ХмилевскаяPas encore d'évaluation

- Stock MarketDocument697 pagesStock MarketSachin SharmaPas encore d'évaluation

- GO MS No.29Document5 pagesGO MS No.29kvjraghunathPas encore d'évaluation

- CRB Complete ScamDocument8 pagesCRB Complete ScamOkkishorePas encore d'évaluation

- India's Leading Travel Show Focused On Business Travel and MICEDocument4 pagesIndia's Leading Travel Show Focused On Business Travel and MICEKiara MpPas encore d'évaluation

- Quiz Partnership 1Document2 pagesQuiz Partnership 1Arj Sulit Centino DaquiPas encore d'évaluation

- The Handbook Direct MarketingDocument11 pagesThe Handbook Direct MarketingEarl Russell S PaulicanPas encore d'évaluation

- Sample Ch01Document39 pagesSample Ch01wingssPas encore d'évaluation

- CORPORATE GOVERNANCE AWARDSDocument5 pagesCORPORATE GOVERNANCE AWARDSMaya BarcoPas encore d'évaluation