Vous aimerez peut-être aussi

- An Introduction To OptionsDocument65 pagesAn Introduction To OptionsmagimaidossPas encore d'évaluation

- Option Strategies - WSDocument10 pagesOption Strategies - WSSrilekha BasavojuPas encore d'évaluation

- Net ProfitDocument43 pagesNet ProfitAmisha ShrivastavPas encore d'évaluation

- Scoresheet Electronic QbowlDocument30 pagesScoresheet Electronic QbowlAnand KamannavarPas encore d'évaluation

- 04 Forwards - Graphs - XLSBDocument6 pages04 Forwards - Graphs - XLSBYousef KhanPas encore d'évaluation

- Female Weight For Age Height For AgeDocument1 pageFemale Weight For Age Height For AgeAng Fei FeiPas encore d'évaluation

- Date Particular Units Rate AmountDocument7 pagesDate Particular Units Rate AmountUmair HayatPas encore d'évaluation

- Prob 2Document247 pagesProb 2abuzarPas encore d'évaluation

- Exercise Test Weight Reps Set Interval Tonnage Cutoff 1Rm 5Rm Squat Bench Row Press Deadlift Smallest Plates Available Match Prs in Week #Document7 pagesExercise Test Weight Reps Set Interval Tonnage Cutoff 1Rm 5Rm Squat Bench Row Press Deadlift Smallest Plates Available Match Prs in Week #Chelsea ClarkPas encore d'évaluation

- Foods From ChileDocument1 pageFoods From ChileAsraelPas encore d'évaluation

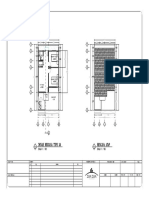

- Zam Zam: Kamar Tidur 0.00 KM / WC - 0.05Document10 pagesZam Zam: Kamar Tidur 0.00 KM / WC - 0.05EnyPas encore d'évaluation

- Monday Reps Week 1 Week 2 Week 3 Squat: Assistance ExercisesDocument4 pagesMonday Reps Week 1 Week 2 Week 3 Squat: Assistance ExercisesTrevor AlbertPas encore d'évaluation

- F&O - Payoff Table and GraphDocument38 pagesF&O - Payoff Table and GraphYash GehlotPas encore d'évaluation

- Bill-Starr-5x5-.Xlsx - Copy of Copy of 5x5 by PoundDocument3 pagesBill-Starr-5x5-.Xlsx - Copy of Copy of 5x5 by PoundRuan Terluk BodnarPas encore d'évaluation

- Chart Title: X y X y X y X - 14 0 - 4 0 6 - 6 11 - 14 4 - 4 8 6 0 11 - 14 8.5 - 8 - 6.5 6 4 13 - 14.7 - 16 - 8 10 7 10 13Document4 pagesChart Title: X y X y X y X - 14 0 - 4 0 6 - 6 11 - 14 4 - 4 8 6 0 11 - 14 8.5 - 8 - 6.5 6 4 13 - 14.7 - 16 - 8 10 7 10 13Andres Camilo Navarro MonterrosaPas encore d'évaluation

- Event Round Moderator Room TeamsDocument40 pagesEvent Round Moderator Room TeamsAnand KamannavarPas encore d'évaluation

- HW7Document1 pageHW7James PerkinsPas encore d'évaluation

- (Part2) NoPart1Document5 pages(Part2) NoPart1chicao haPas encore d'évaluation

- StrongLifts Madcow 5x5.Document9 pagesStrongLifts Madcow 5x5.Raffaele TestaPas encore d'évaluation

- Book 1Document5 pagesBook 1akash advisorsPas encore d'évaluation

- DCP On TP 4Document5 pagesDCP On TP 4Demsew AdelahuPas encore d'évaluation

- Penilaian Tugas PRaktekDocument2 pagesPenilaian Tugas PRaktekboksaiPas encore d'évaluation

- Business Economic-1Document14 pagesBusiness Economic-1kt05284Pas encore d'évaluation

- Caracteristici Dominante Now Prefered A B C D A B C DDocument4 pagesCaracteristici Dominante Now Prefered A B C D A B C DszilagyiPas encore d'évaluation

- 5x5 Advanced (Aka StrongLifts Advanced)Document3 pages5x5 Advanced (Aka StrongLifts Advanced)vVipezPas encore d'évaluation

- Visit The Complete Version of This Tutorial inDocument23 pagesVisit The Complete Version of This Tutorial inChetan PatilPas encore d'évaluation

- Greyskull TemplateDocument25 pagesGreyskull Templateasza121Pas encore d'évaluation

- Day Date Sets Reps Misc Inc Inc IncDocument5 pagesDay Date Sets Reps Misc Inc Inc IncTim Donahey100% (3)

- The Beergame: A Role Play Supply Chain Simulation Materials by Kai RiemerDocument19 pagesThe Beergame: A Role Play Supply Chain Simulation Materials by Kai RiemerJelyne PachecoPas encore d'évaluation

- Determine Your Unique Question Analysis Conditions:: To Be Submitted With Your ReportDocument1 pageDetermine Your Unique Question Analysis Conditions:: To Be Submitted With Your ReportMakhosonke MkhonzaPas encore d'évaluation

- CCC LingDocument1 pageCCC LingCindyPas encore d'évaluation

- Juggernaut Method Base TemplateDocument3 pagesJuggernaut Method Base TemplatePatbarbellPas encore d'évaluation

- Bill Starr 5x5Document18 pagesBill Starr 5x5Joe MotherfuckerPas encore d'évaluation

- Punto PinchDocument3 pagesPunto PinchAdrian RosePas encore d'évaluation

- Bear Spread Payoff Strategy CalculationDocument3 pagesBear Spread Payoff Strategy CalculationMukund KumarPas encore d'évaluation

- Jogo Das 3 Pistas Sem Com TemporizadorDocument16 pagesJogo Das 3 Pistas Sem Com TemporizadorDaniloArrudaPas encore d'évaluation

- Vozni Red Vozni Red: Glavni Kolodvor - Kajzerica - Lanište 234 Glavni Kolodvor - Kajzerica - Lanište 234Document1 pageVozni Red Vozni Red: Glavni Kolodvor - Kajzerica - Lanište 234 Glavni Kolodvor - Kajzerica - Lanište 234Tina KovačevićPas encore d'évaluation

- Sen Cos y TanhDocument4 pagesSen Cos y TanhalbiittaPas encore d'évaluation

- Stock Price at Expirati OnDocument5 pagesStock Price at Expirati Onvirat kohliPas encore d'évaluation

- Short Call Condor: Short 1 Itm Call + Long 1 Itm Call + Long 1 Otm Call + Short 1 Otm CallDocument7 pagesShort Call Condor: Short 1 Itm Call + Long 1 Itm Call + Long 1 Otm Call + Short 1 Otm Callmanpreet1810878135Pas encore d'évaluation

- VSeal VLDocument1 pageVSeal VLNoranda AnelytaPas encore d'évaluation

- IR Fare SuburbanDocument4 pagesIR Fare SuburbanbharathbuddyPas encore d'évaluation

- IR Fare SuburbanDocument4 pagesIR Fare SuburbanSoumabho ParuiPas encore d'évaluation

- IR Fare SuburbanDocument4 pagesIR Fare SuburbanPandiyanPas encore d'évaluation

- Weight Room Power Sets-Specific Sets ChartiiDocument31 pagesWeight Room Power Sets-Specific Sets Chartiiapi-413915581Pas encore d'évaluation

- Stronglifts 5x5 AdvancedDocument6 pagesStronglifts 5x5 Advancedrbn brbPas encore d'évaluation

- ITEM TYPE Volume Buying Price /piece Selling Price /piece Shipping Price /pieceDocument2 pagesITEM TYPE Volume Buying Price /piece Selling Price /piece Shipping Price /piecevishal gogiaPas encore d'évaluation

- Vozni Red Vozni Red: Dubrava - Markuševec - Bidrovec 205 Dubrava - Markuševec - Bidrovec 205Document1 pageVozni Red Vozni Red: Dubrava - Markuševec - Bidrovec 205 Dubrava - Markuševec - Bidrovec 205NK Devetka SenioriPas encore d'évaluation

- Presentasi - SCM 2 - Role Retailer - Kelompok 8Document21 pagesPresentasi - SCM 2 - Role Retailer - Kelompok 8Muhammad DanielPas encore d'évaluation

- Sai Kumar Vijay Anil Padmaja Sirisha Uday: Game - 1 Game - 2 Game - 3 Game - 4 Game - 5 TotalDocument1 pageSai Kumar Vijay Anil Padmaja Sirisha Uday: Game - 1 Game - 2 Game - 3 Game - 4 Game - 5 Totalsai kumarPas encore d'évaluation

- 2017-05-03 214 GradebookDocument5 pages2017-05-03 214 Gradebookapi-356487372Pas encore d'évaluation

- Endurance Warm Up Test SetsDocument24 pagesEndurance Warm Up Test Setsapi-413915581Pas encore d'évaluation

- JadualDocument1 pageJadualAbu MansurPas encore d'évaluation

- Detail Kusen Pj1 (1 Unit) SKALA 1:20 Detail Kusen P1 (2 Unit) SKALA 1:20 Detail Kusen P2 (3 Unit) SKALA 1:20Document1 pageDetail Kusen Pj1 (1 Unit) SKALA 1:20 Detail Kusen P1 (2 Unit) SKALA 1:20 Detail Kusen P2 (3 Unit) SKALA 1:20adi prasetyoPas encore d'évaluation

- Parcial Problem A 2Document5 pagesParcial Problem A 2Santiago Rodríguez CantoPas encore d'évaluation

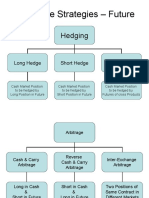

- Derivative Strategies - Future: HedgingDocument22 pagesDerivative Strategies - Future: HedgingKaran PatilPas encore d'évaluation

- CARTACrontrolDocument18 pagesCARTACrontrolMariana GómezPas encore d'évaluation

- Juggernaut Method Spreadsheet Without AssistanceDocument3 pagesJuggernaut Method Spreadsheet Without AssistanceRolphulPas encore d'évaluation

- Juggernaut Method Spreadsheet Without AssistanceDocument3 pagesJuggernaut Method Spreadsheet Without AssistanceRolphulPas encore d'évaluation

- Taxguru - In-Procedure For Formation of Private and Public Company in IndiaDocument15 pagesTaxguru - In-Procedure For Formation of Private and Public Company in IndiaRam IyerPas encore d'évaluation

- CGST Act 2017 PDFDocument103 pagesCGST Act 2017 PDFRam IyerPas encore d'évaluation

- Taxguru - In-Incorporation of Producer Company Companies Act 2013Document12 pagesTaxguru - In-Incorporation of Producer Company Companies Act 2013Ram IyerPas encore d'évaluation

- FAQs On Producer Companies ICSI PDFDocument35 pagesFAQs On Producer Companies ICSI PDFsandeepPas encore d'évaluation

- Concept of Small Shareholder DirectorDocument4 pagesConcept of Small Shareholder DirectorRam IyerPas encore d'évaluation

- Critical Issues - SEBI Listing Regulations 2015-7.4.2018 by CS S Sudhakar PDFDocument91 pagesCritical Issues - SEBI Listing Regulations 2015-7.4.2018 by CS S Sudhakar PDFRam IyerPas encore d'évaluation

- Set Off and Carry Forward of Losses An AnalysisDocument6 pagesSet Off and Carry Forward of Losses An AnalysisRam IyerPas encore d'évaluation

- Penalties Under The Income Tax Act 1961Document10 pagesPenalties Under The Income Tax Act 1961Ram IyerPas encore d'évaluation

- Nagpur BranchDocument21 pagesNagpur BranchRam IyerPas encore d'évaluation

- Listing Agreement ClausesDocument3 pagesListing Agreement ClausesMrudula NutakkiPas encore d'évaluation

- No - SEBI/LAD-NRO/GN/2015-16/013In Exercise of The Powers Conferred by Section 11, SubDocument101 pagesNo - SEBI/LAD-NRO/GN/2015-16/013In Exercise of The Powers Conferred by Section 11, SubPatrickLnanduPas encore d'évaluation

- Critical Issues - SEBI Listing Regulations 2015-7.4.2018 by CS S Sudhakar PDFDocument91 pagesCritical Issues - SEBI Listing Regulations 2015-7.4.2018 by CS S Sudhakar PDFRam IyerPas encore d'évaluation

- Working Paper 173 PDFDocument40 pagesWorking Paper 173 PDFRam IyerPas encore d'évaluation

- 74 PDFDocument3 pages74 PDFRam IyerPas encore d'évaluation

- A Study On The Corporate Governance Issues at SATYAMDocument18 pagesA Study On The Corporate Governance Issues at SATYAMSomiya91% (22)

- CSR Final 02022015Document84 pagesCSR Final 02022015Ram IyerPas encore d'évaluation

- CSR Final 02022015 PDFDocument84 pagesCSR Final 02022015 PDFRam IyerPas encore d'évaluation

- Summarize MCQs PDFDocument32 pagesSummarize MCQs PDFRam IyerPas encore d'évaluation

- Corporate Governance Case Studies CataloguesDocument12 pagesCorporate Governance Case Studies CataloguesAnita PanthakiPas encore d'évaluation

- Satyam Fiasco Corporate Governance FailuDocument11 pagesSatyam Fiasco Corporate Governance FailuRam IyerPas encore d'évaluation

- Practice Questions Valuations & Business Modelling PDFDocument103 pagesPractice Questions Valuations & Business Modelling PDFRam Iyer0% (1)

- Working Paper 173Document40 pagesWorking Paper 173Ram IyerPas encore d'évaluation

- Valuation ProblemsDocument2 pagesValuation ProblemsRam IyerPas encore d'évaluation

- Brealey. Myers. Allen Chapter 21 TestDocument15 pagesBrealey. Myers. Allen Chapter 21 TestSasha100% (1)

- Director LMRDocument17 pagesDirector LMRPriyanshi SinghPas encore d'évaluation

- Gtal - 2016 - Valuations of Sme Pres Phill R PDFDocument21 pagesGtal - 2016 - Valuations of Sme Pres Phill R PDFRam IyerPas encore d'évaluation

- Private CompanyDocument180 pagesPrivate CompanyRam IyerPas encore d'évaluation

- Costing Formula SheetDocument16 pagesCosting Formula SheetRam Iyer100% (1)

- Aclp 2018Document728 pagesAclp 2018Ram IyerPas encore d'évaluation

- Green Shoe Options in IndiaDocument32 pagesGreen Shoe Options in IndiaRajeev AroraPas encore d'évaluation

- CEMA Brochure PDFDocument2 pagesCEMA Brochure PDFKumar RajputPas encore d'évaluation

- Equity Derivatives NCFM PDFDocument148 pagesEquity Derivatives NCFM PDFsarankumararamco100% (2)

- Ch10 HW SolutionsDocument43 pagesCh10 HW Solutionsgilli1trPas encore d'évaluation

- Exchange-Traded Funds: An Introduction: and Further Likely EvolutionDocument9 pagesExchange-Traded Funds: An Introduction: and Further Likely EvolutionNathália Alves de JesusPas encore d'évaluation

- Saim NotesDocument120 pagesSaim NotesJagmohan Bisht0% (1)

- Modified Dietz MethodDocument46 pagesModified Dietz MethodprmushayiPas encore d'évaluation

- The Market Maker's MatrixDocument72 pagesThe Market Maker's Matrixjlaudirt100% (4)

- "What Is " ا: َب ِّ رلا " (THE RIBA) ?Document11 pages"What Is " ا: َب ِّ رلا " (THE RIBA) ?Zaki AlattarPas encore d'évaluation

- PMEX Gold 100 Gms Futures Contracts Specifications: ST ST STDocument3 pagesPMEX Gold 100 Gms Futures Contracts Specifications: ST ST STFaizan UllahPas encore d'évaluation

- Nism Certification V-A (Mutual Fund) MOck TestDocument36 pagesNism Certification V-A (Mutual Fund) MOck TestAishwarya Adlakha100% (1)

- Cme Fee Schedule 2024 03 01Document11 pagesCme Fee Schedule 2024 03 01hiter67364Pas encore d'évaluation

- Ifrs Standards BrochureDocument64 pagesIfrs Standards Brochuresantosh kumarPas encore d'évaluation

- Trading Rules English Growth SheraDocument31 pagesTrading Rules English Growth SheraMann MannPas encore d'évaluation

- FIN645 Assignment (FTP) - Oct2023-Feb2024 - EPJJDocument3 pagesFIN645 Assignment (FTP) - Oct2023-Feb2024 - EPJJ2019489528Pas encore d'évaluation

- Chart Patterns & Algo. Trader PDFDocument89 pagesChart Patterns & Algo. Trader PDFsaingthy100% (1)

- Crude Oil Market Vol Report 12-02-06Document2 pagesCrude Oil Market Vol Report 12-02-06fmxconnectPas encore d'évaluation

- Cross Hedging: Nupur Gill 08D1328 Fin-2 (BBM D)Document9 pagesCross Hedging: Nupur Gill 08D1328 Fin-2 (BBM D)Priti ChowdaryPas encore d'évaluation

- Hid - Ch-2 Derivative MarketDocument40 pagesHid - Ch-2 Derivative Markethizkel hermPas encore d'évaluation

- Royalty Firms: How To Pick The Right Tool For The Right JobDocument40 pagesRoyalty Firms: How To Pick The Right Tool For The Right JobaliciaperezperezPas encore d'évaluation

- Foreign Exchange MarketDocument71 pagesForeign Exchange MarketAnonymous PDQ0wEpzMa80% (5)

- Problem 7.1 Amber Mcclain: A. B. C. Assumptions Values Values ValuesDocument25 pagesProblem 7.1 Amber Mcclain: A. B. C. Assumptions Values Values Valuesveronika100% (1)

- CH 14 PRDocument5 pagesCH 14 PRMohsinKabirPas encore d'évaluation

- Security Analysis and Portfolio Management by Rohini Singh 2018Document446 pagesSecurity Analysis and Portfolio Management by Rohini Singh 2018Aman Kumar SharanPas encore d'évaluation

- Temenos T24 Derivatives: User GuideDocument189 pagesTemenos T24 Derivatives: User GuidehuongdtPas encore d'évaluation

- Metals Hedge PDFDocument37 pagesMetals Hedge PDFMrutunjay PatraPas encore d'évaluation

- Chapter 3 - NewDocument14 pagesChapter 3 - NewNatasha GhazaliPas encore d'évaluation

- FIN 444 Mid Term Spring 2021Document6 pagesFIN 444 Mid Term Spring 2021Ahmed Kabir Akib 1631712630Pas encore d'évaluation

- Philip Maymin - Financial Hacking - Evaluate Risks, Price Derivatives, Structure Trades, and Build Your Intuition Quickly and Easily-WSPC (2012) PDFDocument222 pagesPhilip Maymin - Financial Hacking - Evaluate Risks, Price Derivatives, Structure Trades, and Build Your Intuition Quickly and Easily-WSPC (2012) PDFjc100% (1)

- Launch of MCX iCOMDEX Bullion Index FuturesDocument4 pagesLaunch of MCX iCOMDEX Bullion Index Futuresmkalidas2006Pas encore d'évaluation

- SPAN Margin System For PlatformsDocument7 pagesSPAN Margin System For Platformsprashantmehra02Pas encore d'évaluation