Vous aimerez peut-être aussi

- Charge Back Secretary Treasury TemplateDocument1 pageCharge Back Secretary Treasury TemplateNotarys To Go82% (11)

- Surety Bond TemplateDocument10 pagesSurety Bond TemplateJohn Ox95% (22)

- CreditsDocument5 pagesCreditscholericmiss100% (4)

- Tender of Payment Laws Here in Georgia, GREATDocument3 pagesTender of Payment Laws Here in Georgia, GREATDavid Jeremiah II95% (20)

- Private Bond For Set-Off, Non-Negotiable Value of Bond Is: 100 Trillion DolsDocument1 pagePrivate Bond For Set-Off, Non-Negotiable Value of Bond Is: 100 Trillion DolsKonan Snowden100% (24)

- Cash Process WebinarDocument83 pagesCash Process Webinartechcert89% (9)

- UCC IRS Form For Discharge of Estate Tax Liens f4422Document3 pagesUCC IRS Form For Discharge of Estate Tax Liens f4422Anonymous 23VuLx100% (23)

- What Is A Dollar-Conditional Acceptance-Offer To PayDocument11 pagesWhat Is A Dollar-Conditional Acceptance-Offer To Paylyocco188% (8)

- Private Surety BondDocument1 pagePrivate Surety BondHorace Ward100% (5)

- 50 State Ucc LawDocument102 pages50 State Ucc Lawpwilkers3695% (22)

- Banker S Right of Set Off - Explained - BankExamsTodayDocument4 pagesBanker S Right of Set Off - Explained - BankExamsTodayHimanshu Panchpal100% (3)

- Notarial Protest ManualDocument183 pagesNotarial Protest ManualGreg Meanwell100% (20)

- Certificate of AuthorityDocument1 pageCertificate of Authoritybob100% (15)

- Notice To Cease and Desist RedactDocument2 pagesNotice To Cease and Desist Redactmellowjohnny100% (15)

- Letter of RogatoryDocument5 pagesLetter of Rogatoryali83% (23)

- Foreclosure Remedies HandoutsDocument14 pagesForeclosure Remedies HandoutsBaqi-Khaliq Bey100% (4)

- Birth BondDocument3 pagesBirth Bondthales1980100% (11)

- Traffic Stop Practice ScriptDocument3 pagesTraffic Stop Practice ScriptHTMssm100% (25)

- Registration and TitleDocument2 pagesRegistration and TitleLukeCarter100% (8)

- Certified Fee Schedule 12-03-2012Document8 pagesCertified Fee Schedule 12-03-2012designsforliving100% (11)

- A4V EndorsementsDocument1 pageA4V Endorsementsapi-3744408100% (9)

- CUF Replacement of Surety BondDocument2 pagesCUF Replacement of Surety BondTruth Press Media100% (5)

- A Collection of Thoughts Concerning Accepted For Value (AFV) or (A4V)Document5 pagesA Collection of Thoughts Concerning Accepted For Value (AFV) or (A4V)Julian Williams©™60% (5)

- Declaration of Ownership SanitizedDocument1 pageDeclaration of Ownership Sanitizedrazcomm91% (11)

- What Is The Solution To ALL Your Problems (Update)Document75 pagesWhat Is The Solution To ALL Your Problems (Update)Michael Kovach96% (27)

- Matrix NoticeDocument1 pageMatrix Noticemellowjohnny100% (16)

- Pree-Offset Notice - ABH-122009-PON101 PDFDocument1 pagePree-Offset Notice - ABH-122009-PON101 PDFAllen-nelson of the Boisjoli family100% (8)

- Sec of State Letter Property CustodianDocument5 pagesSec of State Letter Property CustodianFAQMD285% (20)

- Tender InstructionsDocument4 pagesTender InstructionsHerbert Stout100% (73)

- Voucher Sample DC Ins#2C1BFBDocument1 pageVoucher Sample DC Ins#2C1BFBOlympus6969100% (7)

- A4V ALL ExamplesDocument8 pagesA4V ALL ExamplesTom Harkins95% (20)

- DischargeDocument1 pageDischargeAvic Perez De Leon100% (1)

- Inalienable RightsDocument7 pagesInalienable Rightsali93% (27)

- Sample Student Loan Debt Validation LetterDocument3 pagesSample Student Loan Debt Validation LetterNotarys To Go100% (12)

- The Negotiable Instruments LawDocument18 pagesThe Negotiable Instruments Lawcode4sale100% (1)

- Accessing Your Postal Treasury AccountsDocument1 pageAccessing Your Postal Treasury AccountsLiz Pasillas88% (8)

- PAYMENT BOND and Performance BondDocument3 pagesPAYMENT BOND and Performance Bondaplaw83% (6)

- Connecting The Dots Social Security To The Queen of England To The VaticanDocument5 pagesConnecting The Dots Social Security To The Queen of England To The Vaticandesignsforliving83% (6)

- Basic Accounting For Credit and Savings SchemesDocument103 pagesBasic Accounting For Credit and Savings SchemesOxfam100% (1)

- Surety Bond IiDocument2 pagesSurety Bond IiStephen Monaghan100% (24)

- F.R.B. Manuals and Forms - PDFDocument2 pagesF.R.B. Manuals and Forms - PDFBranden Hall89% (9)

- Sample Discharge of Mortgage To LendersDocument2 pagesSample Discharge of Mortgage To LendersZIONCREDITGROUP100% (12)

- LETTER ROGATORY-Bankrupcy CourtDocument1 pageLETTER ROGATORY-Bankrupcy Courtrazcomm100% (6)

- US Internal Revenue Service: I1040 - 1995Document84 pagesUS Internal Revenue Service: I1040 - 1995IRS67% (3)

- Charge Back Letter No. 1 SAMPLEDocument1 pageCharge Back Letter No. 1 SAMPLEJames Thomas100% (1)

- Supercedes Bond To Pay Our DebtsDocument2 pagesSupercedes Bond To Pay Our DebtsFreeman Lawyer100% (7)

- Notice of Default Discharge of Obligation Demand For Re Conveyance To Donna Carpenter For First American Title Inter Lac Hen LNDocument4 pagesNotice of Default Discharge of Obligation Demand For Re Conveyance To Donna Carpenter For First American Title Inter Lac Hen LNPieter Panne100% (5)

- How To Make A Bill Into A Money OrderDocument1 pageHow To Make A Bill Into A Money OrderJohn Wallace40% (5)

- I Am One Stupid American-RDDocument6 pagesI Am One Stupid American-RDjvonmeier92% (13)

- Instructions For Discharging Public Debt With Private ChecksDocument4 pagesInstructions For Discharging Public Debt With Private Checkssspikes93% (168)

- Negotiable Instruments Laws Carlos Hilado Memorial State University Submitted By: Atty. Jul Davi P. SaezDocument26 pagesNegotiable Instruments Laws Carlos Hilado Memorial State University Submitted By: Atty. Jul Davi P. SaezJellie ElmerPas encore d'évaluation

- NIL WK 1 2Document123 pagesNIL WK 1 2Jeanette Formentera100% (1)

- Law of Negotiable Instrument (Law 416)Document8 pagesLaw of Negotiable Instrument (Law 416)Sarah M'dinPas encore d'évaluation

- Group 5 Final Written Report-Legal FormsDocument34 pagesGroup 5 Final Written Report-Legal FormsFederico Dipay Jr.Pas encore d'évaluation

- 5552 Negotiable Instrument ActDocument28 pages5552 Negotiable Instrument Actbrollsports250Pas encore d'évaluation

- Business Law Question N AnswersDocument24 pagesBusiness Law Question N AnswersMohanarajPas encore d'évaluation

- Negotiable Inctruments LawDocument15 pagesNegotiable Inctruments LawAr Di SagamlaPas encore d'évaluation

- Remedial Law Review 1 (Civil Procedure Only) - Doctrines of Cases - Atty. BrondialDocument34 pagesRemedial Law Review 1 (Civil Procedure Only) - Doctrines of Cases - Atty. BrondialGemma F. Tiama100% (1)

- Remedial Law Review 1 (Civil Procedure Only) - Doctrines of Cases - Atty. BrondialDocument34 pagesRemedial Law Review 1 (Civil Procedure Only) - Doctrines of Cases - Atty. BrondialGemma F. Tiama100% (1)

- LegForms Group 4Document25 pagesLegForms Group 4SmurfPas encore d'évaluation

- Insurance CasesDocument35 pagesInsurance CasesSmurfPas encore d'évaluation

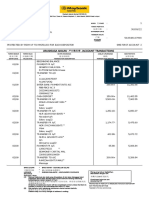

- Mashreq Credit Card Statement Oct - Nov 2021Document4 pagesMashreq Credit Card Statement Oct - Nov 2021bAYASUPas encore d'évaluation

- CTA Case EB For ReferenceDocument29 pagesCTA Case EB For Referencepatricia_arpilledaPas encore d'évaluation

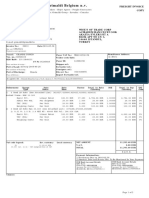

- Grimaldi Belgium N.V.: Freight InvoiceDocument2 pagesGrimaldi Belgium N.V.: Freight InvoiceAyseColakPas encore d'évaluation

- Kotak InsuraceDocument1 pageKotak InsuraceRemo RomeoPas encore d'évaluation

- Form XVIIDocument32 pagesForm XVIIUmesh CPas encore d'évaluation

- Tarif Customs Clearance Di SurabayaDocument2 pagesTarif Customs Clearance Di SurabayaAlvinBurhaniPas encore d'évaluation

- LOIDocument1 pageLOIValencia Mazariegos Pablo Roberto100% (1)

- Illustration For Your HDFC Life Click 2 Protect PlusDocument2 pagesIllustration For Your HDFC Life Click 2 Protect Plusbommakanti.shivaPas encore d'évaluation

- Payslip For September 2019 - LIANGCHOW (Closed Payroll) : Uniteam Marine LimitedDocument1 pagePayslip For September 2019 - LIANGCHOW (Closed Payroll) : Uniteam Marine LimitedThet NaingPas encore d'évaluation

- Double Entry Book KeepingDocument20 pagesDouble Entry Book KeepingLynda Davis100% (4)

- Penyata Akaun: Tarikh Date Keterangan Description Terminal ID ID Terminal Amaun (RM) Amount (RM) Baki (RM) Balance (RM)Document3 pagesPenyata Akaun: Tarikh Date Keterangan Description Terminal ID ID Terminal Amaun (RM) Amount (RM) Baki (RM) Balance (RM)Fida AwangPas encore d'évaluation

- Northsouth: Estados UnidosDocument1 pageNorthsouth: Estados UnidosRodri DuartePas encore d'évaluation

- XXXXXXXXXX6781 - 20230615160830874376 (1) - UnlockedDocument16 pagesXXXXXXXXXX6781 - 20230615160830874376 (1) - UnlockedRajendra SharmaPas encore d'évaluation

- 13 Accounting Cycle of A Service Business 2Document28 pages13 Accounting Cycle of A Service Business 2Ashley Judd Mallonga Beran60% (5)

- TB - Ch05-Short Term Decisions and Accounting InformationsDocument14 pagesTB - Ch05-Short Term Decisions and Accounting InformationsJc GappiPas encore d'évaluation

- Payment Confirmation Receipt: No: 88/DCE/05/2021Document2 pagesPayment Confirmation Receipt: No: 88/DCE/05/2021Dinda Cinta NainggolanPas encore d'évaluation

- IQJxjk EFTy Ua 5 G KTDocument8 pagesIQJxjk EFTy Ua 5 G KTAbhishek KeshariPas encore d'évaluation

- Supply Chain ManagementDocument59 pagesSupply Chain ManagementNyeko FrancisPas encore d'évaluation

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document3 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961digi timePas encore d'évaluation

- MBBcurrent 564548147990 2022-09-30 PDFDocument12 pagesMBBcurrent 564548147990 2022-09-30 PDFAdeela fazlinPas encore d'évaluation

- Planning Designing and Analysis of Bus Stand With Special FeaturesDocument21 pagesPlanning Designing and Analysis of Bus Stand With Special FeaturesThamilarasanPas encore d'évaluation

- JNTU (K) LSCM 4th Sem 2017 Question PaperDocument1 pageJNTU (K) LSCM 4th Sem 2017 Question Paperujjal dasPas encore d'évaluation

- Premium Paid CertificateDocument1 pagePremium Paid Certificatemsurendra642Pas encore d'évaluation

- Money and Banking Class 12 ProjectDocument2 pagesMoney and Banking Class 12 ProjectRocking Rahul55% (11)

- Summary:: Employment Summary: Employer Role DurationsDocument2 pagesSummary:: Employment Summary: Employer Role DurationsNaseer SapPas encore d'évaluation

- Conveyance Format November MonthDocument10 pagesConveyance Format November MonthVimal SinghPas encore d'évaluation

- 6927022343Document1 page6927022343JohnPas encore d'évaluation

- Equity Program FAQDocument14 pagesEquity Program FAQNikhil SinghalPas encore d'évaluation

- Tax Cases Table of ContentsDocument7 pagesTax Cases Table of ContentsKaren Sheila B. Mangusan - DegayPas encore d'évaluation

- Business Bank Statement Wells FargoDocument6 pagesBusiness Bank Statement Wells FargoJoe SF100% (1)

- Finance Basics (HBR 20-Minute Manager Series)D'EverandFinance Basics (HBR 20-Minute Manager Series)Évaluation : 4.5 sur 5 étoiles4.5/5 (32)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaD'EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (14)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingD'EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingÉvaluation : 4.5 sur 5 étoiles4.5/5 (17)

- Value: The Four Cornerstones of Corporate FinanceD'EverandValue: The Four Cornerstones of Corporate FinanceÉvaluation : 4.5 sur 5 étoiles4.5/5 (18)

- The Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetD'EverandThe Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetÉvaluation : 5 sur 5 étoiles5/5 (2)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successD'EverandReady, Set, Growth hack:: A beginners guide to growth hacking successÉvaluation : 4.5 sur 5 étoiles4.5/5 (93)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistD'EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistÉvaluation : 4.5 sur 5 étoiles4.5/5 (73)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisD'EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisÉvaluation : 5 sur 5 étoiles5/5 (6)

- Joy of Agility: How to Solve Problems and Succeed SoonerD'EverandJoy of Agility: How to Solve Problems and Succeed SoonerÉvaluation : 4 sur 5 étoiles4/5 (1)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelD'Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelPas encore d'évaluation

- Financial Risk Management: A Simple IntroductionD'EverandFinancial Risk Management: A Simple IntroductionÉvaluation : 4.5 sur 5 étoiles4.5/5 (7)

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityD'EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityÉvaluation : 4.5 sur 5 étoiles4.5/5 (4)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursD'EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursÉvaluation : 4.5 sur 5 étoiles4.5/5 (8)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialD'EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialÉvaluation : 4.5 sur 5 étoiles4.5/5 (32)

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)D'EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Évaluation : 4.5 sur 5 étoiles4.5/5 (4)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsD'EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsPas encore d'évaluation

- How to Measure Anything: Finding the Value of Intangibles in BusinessD'EverandHow to Measure Anything: Finding the Value of Intangibles in BusinessÉvaluation : 3.5 sur 5 étoiles3.5/5 (4)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanD'EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanÉvaluation : 4.5 sur 5 étoiles4.5/5 (79)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSND'Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNÉvaluation : 4.5 sur 5 étoiles4.5/5 (3)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialD'EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialPas encore d'évaluation

- The Synergy Solution: How Companies Win the Mergers and Acquisitions GameD'EverandThe Synergy Solution: How Companies Win the Mergers and Acquisitions GamePas encore d'évaluation

- Creating Shareholder Value: A Guide For Managers And InvestorsD'EverandCreating Shareholder Value: A Guide For Managers And InvestorsÉvaluation : 4.5 sur 5 étoiles4.5/5 (8)

- Value: The Four Cornerstones of Corporate FinanceD'EverandValue: The Four Cornerstones of Corporate FinanceÉvaluation : 5 sur 5 étoiles5/5 (2)