Vous aimerez peut-être aussi

- Financial Reporting - First Term Exams (Fall 2018)Document7 pagesFinancial Reporting - First Term Exams (Fall 2018)Aqsa AftabPas encore d'évaluation

- 1 Accounting-Week-2assignmentsDocument4 pages1 Accounting-Week-2assignmentsTim Thiru0% (1)

- Chapter 12 Solutions ManualDocument82 pagesChapter 12 Solutions ManualbearfoodPas encore d'évaluation

- Ch-5 Solution ManualDocument15 pagesCh-5 Solution ManualCyn SyjucoPas encore d'évaluation

- Time Value of Money General Instructions:: Activity 4 MfcapistranoDocument2 pagesTime Value of Money General Instructions:: Activity 4 MfcapistranoAstrid BuenacosaPas encore d'évaluation

- Problems On Pricing DecisionsDocument15 pagesProblems On Pricing DecisionsMae-shane SagayoPas encore d'évaluation

- Test Bank For Financial Reporting Financial Statement Analysis and Valuation A Strategic Perspective 7th Edition Wahlen, Baginski, BradshawDocument33 pagesTest Bank For Financial Reporting Financial Statement Analysis and Valuation A Strategic Perspective 7th Edition Wahlen, Baginski, Bradshawa415878694Pas encore d'évaluation

- CH 07Document33 pagesCH 07Nguyen Thanh Tung (K15 HL)Pas encore d'évaluation

- Tutorial 7Document18 pagesTutorial 7chun0100% (1)

- 03B) Chapter 3 Questions - BrighamDocument7 pages03B) Chapter 3 Questions - BrighamMohammad Ather100% (1)

- Apex Spinning Annual Report-2016-17Document50 pagesApex Spinning Annual Report-2016-17SayeedMdAzaharulIslamPas encore d'évaluation

- Aafr Ifrs 15 Icap Past Papers With SolutionDocument10 pagesAafr Ifrs 15 Icap Past Papers With SolutionAqib Sheikh0% (1)

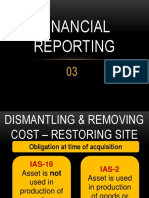

- Question-Ias 2 - Ias 16 and Ias 40 - Admin-2019-2020-1Document6 pagesQuestion-Ias 2 - Ias 16 and Ias 40 - Admin-2019-2020-1Letsah BrightPas encore d'évaluation

- UntitledDocument17 pagesUntitledEhab M. Abdel HadyPas encore d'évaluation

- Finance Chapter No 2Document20 pagesFinance Chapter No 2UzairPas encore d'évaluation

- Foundations of Financial Management Canadian 11th Edition Block Solutions ManualDocument6 pagesFoundations of Financial Management Canadian 11th Edition Block Solutions ManualEricYoderptkaoPas encore d'évaluation

- Devamsha's Big 4 Competency Bible: Final InterviewDocument33 pagesDevamsha's Big 4 Competency Bible: Final InterviewsadasdPas encore d'évaluation

- Cost and Management Accounting: Paper 7Document31 pagesCost and Management Accounting: Paper 7Atukwatse PamelaPas encore d'évaluation

- Practice Exercises 2Document3 pagesPractice Exercises 2Richard RobinsonPas encore d'évaluation

- FA - PartnershipDocument109 pagesFA - PartnershipRafay RashidPas encore d'évaluation

- Cash BudgetDocument2 pagesCash BudgetSenthil Kumar0% (1)

- Financial Derivatives Question and SolutionDocument2 pagesFinancial Derivatives Question and SolutionNithya NairPas encore d'évaluation

- CHP 23Document19 pagesCHP 23lena cpaPas encore d'évaluation

- BUDGETING - Exercises: UnitsDocument2 pagesBUDGETING - Exercises: UnitsLeo Sandy Ambe CuisPas encore d'évaluation

- Mas 1405Document12 pagesMas 1405Alvin AgullanaPas encore d'évaluation

- Techniques of Capital Budgeting SumsDocument15 pagesTechniques of Capital Budgeting Sumshardika jadavPas encore d'évaluation

- CH 4Document6 pagesCH 4Jean ValderramaPas encore d'évaluation

- Valuation Method - Risk and Rate ReturnsDocument6 pagesValuation Method - Risk and Rate ReturnsGlendy PasantingPas encore d'évaluation

- Advanced Taxation Novmock2019 PDFDocument13 pagesAdvanced Taxation Novmock2019 PDFAndy AsantePas encore d'évaluation

- Chapter 8 Interest Risk IDocument46 pagesChapter 8 Interest Risk ISabrina Karim0% (1)

- SMG - 3 - Modeling and Solving LP Problems in A SpreadsheetDocument43 pagesSMG - 3 - Modeling and Solving LP Problems in A SpreadsheetTestPas encore d'évaluation

- Aafr Ifrs 16 Icap Past Papers With SolutionDocument8 pagesAafr Ifrs 16 Icap Past Papers With SolutionAqib SheikhPas encore d'évaluation

- IAS-33 Earning Per ShareDocument10 pagesIAS-33 Earning Per ShareButt Arham100% (1)

- PV Problem Set With AnswersDocument2 pagesPV Problem Set With AnswersArun S BharadwajPas encore d'évaluation

- Accounitng Answers Mid Term QuizDocument9 pagesAccounitng Answers Mid Term QuizWarda Tariq0% (1)

- CH 14Document31 pagesCH 14Bui Thi Thu Hang (K13HN)Pas encore d'évaluation

- Else VierDocument22 pagesElse VierNakambull Hilma100% (1)

- Chapter 16 Budgeting Capital Expenditures Research and Development Expenditures and Cash Pert Cost The Flexible BudgetDocument17 pagesChapter 16 Budgeting Capital Expenditures Research and Development Expenditures and Cash Pert Cost The Flexible BudgetZunaira ButtPas encore d'évaluation

- Incremental AnalysisDocument18 pagesIncremental AnalysisMary Joy BalangcadPas encore d'évaluation

- Assignment No. 1 - If Extra Practice ProblemDocument4 pagesAssignment No. 1 - If Extra Practice ProblemTejas Joshi100% (1)

- Gul Ahmed-Phase 3Document3 pagesGul Ahmed-Phase 3Hashim Ayaz KhanPas encore d'évaluation

- PFM CHAP 22 All SolutionsDocument22 pagesPFM CHAP 22 All Solutionsjanay martin100% (1)

- Foundations of Financial Management Homework Solutions Chapter 1,2,3Document6 pagesFoundations of Financial Management Homework Solutions Chapter 1,2,3nreid27010% (3)

- Chapter 14-Ch. 14-Cash Flow Estimation 11-13.El-Bigbee Bottling CompanyDocument1 pageChapter 14-Ch. 14-Cash Flow Estimation 11-13.El-Bigbee Bottling CompanyRajib DahalPas encore d'évaluation

- FNCE 627 Week 7 Case Study 1 Financial PlanningDocument2 pagesFNCE 627 Week 7 Case Study 1 Financial Planningalka murarka0% (1)

- Taranveer-Wk 1-Quiz 1-Man EcoDocument16 pagesTaranveer-Wk 1-Quiz 1-Man EcoaksPas encore d'évaluation

- Apex Spinning and Knitting Mills LTD: Financial AnalysisDocument29 pagesApex Spinning and Knitting Mills LTD: Financial AnalysisNakibul HoqPas encore d'évaluation

- Balance Sheet Presentation of Liabilities: Problem 10.2ADocument4 pagesBalance Sheet Presentation of Liabilities: Problem 10.2AMuhammad Haris100% (1)

- QN1. Consolidated FS-HeverDocument6 pagesQN1. Consolidated FS-HeverSandeep Gyawali100% (1)

- Manajemen KeuanganDocument5 pagesManajemen KeuanganazmastecPas encore d'évaluation

- Lahore School of Economics Financial Management II Assignment 6 Financial Planning & Forecasting - 1Document1 pageLahore School of Economics Financial Management II Assignment 6 Financial Planning & Forecasting - 1AhmedPas encore d'évaluation

- Distribution Network Models and Case StudyDocument9 pagesDistribution Network Models and Case Studyyellow fishPas encore d'évaluation

- Multiple Choice Questions: Financial Statements and AnalysisDocument29 pagesMultiple Choice Questions: Financial Statements and AnalysisHarvey PeraltaPas encore d'évaluation

- Chapter 11 QuestionsDocument5 pagesChapter 11 QuestionsZic ZacPas encore d'évaluation

- Finman Midterms Part 1Document7 pagesFinman Midterms Part 1JerichoPas encore d'évaluation

- Optimization Techniques and New Management ToolsDocument21 pagesOptimization Techniques and New Management ToolsSaurabh SharmaPas encore d'évaluation

- PDF Solution To Assignment 2 Corrected - CompressDocument4 pagesPDF Solution To Assignment 2 Corrected - CompressAsim MunirPas encore d'évaluation

- RAPHAEL RANDY 20220211161750 ACCT6133003 LH11 FIN ConfDocument8 pagesRAPHAEL RANDY 20220211161750 ACCT6133003 LH11 FIN ConfAnggur CapOTPas encore d'évaluation

- Contingent LiabilityDocument4 pagesContingent LiabilityProspero Jerome IntanoPas encore d'évaluation

- Lobrigas Unit5 Topic1 AssessmentDocument3 pagesLobrigas Unit5 Topic1 AssessmentClaudine LobrigasPas encore d'évaluation

- FR - 03 PDFDocument31 pagesFR - 03 PDFalrightaphroditePas encore d'évaluation

- BrochureKSE30 IdxDocument21 pagesBrochureKSE30 IdxSobhia KamalPas encore d'évaluation

- FR - 11Document47 pagesFR - 11Sobhia KamalPas encore d'évaluation

- FR - 04Document28 pagesFR - 04Sobhia KamalPas encore d'évaluation

- DerivativesDocument1 pageDerivativesRandy ManzanoPas encore d'évaluation

- Chapter 7 - : Valuation and Characteristics of BondsDocument54 pagesChapter 7 - : Valuation and Characteristics of BondsAndre SantosoPas encore d'évaluation

- Careers in Banking & Finance 2010-2011Document79 pagesCareers in Banking & Finance 2010-2011roger654Pas encore d'évaluation

- Reinsurance BiDocument16 pagesReinsurance Biperkin kothariPas encore d'évaluation

- The Long Term by Howard S. KatzDocument4 pagesThe Long Term by Howard S. Katzapi-22433340Pas encore d'évaluation

- Micro-Cap Review Magazine Fall 2010Document80 pagesMicro-Cap Review Magazine Fall 2010Planet MicroCap Review MagazinePas encore d'évaluation

- Excel DataDocument2 098 pagesExcel Dataquangautruc95Pas encore d'évaluation

- Security Trading, Settlement and RegulationsDocument24 pagesSecurity Trading, Settlement and RegulationsAmarinder SinghPas encore d'évaluation

- Accounting in IBDocument23 pagesAccounting in IBAbdur RajakPas encore d'évaluation

- Penilaian Saham: Ari Fahimatussyam PN, S.E., M.AkDocument23 pagesPenilaian Saham: Ari Fahimatussyam PN, S.E., M.AkAynie AyniePas encore d'évaluation

- Final Project On Religare SecuritiesDocument49 pagesFinal Project On Religare SecuritiesShivam MisraPas encore d'évaluation

- Problem 11.3Document1 pageProblem 11.3SamerPas encore d'évaluation

- An Introduction To Derivative Securities, Financial Markets, and Risk ManagementDocument66 pagesAn Introduction To Derivative Securities, Financial Markets, and Risk ManagementMuhammad AliPas encore d'évaluation

- Fibonacci Ratios & Harmonic PatternsDocument10 pagesFibonacci Ratios & Harmonic Patternsgunawan kertosonoPas encore d'évaluation

- 0450/11 Business Studies: Cambridge International ExaminationsDocument12 pages0450/11 Business Studies: Cambridge International ExaminationsRebecca SteatonPas encore d'évaluation

- SMC ProjectDocument34 pagesSMC Projectpiyush solankiPas encore d'évaluation

- ET Wealth Apr 6 - 12 2020Document23 pagesET Wealth Apr 6 - 12 2020Rony GeorgePas encore d'évaluation

- Test - 1 General Studies: Paper - IDocument46 pagesTest - 1 General Studies: Paper - IThe Indian ExpressPas encore d'évaluation

- HomeworkDocument8 pagesHomeworkEnrique Feliciano Cornejo50% (2)

- The Theory of Corporate Finance by Jean Tirole Chapter 1 Notes - Corporate GovernanceDocument10 pagesThe Theory of Corporate Finance by Jean Tirole Chapter 1 Notes - Corporate GovernanceRupesh Sharma100% (1)

- My MM TradingNotesDocument5 pagesMy MM TradingNotesnyagweyaPas encore d'évaluation

- International BusinessDocument4 pagesInternational BusinessAnton TaminPas encore d'évaluation

- Comparing InvestmentsDocument59 pagesComparing InvestmentsKondeti Harsha VardhanPas encore d'évaluation

- Chart Pattern Cheat Sheet-1Document18 pagesChart Pattern Cheat Sheet-1YASHANK VISHWAKARMAPas encore d'évaluation

- Pelaburan Emas - Gold InvestmentDocument18 pagesPelaburan Emas - Gold InvestmentcreativemozakPas encore d'évaluation

- SLVR White Paper FinalDocument16 pagesSLVR White Paper FinalTorVikPas encore d'évaluation

- 01+IJEFI 13752 Enow Okey 20221219 V1Document6 pages01+IJEFI 13752 Enow Okey 20221219 V1o cindy glaudiaPas encore d'évaluation

- EFCh 01 PPEd 2Document28 pagesEFCh 01 PPEd 2Naheed AkhtarPas encore d'évaluation

- Tech Mahindra: Financial Analysis To Determine Investment Decision by Group C10Document9 pagesTech Mahindra: Financial Analysis To Determine Investment Decision by Group C10Sucharita SahaPas encore d'évaluation

- VCM - Chapter 1Document11 pagesVCM - Chapter 1belle crisPas encore d'évaluation