Vous aimerez peut-être aussi

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- ACC301 Auditing NotesDocument19 pagesACC301 Auditing NotesShakeel AhmedPas encore d'évaluation

- Strategic Competitive Analysis Questionnaire 1Document2 pagesStrategic Competitive Analysis Questionnaire 1Ajay BadhayaPas encore d'évaluation

- Page - 1Document49 pagesPage - 1Ankur GadhyanPas encore d'évaluation

- B - ChipsDocument27 pagesB - Chipsshahreen arshadPas encore d'évaluation

- Money Making Secrets of Marketing Genius Jay Abraham and Other Marketing WizardsDocument397 pagesMoney Making Secrets of Marketing Genius Jay Abraham and Other Marketing Wizardsjazminne huang100% (2)

- Philippine Public Sector Accounting Standard 1Document18 pagesPhilippine Public Sector Accounting Standard 1Anonymous bEDr3JhGPas encore d'évaluation

- Understanding The Entity and Its Environment Including Its Internal Control and Assessing The Risks of Material MisstatementDocument35 pagesUnderstanding The Entity and Its Environment Including Its Internal Control and Assessing The Risks of Material MisstatementKathleenPas encore d'évaluation

- Audit Program Inventory ObjectivesDocument2 pagesAudit Program Inventory Objectivesnicole bancoroPas encore d'évaluation

- Om-Chapter 4Document16 pagesOm-Chapter 4wubePas encore d'évaluation

- Castilloraph 2Document4 pagesCastilloraph 2Raphaela CastilloPas encore d'évaluation

- Working Capital ReviewerDocument4 pagesWorking Capital Reviewerjennyxrous26Pas encore d'évaluation

- Chap 06 Inventory Control ModelsDocument112 pagesChap 06 Inventory Control ModelsFatma El TayebPas encore d'évaluation

- Financial Analysis and Planning: Cash Flow and Fund Flow Statement Are Not There in SyllabusDocument29 pagesFinancial Analysis and Planning: Cash Flow and Fund Flow Statement Are Not There in SyllabusHanabusa Kawaii IdouPas encore d'évaluation

- EOQ QuizDocument3 pagesEOQ QuizTesslene Claire SantosPas encore d'évaluation

- Chapter 4 EappDocument10 pagesChapter 4 EappErika DomingoPas encore d'évaluation

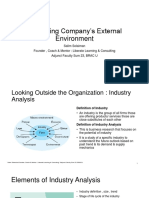

- Ses 3 - Evaluating Company's External EnvironmentDocument21 pagesSes 3 - Evaluating Company's External EnvironmentKazi Ayman AlamPas encore d'évaluation

- SOLUTIONS - Mother GooseDocument2 pagesSOLUTIONS - Mother GooseVivian Loraine BorresPas encore d'évaluation

- Business Marketing Text and Cases 4nbsped 125909796x 9781259097966Document627 pagesBusiness Marketing Text and Cases 4nbsped 125909796x 9781259097966Nguyễn Khánh ChiPas encore d'évaluation

- A Customer Experience Reboot: Pivoting Toward The Automotive Industry's Future SuccessDocument31 pagesA Customer Experience Reboot: Pivoting Toward The Automotive Industry's Future SuccessAtul RaghuvanshiPas encore d'évaluation

- Sample Notice of 1st Annual General MeetingDocument14 pagesSample Notice of 1st Annual General MeetingSudhanshu JhaPas encore d'évaluation

- Final Project PDFDocument79 pagesFinal Project PDFdinesh kumar0% (1)

- PVR Cinemas Marketing StrategyDocument65 pagesPVR Cinemas Marketing Strategyaliwasim100% (1)

- Distribution Strategies For El Fragrancia: Submitted byDocument9 pagesDistribution Strategies For El Fragrancia: Submitted bySoumadeep GuharayPas encore d'évaluation

- Case Analysis: Digital Age GamesDocument1 pageCase Analysis: Digital Age GamesJanine NicolePas encore d'évaluation

- Massa Tucci and Afuah AMA 2017 - Plus APPENDIXDocument58 pagesMassa Tucci and Afuah AMA 2017 - Plus APPENDIXTaonaishe NcubePas encore d'évaluation

- B2B SaaS Metrics Benchmark 2023 REPORTDocument51 pagesB2B SaaS Metrics Benchmark 2023 REPORTstartupcommunity.top100% (1)

- Cadbury Questionnaire - Google FormsDocument6 pagesCadbury Questionnaire - Google FormsPooja bhuvanaPas encore d'évaluation

- 61oq678rf - CD - Chapter 10 - Acctg Cycle of A Merchandising BusinessDocument17 pages61oq678rf - CD - Chapter 10 - Acctg Cycle of A Merchandising BusinessLyra Mae De BotonPas encore d'évaluation

- " Master Blaster On Fundamental of Accounts ": AcknowledgementDocument516 pages" Master Blaster On Fundamental of Accounts ": AcknowledgementPushpinder KumarPas encore d'évaluation