Vous aimerez peut-être aussi

- Global FX StrategyDocument4 pagesGlobal FX StrategyllaryPas encore d'évaluation

- Global FX StrategyDocument3 pagesGlobal FX StrategyrockieballPas encore d'évaluation

- BNP FX WeeklyDocument22 pagesBNP FX WeeklyPhillip HsiaPas encore d'évaluation

- Daily FX Update: Eur Limited by Fibo LevelsDocument3 pagesDaily FX Update: Eur Limited by Fibo LevelsBasil Baby-PisharathuPas encore d'évaluation

- Shadow Capitalism: Market Commentary by Naufal SanaullahDocument6 pagesShadow Capitalism: Market Commentary by Naufal SanaullahNaufal SanaullahPas encore d'évaluation

- ScotiaBank AUG 04 Daily FX UpdateDocument3 pagesScotiaBank AUG 04 Daily FX UpdateMiir ViirPas encore d'évaluation

- ScotiaBank AUG 06 Daily FX UpdateDocument3 pagesScotiaBank AUG 06 Daily FX UpdateMiir ViirPas encore d'évaluation

- EUR poised to recover, DXY pullback | Trading plans Jan 2023Document14 pagesEUR poised to recover, DXY pullback | Trading plans Jan 2023Hồng NgọcPas encore d'évaluation

- Global FX Insights - 25 July 2016Document12 pagesGlobal FX Insights - 25 July 2016alvarocantarioPas encore d'évaluation

- Global FX Insights - 8 August 2016Document12 pagesGlobal FX Insights - 8 August 2016BBand TraderPas encore d'évaluation

- Shadow Capitalism: Market Commentary by Naufal SanaullahDocument7 pagesShadow Capitalism: Market Commentary by Naufal SanaullahNaufal SanaullahPas encore d'évaluation

- Ranges (Up Till 12.12pm HKT) : Currency CurrencyDocument3 pagesRanges (Up Till 12.12pm HKT) : Currency Currencyapi-290371470Pas encore d'évaluation

- ING Think FX Daily Patient Rba Remains A Secondary Driver For AudDocument4 pagesING Think FX Daily Patient Rba Remains A Secondary Driver For AudzushiiiPas encore d'évaluation

- Top Trading Opportunities FOR 2020: Dailyfx Research TeamDocument35 pagesTop Trading Opportunities FOR 2020: Dailyfx Research Teammytemp_01Pas encore d'évaluation

- Sep 16Document12 pagesSep 16kn0qPas encore d'évaluation

- Top Trading Opportunities 2017Document35 pagesTop Trading Opportunities 2017Max KennedyPas encore d'évaluation

- 2008 DB Fixed Income Outlook (12!14!07)Document107 pages2008 DB Fixed Income Outlook (12!14!07)STPas encore d'évaluation

- Top Trading OpportunitiesDocument25 pagesTop Trading Opportunitiestanyan.huangPas encore d'évaluation

- Weekly Report Dec 9th 14thDocument2 pagesWeekly Report Dec 9th 14thFEPFinanceClubPas encore d'évaluation

- Daily-i-Forex-report-1 by EPIC RESEARCH 27 MAY 2013Document15 pagesDaily-i-Forex-report-1 by EPIC RESEARCH 27 MAY 2013EpicresearchPas encore d'évaluation

- 2011 12 06 Migbank Daily Technical Analysis ReportDocument15 pages2011 12 06 Migbank Daily Technical Analysis ReportmigbankPas encore d'évaluation

- Daily FX Update: Europe Provides Offset To Worrisome China PmiDocument3 pagesDaily FX Update: Europe Provides Offset To Worrisome China PmiMohd Sofian YusoffPas encore d'évaluation

- FX Themes and Trades Outlook for 2019Document15 pagesFX Themes and Trades Outlook for 2019JustinC.PaoliniPas encore d'évaluation

- BNP Steer ExplanationDocument31 pagesBNP Steer ExplanationCynthia SerraoPas encore d'évaluation

- Research Report 20 Dec 2023Document21 pagesResearch Report 20 Dec 2023tanmaymaltarPas encore d'évaluation

- 2011 12 02 Migbank Daily Technical Analysis ReportDocument15 pages2011 12 02 Migbank Daily Technical Analysis ReportmigbankPas encore d'évaluation

- Barclays FX Weekly Brief 20100902Document18 pagesBarclays FX Weekly Brief 20100902aaronandmosesllcPas encore d'évaluation

- ScotiaBank AUG 03 Daily FX UpdateDocument3 pagesScotiaBank AUG 03 Daily FX UpdateMiir ViirPas encore d'évaluation

- Currency Daily Report September 24Document4 pagesCurrency Daily Report September 24Angel BrokingPas encore d'évaluation

- FX TacticalsDocument6 pagesFX TacticalsodinPas encore d'évaluation

- Jun-10-DJ Asia Daily Forex OutlookDocument3 pagesJun-10-DJ Asia Daily Forex OutlookMiir ViirPas encore d'évaluation

- Ranges (Up Till 11.50am HKT) : Currency CurrencyDocument3 pagesRanges (Up Till 11.50am HKT) : Currency Currencyapi-290371470Pas encore d'évaluation

- FX Compass: Looking For Signs of Pushback: Focus: Revising GBP Forecasts HigherDocument25 pagesFX Compass: Looking For Signs of Pushback: Focus: Revising GBP Forecasts HighertekesburPas encore d'évaluation

- FX Strategy: Summer Dull With EUR/USD Rangebound But Upside BiasDocument9 pagesFX Strategy: Summer Dull With EUR/USD Rangebound But Upside Biasjesus davidPas encore d'évaluation

- Daily FX Update: Cad Outperforming Into Na OpenDocument3 pagesDaily FX Update: Cad Outperforming Into Na OpenbabbabeuPas encore d'évaluation

- Shadow Capitalism: Market Commentary by Naufal SanaullahDocument6 pagesShadow Capitalism: Market Commentary by Naufal SanaullahNaufal SanaullahPas encore d'évaluation

- NMFMS - Daily Market Analysis - 10th Jan (Wed)Document14 pagesNMFMS - Daily Market Analysis - 10th Jan (Wed)williamrmahasoaPas encore d'évaluation

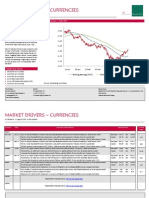

- Market Drivers - Currencies: Today's Comment Today's Chart - EUR/USDDocument5 pagesMarket Drivers - Currencies: Today's Comment Today's Chart - EUR/USDMiir ViirPas encore d'évaluation

- Global FX StrategyDocument3 pagesGlobal FX Strategyashish pandeyPas encore d'évaluation

- FX Daily: High Bar To Reverse The Dollar Bear TrendDocument3 pagesFX Daily: High Bar To Reverse The Dollar Bear Trenddbr trackdPas encore d'évaluation

- Aug-05-Dj Asia Daily Forex OutlookDocument4 pagesAug-05-Dj Asia Daily Forex OutlookMiir ViirPas encore d'évaluation

- HSBC - Currency Outlook DecemberDocument46 pagesHSBC - Currency Outlook Decembermgroble3Pas encore d'évaluation

- ScotiaBank JUL 27 Daily FX UpdateDocument3 pagesScotiaBank JUL 27 Daily FX UpdateMiir ViirPas encore d'évaluation

- Ranges (Up Till 11.25am HKT) : Currency CurrencyDocument3 pagesRanges (Up Till 11.25am HKT) : Currency Currencyapi-290371470Pas encore d'évaluation

- Morning Call - June 7 2010Document7 pagesMorning Call - June 7 2010chibondkingPas encore d'évaluation

- MF Global Daily Report Summary and USDINR OutlookDocument5 pagesMF Global Daily Report Summary and USDINR OutlookTarique kamaalPas encore d'évaluation

- 11/14/14 Global-Macro Trading SimulationDocument17 pages11/14/14 Global-Macro Trading SimulationPaul KimPas encore d'évaluation

- RBC Fixed Income & Currency Strategy Aug 18Document3 pagesRBC Fixed Income & Currency Strategy Aug 18derailedcapitalism.comPas encore d'évaluation

- 2011 12 09 Migbank Daily Technical Analysis ReportDocument15 pages2011 12 09 Migbank Daily Technical Analysis ReportmigbankPas encore d'évaluation

- ScotiaBank AUG 09 Daily FX UpdateDocument3 pagesScotiaBank AUG 09 Daily FX UpdateMiir ViirPas encore d'évaluation

- G10 FX Week Ahead: Tailgating Treasury YieldsDocument8 pagesG10 FX Week Ahead: Tailgating Treasury YieldsrockieballPas encore d'évaluation

- FX Insight eDocument16 pagesFX Insight ePopeye AlexPas encore d'évaluation

- FX Weekly Commentary - Nov 06 - Nov 12 2011Document5 pagesFX Weekly Commentary - Nov 06 - Nov 12 2011James PutraPas encore d'évaluation

- Daily Currency Briefing: Agreement But No Happy EndDocument4 pagesDaily Currency Briefing: Agreement But No Happy EndtimurrsPas encore d'évaluation

- 11/11/14 Global-Macro Trading SimulationDocument20 pages11/11/14 Global-Macro Trading SimulationPaul KimPas encore d'évaluation

- Morning Call July 7 2010Document4 pagesMorning Call July 7 2010chibondkingPas encore d'évaluation

- Daily-i-Forex-report-1 by Epic Research 13 May 2013Document14 pagesDaily-i-Forex-report-1 by Epic Research 13 May 2013EpicresearchPas encore d'évaluation

- Dailyfx: Dollar Consolidation Should Lead To Additional GainsDocument11 pagesDailyfx: Dollar Consolidation Should Lead To Additional GainsTitan1000Pas encore d'évaluation

- 2011 12 05 Migbank Daily Technical Analysis ReportDocument15 pages2011 12 05 Migbank Daily Technical Analysis ReportmigbankPas encore d'évaluation

- Aue4862 2016 Tut102 PDFDocument148 pagesAue4862 2016 Tut102 PDFAnonymous JKyhc5N0uPas encore d'évaluation

- Articles of Incorporation and by Laws Non Stock CorporationDocument9 pagesArticles of Incorporation and by Laws Non Stock CorporationL A AnchetaSalvia DappananPas encore d'évaluation

- Sanitary and Phytosanitary MeasuresDocument14 pagesSanitary and Phytosanitary MeasuresSlim ShadyPas encore d'évaluation

- Ambiguous Statute ConstructionDocument2 pagesAmbiguous Statute ConstructiondanPas encore d'évaluation

- Law Article 101Document30 pagesLaw Article 101Von JhenPas encore d'évaluation

- Powder Cart Med001 - Moduleb Expires 20th April 2021Document5 pagesPowder Cart Med001 - Moduleb Expires 20th April 2021Юлий ДубривныйPas encore d'évaluation

- Indemnity Form Can On Photo Marathon 2010Document1 pageIndemnity Form Can On Photo Marathon 2010Jey JuniorPas encore d'évaluation

- 40th Annual Report and AGM NoticeDocument80 pages40th Annual Report and AGM NoticeShahzad QasimPas encore d'évaluation

- QSR - 21 CFR 808 812 820Document62 pagesQSR - 21 CFR 808 812 820sunePas encore d'évaluation

- 1601 CDocument2 pages1601 CChedrick Fabros SalguetPas encore d'évaluation

- 2nd Draft of The Philippine Valuation Standards PVS 2017Document152 pages2nd Draft of The Philippine Valuation Standards PVS 2017CattPas encore d'évaluation

- CE - Marking - EN 14351Document5 pagesCE - Marking - EN 14351pedro_r_l_silva7530Pas encore d'évaluation

- Resume - JAY Shah1Document2 pagesResume - JAY Shah1Ketan VadorPas encore d'évaluation

- Ey Worldwide Transfer Pricing Reference Guide 2018 19Document588 pagesEy Worldwide Transfer Pricing Reference Guide 2018 19Kelvin RodriguezPas encore d'évaluation

- New Trade TheoryDocument17 pagesNew Trade TheoryYasmin SingaporewalaPas encore d'évaluation

- Case Study 4Document12 pagesCase Study 4Christopher Pontejo63% (8)

- Ad Valorem Bills of LadingDocument2 pagesAd Valorem Bills of LadingNikolay PetkovPas encore d'évaluation

- California Divison of Worker Compensation and Medical Billing & Payment GuideDocument176 pagesCalifornia Divison of Worker Compensation and Medical Billing & Payment Guidearunsanju78Pas encore d'évaluation

- Associated Communications & Wirless Services V NTCDocument6 pagesAssociated Communications & Wirless Services V NTCJosef MacanasPas encore d'évaluation

- LOCDocument45 pagesLOCLance MorilloPas encore d'évaluation

- The Financing of The IASB - An Analysis of Donor DiversityDocument19 pagesThe Financing of The IASB - An Analysis of Donor DiversityVitalie MihailovPas encore d'évaluation

- Reinventing Internal Controls in The Digital Age 201904 PDFDocument34 pagesReinventing Internal Controls in The Digital Age 201904 PDFFernando Sebastian Gallardo CortesPas encore d'évaluation

- Trademark Cases For IPLDocument6 pagesTrademark Cases For IPLcarinokatrinaPas encore d'évaluation

- TEA WASTE LICENSING ORDERDocument14 pagesTEA WASTE LICENSING ORDERsundarsingh5108Pas encore d'évaluation

- Understanding Construction Contracts PDFDocument39 pagesUnderstanding Construction Contracts PDFkarthikaswiPas encore d'évaluation

- Confidential Printer AgreementDocument4 pagesConfidential Printer AgreementKM GomezPas encore d'évaluation

- PC-24 Broschuere Pilatus A4 Final Spreads2b 190913Document16 pagesPC-24 Broschuere Pilatus A4 Final Spreads2b 190913hkhouaderPas encore d'évaluation

- DRAFT Hydrogen Safety Code of PracticeDocument50 pagesDRAFT Hydrogen Safety Code of PracticeSM FerdousPas encore d'évaluation

- MHC - Assignment 2Document6 pagesMHC - Assignment 2Hammad HassanPas encore d'évaluation

- Pacific Timber v. CADocument2 pagesPacific Timber v. CAkmand_lustregPas encore d'évaluation