Vous aimerez peut-être aussi

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Business Management - AssignmentDocument8 pagesBusiness Management - AssignmentHeavenlyPlanetEarth100% (6)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- Employee Benefits and ServicesDocument45 pagesEmployee Benefits and ServicesTrishaPas encore d'évaluation

- SARFESI Act Enforcement ProceduresDocument56 pagesSARFESI Act Enforcement ProcedureskannangksPas encore d'évaluation

- Dissolution and Insolvency in CooperativesDocument11 pagesDissolution and Insolvency in Cooperativeskelcy67% (3)

- Loan Proposal Sample PDFDocument4 pagesLoan Proposal Sample PDFGowsic Roolz100% (1)

- Annual Report On Uganda Petroleum Fund For The Period Ended 30 June, 2019Document13 pagesAnnual Report On Uganda Petroleum Fund For The Period Ended 30 June, 2019African Centre for Media ExcellencePas encore d'évaluation

- A1Document2 pagesA1Sean ArcillaPas encore d'évaluation

- Accounting transactions and their effectsDocument8 pagesAccounting transactions and their effectsAmalMdIsaPas encore d'évaluation

- gm11 Businessmath Annuity Part1withpetaDocument38 pagesgm11 Businessmath Annuity Part1withpetaEmer John Dela CruzPas encore d'évaluation

- Bruin Dog Grooming Journals - Rev 15Document40 pagesBruin Dog Grooming Journals - Rev 15Rishab KhandelwalPas encore d'évaluation

- Revised Service Charges Effective from 16th May 2011Document29 pagesRevised Service Charges Effective from 16th May 2011sekharhaldarPas encore d'évaluation

- Users Guide To The Volcker RuleDocument33 pagesUsers Guide To The Volcker RulemsrchandPas encore d'évaluation

- Accounting For Hire Purchase and Instalment SystemDocument16 pagesAccounting For Hire Purchase and Instalment SystemRAMEEZ. APas encore d'évaluation

- Al HawalahDocument14 pagesAl HawalahNizam BahromPas encore d'évaluation

- Dividend Model NotesDocument8 pagesDividend Model NotesLumumba KuyelaPas encore d'évaluation

- Stock InvestmentDocument61 pagesStock InvestmentKurt Geeno Du VencerPas encore d'évaluation

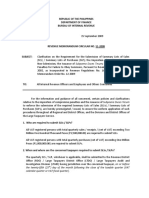

- Bir RMC 51-2009Document5 pagesBir RMC 51-2009Reg YuPas encore d'évaluation

- Rules Gross Estate Taxation PhilippinesDocument4 pagesRules Gross Estate Taxation PhilippinesMarie Tes LocsinPas encore d'évaluation

- LNL Iklcqd /: Page 1 of 3Document3 pagesLNL Iklcqd /: Page 1 of 3Kundan KumarPas encore d'évaluation

- Canadian Banks Real Estate Conference Round Up - Nov.14.2016 VeritasDocument7 pagesCanadian Banks Real Estate Conference Round Up - Nov.14.2016 VeritasKullerglasez RosePas encore d'évaluation

- Global Financial Crisis OverviDocument12 pagesGlobal Financial Crisis Overvispinor01238Pas encore d'évaluation

- Chapter Eight Advanced Investment AppraisalDocument18 pagesChapter Eight Advanced Investment Appraisalkuttan1000100% (1)

- Establishing Capital Market in Ethiopia PDFDocument73 pagesEstablishing Capital Market in Ethiopia PDFMugea Mga100% (3)

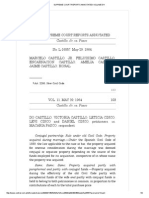

- Castillo Vs Pasco JRDocument9 pagesCastillo Vs Pasco JRThina ChiiPas encore d'évaluation

- Direct Tax Rates For Last 11 Assessment YearsDocument4 pagesDirect Tax Rates For Last 11 Assessment YearsValera HardikPas encore d'évaluation

- Amalda Aulia 1810533004 Int - AccountingDocument11 pagesAmalda Aulia 1810533004 Int - AccountingAmalda AuliaPas encore d'évaluation

- NJ Familycare Aged, Blind, Disabled Programs: Abd ChecklistDocument2 pagesNJ Familycare Aged, Blind, Disabled Programs: Abd Checklistalexverde3Pas encore d'évaluation

- CIR Vs RhombusDocument2 pagesCIR Vs RhombusKateBarrionEspinosaPas encore d'évaluation

- Receivables Management and FactoringDocument11 pagesReceivables Management and FactoringpandubhagyaPas encore d'évaluation

- Compound Interest: Prepared By: Ms. Vanessa T. Garganera, LPTDocument16 pagesCompound Interest: Prepared By: Ms. Vanessa T. Garganera, LPTIrish Dela FuentePas encore d'évaluation