Vous aimerez peut-être aussi

- Banking Domain Knowledge For TestersDocument9 pagesBanking Domain Knowledge For TestersAniket SinghPas encore d'évaluation

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeD'Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeÉvaluation : 1 sur 5 étoiles1/5 (1)

- Example Transition Project Plan ExcelDocument65 pagesExample Transition Project Plan Excelஅனுஷ்யா சார்லஸ்100% (1)

- Q: What Is The Difference Between These Administrative and Judicial Remedies?Document11 pagesQ: What Is The Difference Between These Administrative and Judicial Remedies?Kharen ValdezPas encore d'évaluation

- A Top Bloodline of The Black Nobility (Odescalchi)Document11 pagesA Top Bloodline of The Black Nobility (Odescalchi)karen hudes100% (2)

- Ebook: Blockchain Technology (English)Document25 pagesEbook: Blockchain Technology (English)BBVA Innovation Center100% (2)

- Vessel Registration GuideDocument30 pagesVessel Registration GuideeltioferdiPas encore d'évaluation

- 5cs CreditDocument6 pages5cs CreditiftikharchughtaiPas encore d'évaluation

- Uncommon GST TopicsDocument36 pagesUncommon GST TopicsEugeniePaxtonPas encore d'évaluation

- Gold Monetization Scheme: Research ReportDocument9 pagesGold Monetization Scheme: Research ReportVarun MaggonPas encore d'évaluation

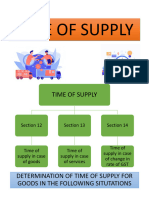

- GST For Nov 2022 & May 2023 Exams (GST Time of Supply of ServicesDocument1 pageGST For Nov 2022 & May 2023 Exams (GST Time of Supply of ServicesVikasPas encore d'évaluation

- 5 Time of SupplyDocument18 pages5 Time of SupplyDhana SekarPas encore d'évaluation

- Levy in GST S.No Particulars 1 Time of SupplyDocument7 pagesLevy in GST S.No Particulars 1 Time of SupplyAnonymous ikQZphPas encore d'évaluation

- Time of SupplyDocument31 pagesTime of SupplyNalin KPas encore d'évaluation

- Chapter 6 - Time of SupplyDocument7 pagesChapter 6 - Time of SupplyDrafts StoragePas encore d'évaluation

- Time of SupplyDocument28 pagesTime of SupplySam RockerPas encore d'évaluation

- Time of Supply: CMA Bhogavalli Mallikarjuna GuptaDocument5 pagesTime of Supply: CMA Bhogavalli Mallikarjuna Guptagurusha bhallaPas encore d'évaluation

- Time of Supply PDFDocument1 pageTime of Supply PDFjayanitrivedi03Pas encore d'évaluation

- Time of Supply PDFDocument16 pagesTime of Supply PDFNaveed AnsariPas encore d'évaluation

- Time & Value of SupplyDocument2 pagesTime & Value of SupplyRahul NegiPas encore d'évaluation

- UNIT 2 (4) Time of SupplyDocument15 pagesUNIT 2 (4) Time of SupplySania KhanPas encore d'évaluation

- Time of Supply: General Time Limit For Raising InvoicesDocument4 pagesTime of Supply: General Time Limit For Raising InvoicesPrasanthPas encore d'évaluation

- New PPTX PresentationDocument9 pagesNew PPTX PresentationdataprotaxPas encore d'évaluation

- Time of Supply of ServicesDocument10 pagesTime of Supply of ServicesShiwang AgrawalPas encore d'évaluation

- Time of Supply: When Invoice Is Issued Within Statutory Period (30 Days or 45 Days)Document3 pagesTime of Supply: When Invoice Is Issued Within Statutory Period (30 Days or 45 Days)DebaPas encore d'évaluation

- 4 Time of SupplyDocument43 pages4 Time of SupplynashwauefaPas encore d'évaluation

- All The Due Dates and Time Limits in GSTDocument10 pagesAll The Due Dates and Time Limits in GST2d77gp69kzPas encore d'évaluation

- Time of Supply INTERDocument20 pagesTime of Supply INTERKaylee WrightPas encore d'évaluation

- 4 GST Time and Value of Supply NotesDocument6 pages4 GST Time and Value of Supply NotesMurali Krishnan RPas encore d'évaluation

- Invoice InterDocument10 pagesInvoice InterKaylee WrightPas encore d'évaluation

- Time of SupplyDocument6 pagesTime of SupplygriefernjanPas encore d'évaluation

- Time of SupplyDocument4 pagesTime of SupplyAarushi GuptaPas encore d'évaluation

- S. 16: Eligibility & Conditions: Receipt of Document Forward Charge Cases (FCM)Document3 pagesS. 16: Eligibility & Conditions: Receipt of Document Forward Charge Cases (FCM)MANU SHANKARPas encore d'évaluation

- Tax Points - Reference Material: Pro Forma InvoicesDocument2 pagesTax Points - Reference Material: Pro Forma Invoicesanon_178447188Pas encore d'évaluation

- Time and Value of Supply-4Document73 pagesTime and Value of Supply-4Muhammad MehrajPas encore d'évaluation

- Idt 3Document10 pagesIdt 3manan agrawalPas encore d'évaluation

- Value of Supply: A. Supply To Unrelated Persons Where Price Is The Sole Consideration ForDocument19 pagesValue of Supply: A. Supply To Unrelated Persons Where Price Is The Sole Consideration ForPrasanthPas encore d'évaluation

- Bill of SupplyDocument3 pagesBill of SupplyAnas QasmiPas encore d'évaluation

- Basic Concepts of Transition & Invoice I20177804Document28 pagesBasic Concepts of Transition & Invoice I20177804vishalPas encore d'évaluation

- Time of SupplyDocument7 pagesTime of SupplyTushar MadanPas encore d'évaluation

- Chapter 5 WhentoPayTaxonSupplyofGoods ServicesDocument24 pagesChapter 5 WhentoPayTaxonSupplyofGoods ServicesDR. PREETI JINDALPas encore d'évaluation

- Prompt Payment To MSME VendorsDocument3 pagesPrompt Payment To MSME VendorsAmit MantryPas encore d'évaluation

- Time of Supply-20Document44 pagesTime of Supply-20Sidhant GoyalPas encore d'évaluation

- Time of Supply-IDocument50 pagesTime of Supply-IVaibhav GawadePas encore d'évaluation

- Time Value of Goods and SupplyDocument4 pagesTime Value of Goods and SupplyAnshuman ThatoiPas encore d'évaluation

- 12 List of Clarifications - Editorial Amendments - PSSCOCDocument2 pages12 List of Clarifications - Editorial Amendments - PSSCOCAlvin KangPas encore d'évaluation

- Time of Supply Under Goods and Service Tax ActDocument8 pagesTime of Supply Under Goods and Service Tax ActNarayan KabraPas encore d'évaluation

- E Flier Credit Notes in GSTDocument2 pagesE Flier Credit Notes in GSTSneha AgarwalPas encore d'évaluation

- Transitional Provisions in GST S.No Particulars 1 Transitional ProvisionsDocument8 pagesTransitional Provisions in GST S.No Particulars 1 Transitional ProvisionsAnonymous ikQZphPas encore d'évaluation

- REMEDIES by J. DimaampaoDocument2 pagesREMEDIES by J. DimaampaoJeninah Arriola CalimlimPas encore d'évaluation

- GST PPT (Group 5)Document20 pagesGST PPT (Group 5)Hanna GeorgePas encore d'évaluation

- GST1Document25 pagesGST1DeepikaPas encore d'évaluation

- GST 5.1Document46 pagesGST 5.1Raghav TiwariPas encore d'évaluation

- 7 Input Tax CreditDocument16 pages7 Input Tax CreditinstainstantuserPas encore d'évaluation

- Sop BrochureDocument6 pagesSop BrochurePhonemyat MoePas encore d'évaluation

- Tos & Vos PDFDocument42 pagesTos & Vos PDFRatulPas encore d'évaluation

- GST Seminar: Hosted By:-Akola Branch of WICASA of ICAIDocument40 pagesGST Seminar: Hosted By:-Akola Branch of WICASA of ICAINavneetPas encore d'évaluation

- Bric T&C'sDocument2 pagesBric T&C'sDavidPas encore d'évaluation

- Government RemediesDocument3 pagesGovernment RemediesShan ElisPas encore d'évaluation

- Average Due DateDocument19 pagesAverage Due DatePriyanshuPas encore d'évaluation

- Invoicing Under Goods and Service TAXDocument37 pagesInvoicing Under Goods and Service TAXAmit GuptaPas encore d'évaluation

- GST - Tax Invoice, Debit or Credit Notes, Returns, Payment of Tax PDFDocument78 pagesGST - Tax Invoice, Debit or Credit Notes, Returns, Payment of Tax PDFSapna MalikPas encore d'évaluation

- Bills of ExchangeDocument8 pagesBills of ExchangeAnonymous MhCdtwxQIPas encore d'évaluation

- Transitional ProvisionsDocument21 pagesTransitional ProvisionsRahul AkellaPas encore d'évaluation

- Debit or Credit NoteDocument6 pagesDebit or Credit Noteamolisrivastava8Pas encore d'évaluation

- CH-04 Input Tax Credit Under GST ReturnsDocument10 pagesCH-04 Input Tax Credit Under GST ReturnsSanket MhetrePas encore d'évaluation

- Tax InvoiceDocument52 pagesTax InvoicesidhantPas encore d'évaluation

- Auditors Report For NBFCDocument9 pagesAuditors Report For NBFCamidclPas encore d'évaluation

- Master Minds: No.1 For CA/CWA & MEC/CECDocument8 pagesMaster Minds: No.1 For CA/CWA & MEC/CECr_s_kediaPas encore d'évaluation

- Policy ScheduleDocument4 pagesPolicy ScheduleacrajeshPas encore d'évaluation

- Antara Bijak Sdn. BHD.: Company No: 669691 PDocument17 pagesAntara Bijak Sdn. BHD.: Company No: 669691 PIkhmil FariszPas encore d'évaluation

- PartDocument29 pagesPartPrakash KhemalapurPas encore d'évaluation

- How To Enforce Judgments Under The Civil Proceeding in MalaysiaDocument3 pagesHow To Enforce Judgments Under The Civil Proceeding in MalaysiaDevika SuppiahPas encore d'évaluation

- International Payment SystemsDocument2 pagesInternational Payment SystemsPrerna SharmaPas encore d'évaluation

- US Internal Revenue Service: 2005p1212 Sect I-IiiDocument168 pagesUS Internal Revenue Service: 2005p1212 Sect I-IiiIRSPas encore d'évaluation

- Arbitrage Calculator 3Document4 pagesArbitrage Calculator 3Eduardo MontanhaPas encore d'évaluation

- 4 Profit Planning Budgeting PDFDocument85 pages4 Profit Planning Budgeting PDFNadie LrdPas encore d'évaluation

- United States Bankruptcy Court For The District of DelawareDocument9 pagesUnited States Bankruptcy Court For The District of DelawareChapter 11 DocketsPas encore d'évaluation

- Personal Financial Statement: Section 1-Individual InformationDocument3 pagesPersonal Financial Statement: Section 1-Individual InformationAndrea MoralesPas encore d'évaluation

- Fund Flow Statement TheoryDocument3 pagesFund Flow Statement TheoryprajaktadasPas encore d'évaluation

- GST - ReturnsDocument30 pagesGST - ReturnsAniket Rastogi100% (2)

- Secretary 'S Certificate Incorporating The Board Resolution "A"Document18 pagesSecretary 'S Certificate Incorporating The Board Resolution "A"hellojdeyPas encore d'évaluation

- Name - Revati Tapaskar Roll No - 2k181175 Specialization - Finance Porter's Five Force Model of Air IndiaDocument2 pagesName - Revati Tapaskar Roll No - 2k181175 Specialization - Finance Porter's Five Force Model of Air Indiarevati tapaskarPas encore d'évaluation

- Monte Carlo - Cash Budget Models Outline and CorrelationsDocument13 pagesMonte Carlo - Cash Budget Models Outline and CorrelationsphanhailongPas encore d'évaluation

- India's Journey Towards Cashless Economy-A Study: K. Sai Pavan KumarDocument9 pagesIndia's Journey Towards Cashless Economy-A Study: K. Sai Pavan KumarSai PavanPas encore d'évaluation

- GSRTC 9-12-17.Document1 pageGSRTC 9-12-17.Nilay GandhiPas encore d'évaluation

- Bailment ContractDocument8 pagesBailment Contractadi_gupta19100% (1)

- IBA Suggested Solution First MidTerm Taxation 12072016Document9 pagesIBA Suggested Solution First MidTerm Taxation 12072016Syed Azfar HassanPas encore d'évaluation

- National General Insurance - CARFDocument2 pagesNational General Insurance - CARFCP TewPas encore d'évaluation