Vous aimerez peut-être aussi

- Mutants & Masterminds 3e - Power Profile - Death PowersDocument6 pagesMutants & Masterminds 3e - Power Profile - Death PowersMichael MorganPas encore d'évaluation

- Google Chrome OSDocument47 pagesGoogle Chrome OSnitin07sharmaPas encore d'évaluation

- President Manuel A. Roxas (1946-1948) Enacted The Following LawsDocument6 pagesPresident Manuel A. Roxas (1946-1948) Enacted The Following LawsApril Aguigam100% (1)

- Story of Carlos GarciaDocument1 pageStory of Carlos GarciaRENGIE GALOPas encore d'évaluation

- Math5 Q4 Mod10 DescribingAndComparingPropertiesOfRegularAndIrregularPolygons v1Document19 pagesMath5 Q4 Mod10 DescribingAndComparingPropertiesOfRegularAndIrregularPolygons v1ronaldPas encore d'évaluation

- The KNIGHTHOOD in RetrospectDocument25 pagesThe KNIGHTHOOD in RetrospectFajjahuj OancekPas encore d'évaluation

- Shiela Mary P. Calimag Gr. 6-St. CatherineDocument24 pagesShiela Mary P. Calimag Gr. 6-St. CatherineVanesa Calimag ClementePas encore d'évaluation

- Taxation Under Spanish and Americans.Document2 pagesTaxation Under Spanish and Americans.Gwyneth Klaire GeliPas encore d'évaluation

- n4 Verbs Root FormsDocument6 pagesn4 Verbs Root FormsRaj RamPas encore d'évaluation

- 4 - Q1 - LAS - WK 8 Day 1-5Document8 pages4 - Q1 - LAS - WK 8 Day 1-5maka yawaaa100% (1)

- Philippines Social EnvironmentDocument9 pagesPhilippines Social EnvironmentJasper CheungPas encore d'évaluation

- Tle He 6 q1 Mod3 Ict EntrepDocument21 pagesTle He 6 q1 Mod3 Ict EntrepGLORIA MACAYPas encore d'évaluation

- EPP 5 HE Module 5Document8 pagesEPP 5 HE Module 5ronaldPas encore d'évaluation

- Grade 4.centennial CELEBRATIONS - Posttest.oralDocument2 pagesGrade 4.centennial CELEBRATIONS - Posttest.oralJean Claudine Manday100% (2)

- Slidess111 PDFDocument26 pagesSlidess111 PDFdaahu dashhPas encore d'évaluation

- Technology and Livelihood Education (TLE) 6Document10 pagesTechnology and Livelihood Education (TLE) 6Louie EscuderoPas encore d'évaluation

- Agrarian Reform G3 FinalDocument38 pagesAgrarian Reform G3 FinalCRISTY LOU SAMSON BSED-1Pas encore d'évaluation

- Music6 - Q2 - Mod1 - C, G, F MajorDocument40 pagesMusic6 - Q2 - Mod1 - C, G, F MajorJohn Lorenz G. FaltiqueraPas encore d'évaluation

- PE 6 Q.2 Module 3Document3 pagesPE 6 Q.2 Module 3RjVValdezPas encore d'évaluation

- Commonwealth Government Group 3 UpdatedDocument24 pagesCommonwealth Government Group 3 UpdatedRobinPas encore d'évaluation

- q3 Las Music6 Wk6-8 Tolentino-Leonciobenigno Tarlac-CityDocument12 pagesq3 Las Music6 Wk6-8 Tolentino-Leonciobenigno Tarlac-Citymaster hamsterPas encore d'évaluation

- ST 2 - Art 6 - Q1Document3 pagesST 2 - Art 6 - Q1Dido Mamarungcas Guro Rpt100% (1)

- Summative 4.1Document1 pageSummative 4.1Shuwb Ne PheshPas encore d'évaluation

- Assessment 4 Comparative Analysis: Primary Vs Secondary SourcesDocument2 pagesAssessment 4 Comparative Analysis: Primary Vs Secondary SourcesGerald PerionPas encore d'évaluation

- 2 Puberty Quiz True of False With Answers 1Document1 page2 Puberty Quiz True of False With Answers 1pisit poladpraoPas encore d'évaluation

- Republic of The Philippines Department of Education Region III Division of City of San Fernando (P)Document6 pagesRepublic of The Philippines Department of Education Region III Division of City of San Fernando (P)Joy G. VirayPas encore d'évaluation

- Secular MusicDocument5 pagesSecular MusicAngelle BahinPas encore d'évaluation

- Vdocuments - MX Pambansang Sagisag NG PilipinasDocument21 pagesVdocuments - MX Pambansang Sagisag NG PilipinasMersad Aras100% (1)

- Tle Agri 6 Week 8Document113 pagesTle Agri 6 Week 8Paaralang Elementarya ng Kinalaglagan (R IV-A - Batangas)Pas encore d'évaluation

- English 5 - Q3 - MELC1-7 - QA RFTATDocument36 pagesEnglish 5 - Q3 - MELC1-7 - QA RFTATRonnie Francisco Tejano100% (1)

- Template - PE 7 Q2 Module 1Document15 pagesTemplate - PE 7 Q2 Module 1Michaela Teodoro100% (1)

- Tle Agriculture AnimalsDocument2 pagesTle Agriculture AnimalsRonel Sayaboc AsuncionPas encore d'évaluation

- ART 6 1st Quarter Module 4Document11 pagesART 6 1st Quarter Module 4Salve Serrano100% (1)

- 1 Asexula Reproduction in PlantsDocument18 pages1 Asexula Reproduction in PlantsJojo AcuñaPas encore d'évaluation

- Taxation in Spanish Philippines: Evolution of Philippine TaxationDocument16 pagesTaxation in Spanish Philippines: Evolution of Philippine TaxationC. I .APas encore d'évaluation

- Eng Epp Ap Math5 - ST3 - Q1Document8 pagesEng Epp Ap Math5 - ST3 - Q1Aiza Conchada100% (1)

- Science Summative No.4Document53 pagesScience Summative No.4mhafolzPas encore d'évaluation

- Grade 5: Mathematics Edukasyong Pantahanan at Pangkabuhayan 5 Quarter 4 - Week 2Document27 pagesGrade 5: Mathematics Edukasyong Pantahanan at Pangkabuhayan 5 Quarter 4 - Week 2Neri ErinPas encore d'évaluation

- II. Find The Quotient of The FollowingDocument2 pagesII. Find The Quotient of The Followingpot pooot100% (1)

- Physical Fitness MapehDocument25 pagesPhysical Fitness Mapehjohn lesterPas encore d'évaluation

- MAPEH 5 - Module 3 - Answer KeyDocument2 pagesMAPEH 5 - Module 3 - Answer KeyNard Lastimosa0% (2)

- Sci Sum First Grading No. 2Document18 pagesSci Sum First Grading No. 2Paul Aldrin OlaeraPas encore d'évaluation

- Heneral Emilio Aguinaldo: Mga Gunita NG HimagsikanDocument2 pagesHeneral Emilio Aguinaldo: Mga Gunita NG HimagsikanDanielle Bartolome100% (1)

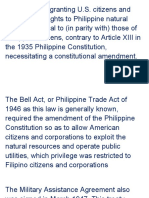

- Parity RightsDocument4 pagesParity RightsGlaiza Lyn JumamilPas encore d'évaluation

- Science q1 w2 Day 1-5Document43 pagesScience q1 w2 Day 1-5marilou soriano0% (1)

- TLE - ScriptDocument4 pagesTLE - ScriptverenicaPas encore d'évaluation

- Q3 Las EppDocument6 pagesQ3 Las EppedelbertoPas encore d'évaluation

- Science 3 FormativeDocument92 pagesScience 3 FormativeEr Ma100% (1)

- Science5 Q4 Module3 Week3 21pDocument21 pagesScience5 Q4 Module3 Week3 21praymondcapePas encore d'évaluation

- How Matter Changes When Applied With Heat - FINAL07182020Document19 pagesHow Matter Changes When Applied With Heat - FINAL07182020TEAM KnightzPas encore d'évaluation

- Math - 6 Module - Q4 - M1Document11 pagesMath - 6 Module - Q4 - M1Miriam Haber BarnachiaPas encore d'évaluation

- Ap 5 Las Q4Document52 pagesAp 5 Las Q4ALBA JANE WENDAMPas encore d'évaluation

- Postwar Problems and The Republic (AutoRecovered)Document2 pagesPostwar Problems and The Republic (AutoRecovered)Rachel Nicole100% (1)

- Parable of The Pharisee and The Tax Collector 2 Feb 2018Document2 pagesParable of The Pharisee and The Tax Collector 2 Feb 2018Caroline PPas encore d'évaluation

- Quarter 2 - Module 1: Explore Significant Information: EnglishDocument32 pagesQuarter 2 - Module 1: Explore Significant Information: EnglishEmily Ramos100% (1)

- ARAL PAN 4 QTR 1 WEEK 6-EDITEDDocument16 pagesARAL PAN 4 QTR 1 WEEK 6-EDITEDAmy MacahindogPas encore d'évaluation

- Mathematics: Quarter 1 - Module 13Document24 pagesMathematics: Quarter 1 - Module 13Che LVPas encore d'évaluation

- Implementation of Plan On Animalfish RaisingDocument4 pagesImplementation of Plan On Animalfish Raisingpaulo zotoPas encore d'évaluation

- Administration of Elpidio QuirinoDocument7 pagesAdministration of Elpidio QuirinoJhay R de LeonPas encore d'évaluation

- The Declaration of The Philippine Independence - GEC-2-RPH - BSN-1-B - CABUGATAN J AL-KHAIRAH ODocument2 pagesThe Declaration of The Philippine Independence - GEC-2-RPH - BSN-1-B - CABUGATAN J AL-KHAIRAH OACPas encore d'évaluation

- Agri-Fishery Arts: Module 15: Marketing Raised or Cultured FishDocument20 pagesAgri-Fishery Arts: Module 15: Marketing Raised or Cultured Fishfaithraque mendozaPas encore d'évaluation

- TaxationDocument34 pagesTaxationLOREEN BERNICE LACSONPas encore d'évaluation

- PROFED 2 Learning TheoriesDocument3 pagesPROFED 2 Learning TheoriesK. U. A.Pas encore d'évaluation

- PROFED 1 Midterm Reviewer (Questions)Document4 pagesPROFED 1 Midterm Reviewer (Questions)K. U. A.Pas encore d'évaluation

- PROFED 1 Midterm ReviewerDocument4 pagesPROFED 1 Midterm ReviewerK. U. A.Pas encore d'évaluation

- GEC 102 Historical ResearchDocument27 pagesGEC 102 Historical ResearchK. U. A.Pas encore d'évaluation

- GEC 102 Midterm ReviewerDocument6 pagesGEC 102 Midterm ReviewerK. U. A.Pas encore d'évaluation

- GEC 101 Midterm ReviewerDocument5 pagesGEC 101 Midterm ReviewerK. U. A.Pas encore d'évaluation

- SOLO FrameworkDocument12 pagesSOLO FrameworkMaureen Leafeiiel Salahid100% (2)

- National Healthy Lifestyle ProgramDocument6 pagesNational Healthy Lifestyle Programmale nursePas encore d'évaluation

- Compare Visual Studio 2013 EditionsDocument3 pagesCompare Visual Studio 2013 EditionsankurbhatiaPas encore d'évaluation

- Congestion AvoidanceDocument23 pagesCongestion AvoidanceTheIgor997Pas encore d'évaluation

- Pencak Silat New Rules 2020 - Slides Presentation (International) - As of 22 Aug 2020 - 1000hrs (1) (201-400)Document200 pagesPencak Silat New Rules 2020 - Slides Presentation (International) - As of 22 Aug 2020 - 1000hrs (1) (201-400)Yasin ilmansyah hakimPas encore d'évaluation

- 03-Volume II-A The MIPS64 Instruction Set (MD00087)Document793 pages03-Volume II-A The MIPS64 Instruction Set (MD00087)miguel gonzalezPas encore d'évaluation

- Effect of Innovative Leadership On Teacher's Job Satisfaction Mediated of A Supportive EnvironmentDocument10 pagesEffect of Innovative Leadership On Teacher's Job Satisfaction Mediated of A Supportive EnvironmentAPJAET JournalPas encore d'évaluation

- Cui Et Al. 2017Document10 pagesCui Et Al. 2017Manaswini VadlamaniPas encore d'évaluation

- Bike Chasis DesignDocument7 pagesBike Chasis Designparth sarthyPas encore d'évaluation

- Kangaroo High Build Zinc Phosphate PrimerDocument2 pagesKangaroo High Build Zinc Phosphate PrimerChoice OrganoPas encore d'évaluation

- 5.4 Marketing Arithmetic For Business AnalysisDocument12 pages5.4 Marketing Arithmetic For Business AnalysisashPas encore d'évaluation

- How To Select The Right Motor DriverDocument4 pagesHow To Select The Right Motor DriverHavandinhPas encore d'évaluation

- IsaiahDocument7 pagesIsaiahJett Rovee Navarro100% (1)

- Propht William Marrion Branham Vist IndiaDocument68 pagesPropht William Marrion Branham Vist IndiaJoshuva Daniel86% (7)

- A Mercy Guided StudyDocument23 pagesA Mercy Guided StudyAnas HudsonPas encore d'évaluation

- Bon JourDocument15 pagesBon JourNikolinaJamicic0% (1)

- Robot 190 & 1110 Op - ManualsDocument112 pagesRobot 190 & 1110 Op - ManualsSergeyPas encore d'évaluation

- The Bipolar Affective Disorder Dimension Scale (BADDS) - A Dimensional Scale For Rating Lifetime Psychopathology in Bipolar Spectrum DisordersDocument11 pagesThe Bipolar Affective Disorder Dimension Scale (BADDS) - A Dimensional Scale For Rating Lifetime Psychopathology in Bipolar Spectrum DisordersDM YazdaniPas encore d'évaluation

- Event Planning Sample Cover Letter and ItineraryDocument6 pagesEvent Planning Sample Cover Letter and ItineraryWhitney Mae HaddardPas encore d'évaluation

- Surge Protectionfor ACMachineryDocument8 pagesSurge Protectionfor ACMachineryvyroreiPas encore d'évaluation

- Hayat ProposalDocument22 pagesHayat Proposalsebehadinahmed1992Pas encore d'évaluation

- Appendix I - Plant TissuesDocument24 pagesAppendix I - Plant TissuesAmeera ChaitramPas encore d'évaluation

- ESS Revision Session 2 - Topics 5-8 & P1 - 2Document54 pagesESS Revision Session 2 - Topics 5-8 & P1 - 2jinLPas encore d'évaluation

- Bus Organization of 8085 MicroprocessorDocument6 pagesBus Organization of 8085 MicroprocessorsrikrishnathotaPas encore d'évaluation

- Forensic BallisticsDocument23 pagesForensic BallisticsCristiana Jsu DandanPas encore d'évaluation

- Judges Kings ProphetsDocument60 pagesJudges Kings ProphetsKim John BolardePas encore d'évaluation

- Evolution Epidemiology and Etiology of Temporomandibular Joint DisordersDocument6 pagesEvolution Epidemiology and Etiology of Temporomandibular Joint DisordersCM Panda CedeesPas encore d'évaluation

- LECTURE 1.COMMUNICATION PROCESSES, PRINCIPLES, AND ETHICS - Ver 2Document24 pagesLECTURE 1.COMMUNICATION PROCESSES, PRINCIPLES, AND ETHICS - Ver 2Trixia Nicole De LeonPas encore d'évaluation