Vous aimerez peut-être aussi

- Olympiad Sample Paper 3: Useful for Olympiad conducted at School, National & International levelsD'EverandOlympiad Sample Paper 3: Useful for Olympiad conducted at School, National & International levelsÉvaluation : 1 sur 5 étoiles1/5 (1)

- Accounting Cycle Applied To A Service Business (Part 2) : Quarter 4, Week 1-2Document18 pagesAccounting Cycle Applied To A Service Business (Part 2) : Quarter 4, Week 1-2アイバニーズ ダニカPas encore d'évaluation

- ACC 122 SAS DAY 21 QUIZ - Docx-2Document10 pagesACC 122 SAS DAY 21 QUIZ - Docx-2Aldrin Dela CruzPas encore d'évaluation

- 2020 - Semester 1 Exam - Unit 3Document31 pages2020 - Semester 1 Exam - Unit 3EdwinPas encore d'évaluation

- 3 Term SY 2019-2020: Midterm ExaminationDocument10 pages3 Term SY 2019-2020: Midterm ExaminationAdolph Christian GonzalesPas encore d'évaluation

- Exam Iv Spring 2008: BAN 530 Ves/VpmDocument14 pagesExam Iv Spring 2008: BAN 530 Ves/VpmKasim MergaPas encore d'évaluation

- PME CM Midterm Assessment Assignment Spring 20 14052020 083835amDocument3 pagesPME CM Midterm Assessment Assignment Spring 20 14052020 083835amSharjeel Humayun HassanPas encore d'évaluation

- Erp Practice Exam4-2014 PDFDocument40 pagesErp Practice Exam4-2014 PDFagamemnon8899Pas encore d'évaluation

- MCQ Cma Inter-P8 CostingDocument58 pagesMCQ Cma Inter-P8 Costingsekhee1011Pas encore d'évaluation

- Ca5101 PDFDocument12 pagesCa5101 PDFNiccoRobDeCastroPas encore d'évaluation

- MGT 111 - Course SyllabusDocument2 pagesMGT 111 - Course SyllabusFerraci Sanvictores0% (1)

- FinalexamDocument14 pagesFinalexamSureshPas encore d'évaluation

- (Ust-Jpia) Ca51016 Ia3 Mock Preliminary Examination ReviewerDocument12 pages(Ust-Jpia) Ca51016 Ia3 Mock Preliminary Examination Reviewerhpp academicmaterialsPas encore d'évaluation

- (Ust-Jpia) Ca51016 Ia3 Mock Preliminary Examination ReviewerDocument12 pages(Ust-Jpia) Ca51016 Ia3 Mock Preliminary Examination Reviewerhpp academicmaterialsPas encore d'évaluation

- Mas 310 - Operations ManagementDocument6 pagesMas 310 - Operations ManagementSuman ChaudharyPas encore d'évaluation

- 2021 MSHS Exam - SolutionsDocument25 pages2021 MSHS Exam - Solutionscharlie.young2Pas encore d'évaluation

- Polytechnic University of The PhilippinesDocument13 pagesPolytechnic University of The PhilippinesNathalie Padilla100% (1)

- CAI Model Test Paper Vol. II TextDocument456 pagesCAI Model Test Paper Vol. II TextChittiappa ChendrimadaPas encore d'évaluation

- Acct3044 2020Document3 pagesAcct3044 2020sharnette.daley22Pas encore d'évaluation

- 27th Batch First PB MasDocument11 pages27th Batch First PB MasRommel Royce100% (1)

- CT Maf151 Q MayDocument9 pagesCT Maf151 Q May2022459384Pas encore d'évaluation

- Bus359-Operations and Supply Chain Management-Final Exam-02Document4 pagesBus359-Operations and Supply Chain Management-Final Exam-02Thu ĐinhPas encore d'évaluation

- MA QB September 2020-August 2021 As at 15 April 2020 FINALDocument301 pagesMA QB September 2020-August 2021 As at 15 April 2020 FINALOlha L100% (1)

- Ujian Akhir Semester Ganjil TAHUN AKADEMIK 2020/2021: Fakultas: Ekonomi - Bisnis & Manajemen - Teknik - Bahasa - DKVDocument3 pagesUjian Akhir Semester Ganjil TAHUN AKADEMIK 2020/2021: Fakultas: Ekonomi - Bisnis & Manajemen - Teknik - Bahasa - DKVeXpadaPas encore d'évaluation

- Erp Practice Exam3-2014 PDFDocument40 pagesErp Practice Exam3-2014 PDFagamemnon8899Pas encore d'évaluation

- MBA 20 CMA MID-TERM EXAM 19-01-2022 - Olumide ObanlaDocument10 pagesMBA 20 CMA MID-TERM EXAM 19-01-2022 - Olumide Obanlafrank gboPas encore d'évaluation

- COST ACCTG Semi Final Exam 2020Document9 pagesCOST ACCTG Semi Final Exam 2020TyrsonPas encore d'évaluation

- Reviewer From Idk WhereDocument10 pagesReviewer From Idk WherePATRICIA SANTOSPas encore d'évaluation

- Acca107 Strat Cost MGT PrelimsDocument2 pagesAcca107 Strat Cost MGT PrelimsShaneen AdorablePas encore d'évaluation

- WwwwweweweweweDocument4 pagesWwwwweweweweweFrank Anthony Apus ApusPas encore d'évaluation

- Review Class For Final Exam 2016, For Moodle, With SolutionDocument17 pagesReview Class For Final Exam 2016, For Moodle, With SolutionMaxPas encore d'évaluation

- Types of Major AccountsDocument6 pagesTypes of Major Accountsbbrightvc 一ไบร์ทPas encore d'évaluation

- Ais205 June 23Document7 pagesAis205 June 23ediza adha0% (1)

- Senior 12 FABM2 Q1 - M7Document20 pagesSenior 12 FABM2 Q1 - M7Sitti Halima Amilbahar AdgesPas encore d'évaluation

- 4 Cost Acconting Class XII CommerceDocument60 pages4 Cost Acconting Class XII Commercegangadharp497Pas encore d'évaluation

- Ia1 Posttest3 - Inventories (Questionnaire)Document8 pagesIa1 Posttest3 - Inventories (Questionnaire)Chris JacksonPas encore d'évaluation

- ACCT 2010: Principles of Accounting I Mini Exam 1 Monday September 26, 2016 8-9 P.M. LTADocument6 pagesACCT 2010: Principles of Accounting I Mini Exam 1 Monday September 26, 2016 8-9 P.M. LTAPak HoPas encore d'évaluation

- FIN3702 MayJune2022Document21 pagesFIN3702 MayJune2022kevinedgarjacobsPas encore d'évaluation

- Strategic Cost Management Coordinated Quiz 2Document8 pagesStrategic Cost Management Coordinated Quiz 2Kim TaehyungPas encore d'évaluation

- Quiz 9 - Subs Test - Audit of Inventory (KEY)Document4 pagesQuiz 9 - Subs Test - Audit of Inventory (KEY)Kenneth Christian WilburPas encore d'évaluation

- Lesson 002 Branches of AccountingDocument4 pagesLesson 002 Branches of AccountingYnnoJhom harthartPas encore d'évaluation

- COHRA1-B22 - Take-Home Assessment 1 - Paper Block 2 2021 (V1.0) PDFDocument15 pagesCOHRA1-B22 - Take-Home Assessment 1 - Paper Block 2 2021 (V1.0) PDFjoseph mphahoPas encore d'évaluation

- Commerce MCQs Practice Test 1Document7 pagesCommerce MCQs Practice Test 1SujitPas encore d'évaluation

- Erp Practice Exam1-2014Document41 pagesErp Practice Exam1-2014Anas JivrajPas encore d'évaluation

- September 12, 2023 DLL Q1Document3 pagesSeptember 12, 2023 DLL Q1Robert Del PilarPas encore d'évaluation

- Mas - 4Document12 pagesMas - 4AzureBlazePas encore d'évaluation

- Answer Sheet: Maximum of 15 Sentences Only Per Number/question DUE NOVEMBER 10, 2020Document3 pagesAnswer Sheet: Maximum of 15 Sentences Only Per Number/question DUE NOVEMBER 10, 2020Arven FrancoPas encore d'évaluation

- 21937mtp Cptvolu2 Part1Document114 pages21937mtp Cptvolu2 Part1Govind SharmaPas encore d'évaluation

- CaatsDocument4 pagesCaatsamormi2702Pas encore d'évaluation

- LogicDocument7 pagesLogicMuhammad HamzaPas encore d'évaluation

- Assignment 5 - MGT230 Mock Final Exam.Document6 pagesAssignment 5 - MGT230 Mock Final Exam.hamzaPas encore d'évaluation

- Lean Manufacturing Quiz IDocument18 pagesLean Manufacturing Quiz IDiệp Nguyễn67% (6)

- CA Inter CMA - Amendment Batch 1 NotesDocument59 pagesCA Inter CMA - Amendment Batch 1 NotesTapoprabho PaulPas encore d'évaluation

- Pathfinder Intermediate Nov 2012Document115 pagesPathfinder Intermediate Nov 2012ALIU HADIPas encore d'évaluation

- Commerce MCQs Practice Test 1Document8 pagesCommerce MCQs Practice Test 1Nirakar GoudaPas encore d'évaluation

- 1 5 ChaptersDocument8 pages1 5 ChaptersshahabPas encore d'évaluation

- LaluGdeMuhammadFarizt - UTS Impl Sistem Ent 2Document3 pagesLaluGdeMuhammadFarizt - UTS Impl Sistem Ent 2lalu gdePas encore d'évaluation

- Cost Accounting Week 2Document15 pagesCost Accounting Week 2AbraPas encore d'évaluation

- Sample Haiku BoholDocument11 pagesSample Haiku BoholAbraPas encore d'évaluation

- Talanyo Folio FinalDocument55 pagesTalanyo Folio FinalAbra100% (1)

- Prepared By: Bagsaw, Frince Jericho Tesalona, Jin Mei Yncierto, Hannah LynneDocument12 pagesPrepared By: Bagsaw, Frince Jericho Tesalona, Jin Mei Yncierto, Hannah LynneAbraPas encore d'évaluation

- Nego Notice of DishonorDocument6 pagesNego Notice of DishonorAbraPas encore d'évaluation

- Compensation and BenefitsDocument4 pagesCompensation and BenefitsNiño Sismoan BenigayPas encore d'évaluation

- ADF Annual Report 2010-11 FinalDocument100 pagesADF Annual Report 2010-11 Finalajey_p1270Pas encore d'évaluation

- 07 - Employee HandbookDocument19 pages07 - Employee HandbookAesha ShahPas encore d'évaluation

- Set-On (In Case of Huge Profits,)Document10 pagesSet-On (In Case of Huge Profits,)Dhananjayan GopinathanPas encore d'évaluation

- Learning Activity Sheets: Business MathematicsDocument4 pagesLearning Activity Sheets: Business MathematicsKimberly Lagman100% (1)

- Labor Law (Bam210) Modules3&4Document27 pagesLabor Law (Bam210) Modules3&4Lord ZyrusPas encore d'évaluation

- Accenture Mettle - QuantsDocument32 pagesAccenture Mettle - QuantsHarshithaPas encore d'évaluation

- Sameer vs. CabilesDocument33 pagesSameer vs. CabilesKate DomingoPas encore d'évaluation

- Portugal: Employment Law Overview 2021-2022Document34 pagesPortugal: Employment Law Overview 2021-2022Wisnu WiwekaPas encore d'évaluation

- College of BusiDocument42 pagesCollege of BusiDamtewPas encore d'évaluation

- Toaz - Info 4 First Comprehensive Test PRDocument11 pagesToaz - Info 4 First Comprehensive Test PRJade VillanuevaPas encore d'évaluation

- Heacock vs. NLUDocument4 pagesHeacock vs. NLUDIGNA HERNANDEZPas encore d'évaluation

- Randstad Guide Salarial en 2019 WebDocument152 pagesRandstad Guide Salarial en 2019 Webdivyaunsh dandPas encore d'évaluation

- Case Digests - Labor Rev - Atty LorenzoDocument90 pagesCase Digests - Labor Rev - Atty LorenzoRewsEn50% (2)

- Journal Entries Answer KeyDocument12 pagesJournal Entries Answer KeyEdna MingPas encore d'évaluation

- GPF All FormsDocument66 pagesGPF All Formsnkj9512Pas encore d'évaluation

- Thangarasu Offer Letter 1 YearDocument5 pagesThangarasu Offer Letter 1 YeargokulvaratharajanPas encore d'évaluation

- C.G. - Greenbury CommitteeDocument15 pagesC.G. - Greenbury Committeeitsme_varun100% (3)

- Ho - Liquid Lives, Compensation, Schemes and Making of (Unsustainable) Financial MarketsDocument1 pageHo - Liquid Lives, Compensation, Schemes and Making of (Unsustainable) Financial MarketsEthanPas encore d'évaluation

- Complete Your Enrolment Process Siddesh PPDocument6 pagesComplete Your Enrolment Process Siddesh PPSiddesh PingalePas encore d'évaluation

- 2014 Pharmaceutical Salary SurveyDocument64 pages2014 Pharmaceutical Salary SurveyClinical Professionals Ltd100% (1)

- Insular Bank of Asia vs. InciongDocument11 pagesInsular Bank of Asia vs. InciongChristiane Marie BajadaPas encore d'évaluation

- Workbook 1A5Document3 pagesWorkbook 1A5Analy Maritza Phocco CanazaPas encore d'évaluation

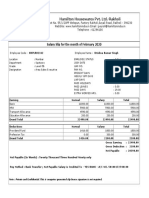

- Hamilton Housewares Pvt. Ltd.-Rakholi: Salary Slip For The Month of February 2020Document1 pageHamilton Housewares Pvt. Ltd.-Rakholi: Salary Slip For The Month of February 2020KRISHNA SINGHPas encore d'évaluation

- GR L49774 - San Miguel Corporation Vs Inchiong (103 SCRA 139, 1981)Document3 pagesGR L49774 - San Miguel Corporation Vs Inchiong (103 SCRA 139, 1981)Belle ConcepcionPas encore d'évaluation

- Hoffman PDFDocument59 pagesHoffman PDFphifzer2Pas encore d'évaluation

- 2010 Hays Salary Guide in AsiaDocument60 pages2010 Hays Salary Guide in AsiaJarvisPas encore d'évaluation

- Human Resource Engineering Case StudyDocument14 pagesHuman Resource Engineering Case StudyL.a. Ladores100% (1)

- Form 16Document6 pagesForm 16Pulkit Gupta100% (1)

- Big 2 RevisiDocument7 pagesBig 2 RevisiIwan KurniawanPas encore d'évaluation