Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Management 3120 ReviewDocument27 pagesManagement 3120 ReviewChristina RomanoPas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Management 3120 ReviewDocument27 pagesManagement 3120 ReviewChristina RomanoPas encore d'évaluation

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Macro Eco ReviewDocument7 pagesMacro Eco ReviewChristina RomanoPas encore d'évaluation

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- MGT Review SheetDocument6 pagesMGT Review SheetChristina RomanoPas encore d'évaluation

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- MGT Review SheetDocument6 pagesMGT Review SheetChristina RomanoPas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Macro Eco ReviewDocument7 pagesMacro Eco ReviewChristina RomanoPas encore d'évaluation

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Macro Eco ReviewDocument7 pagesMacro Eco ReviewChristina RomanoPas encore d'évaluation

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Cis ReviewDocument13 pagesCis ReviewChristina RomanoPas encore d'évaluation

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Film CritiqueDocument8 pagesFilm CritiqueChristina RomanoPas encore d'évaluation

- Psych 2Document2 pagesPsych 2Christina RomanoPas encore d'évaluation

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- MGT 3121Document18 pagesMGT 3121Christina RomanoPas encore d'évaluation

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- Macro 2Document9 pagesMacro 2Christina RomanoPas encore d'évaluation

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Psych 3Document2 pagesPsych 3Christina RomanoPas encore d'évaluation

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Last Psych TestDocument2 pagesLast Psych TestChristina RomanoPas encore d'évaluation

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Persuasive SpeechDocument2 pagesPersuasive SpeechChristina RomanoPas encore d'évaluation

- MGT Cheat SheetDocument3 pagesMGT Cheat SheetChristina RomanoPas encore d'évaluation

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Law 2-13Document1 pageLaw 2-13Christina RomanoPas encore d'évaluation

- Final Review For LawDocument11 pagesFinal Review For LawChristina RomanoPas encore d'évaluation

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Acc 2101Document5 pagesAcc 2101Christina RomanoPas encore d'évaluation

- Fin Cheat SheetDocument3 pagesFin Cheat SheetChristina RomanoPas encore d'évaluation

- Law 3-1-18Document5 pagesLaw 3-1-18Christina RomanoPas encore d'évaluation

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Law ReviewDocument1 pageLaw ReviewChristina RomanoPas encore d'évaluation

- Eco 2-13-18Document22 pagesEco 2-13-18Christina RomanoPas encore d'évaluation

- Pas 29Document6 pagesPas 29AnnePas encore d'évaluation

- FM W10a 1902Document9 pagesFM W10a 1902jonathanchristiandri2258Pas encore d'évaluation

- They Use That Information To Make Important Decisions.: Chapter 1: Accouting and The Business Environment Page 1 of 91Document91 pagesThey Use That Information To Make Important Decisions.: Chapter 1: Accouting and The Business Environment Page 1 of 91Joshe Dela Cruz100% (1)

- AFAR 03 Partnership DissolutionDocument4 pagesAFAR 03 Partnership DissolutionDerick jorgePas encore d'évaluation

- Lecture 2 Operational Gearing ExampleDocument5 pagesLecture 2 Operational Gearing ExampleQi ZhuPas encore d'évaluation

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Strategic Business Reporting Class Notes: (International)Document259 pagesStrategic Business Reporting Class Notes: (International)Ramen ACCA100% (1)

- Central Depository Company OF Pakistan Limited: An OverviewDocument22 pagesCentral Depository Company OF Pakistan Limited: An OverviewFa De-qPas encore d'évaluation

- Chapter 19 Managing Inventory, Accounts Receivable and Accounts PayableDocument38 pagesChapter 19 Managing Inventory, Accounts Receivable and Accounts PayableJan ryanPas encore d'évaluation

- MiniScribe Corporation - FSDocument5 pagesMiniScribe Corporation - FSNinaMartirezPas encore d'évaluation

- 4 Financial Statement AnalysisDocument28 pages4 Financial Statement Analysisrommel legaspi100% (2)

- Practice Quiz6 Module 3 Financial MarketsDocument4 pagesPractice Quiz6 Module 3 Financial MarketsMuhire Kevine50% (2)

- Taxation Law Answers in Assignment and QuizDocument9 pagesTaxation Law Answers in Assignment and QuizAngie JosolPas encore d'évaluation

- Board StructureDocument14 pagesBoard StructureJoeWai LeongPas encore d'évaluation

- Third Quiz For FABM2 (On Adjusting, Closing, and Reversing Entries)Document2 pagesThird Quiz For FABM2 (On Adjusting, Closing, and Reversing Entries)SITTIE RAYMAH ABDULLAHPas encore d'évaluation

- The Following Information For CLH Company Is Available On June 30, 2018, The End of A MonthlyDocument5 pagesThe Following Information For CLH Company Is Available On June 30, 2018, The End of A MonthlyJel SanPas encore d'évaluation

- Financial Management: Charak RayDocument36 pagesFinancial Management: Charak RayCHARAK RAYPas encore d'évaluation

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Accounting For Specialized Institution Set 2 Scheme of ValuationDocument19 pagesAccounting For Specialized Institution Set 2 Scheme of ValuationTitus Clement100% (1)

- Cpa Review School of The Philippines ManilaDocument3 pagesCpa Review School of The Philippines ManilaAljur SalamedaPas encore d'évaluation

- Tutorial 3 For FM-IDocument5 pagesTutorial 3 For FM-IarishthegreatPas encore d'évaluation

- Chapter 3 - Sources of CapitalDocument7 pagesChapter 3 - Sources of CapitalAnthony BalandoPas encore d'évaluation

- Group3 - CFEV - Project Presentation - Fin-MismanagementDocument11 pagesGroup3 - CFEV - Project Presentation - Fin-MismanagementDeepak SoodPas encore d'évaluation

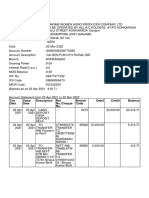

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument16 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceTanu ParidaPas encore d'évaluation

- Automobile IndustryDocument7 pagesAutomobile IndustryAniket VermaPas encore d'évaluation

- Derivatives and Foreign Currency TransacDocument2 pagesDerivatives and Foreign Currency TransacJade jade jadePas encore d'évaluation

- Gambit Corporation Purchased A New Plant Asset On April 1Document1 pageGambit Corporation Purchased A New Plant Asset On April 1Freelance WorkerPas encore d'évaluation

- SUULD 16092023144813 Newspaper IntimationDocument25 pagesSUULD 16092023144813 Newspaper IntimationcadurgayPas encore d'évaluation

- Insolvency and Bankruptcy Code 2016Document6 pagesInsolvency and Bankruptcy Code 2016Taxmann PublicationPas encore d'évaluation

- 2 Past Year Q'sDocument7 pages2 Past Year Q'sJhagantini PalaniveluPas encore d'évaluation

- DRHP AimlDocument636 pagesDRHP AimlSubscriptionPas encore d'évaluation

- Assignment On Powers of Corporation Pt. 3 Name: Section: Date: ScoreDocument2 pagesAssignment On Powers of Corporation Pt. 3 Name: Section: Date: ScoreKris Tine100% (1)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSND'Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNÉvaluation : 4.5 sur 5 étoiles4.5/5 (3)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaD'EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (14)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisD'EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisÉvaluation : 5 sur 5 étoiles5/5 (6)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successD'EverandReady, Set, Growth hack:: A beginners guide to growth hacking successÉvaluation : 4.5 sur 5 étoiles4.5/5 (93)