Vous aimerez peut-être aussi

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- 1300 Maxtrak Manual PartsDocument396 pages1300 Maxtrak Manual PartsMariano David Pons Merino86% (7)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- F2cfe613 Fjbfe613Document518 pagesF2cfe613 Fjbfe613jvega_534120100% (3)

- T433 T503 T553 WorkshopDocument268 pagesT433 T503 T553 WorkshopstevePas encore d'évaluation

- XT 125 2005Document32 pagesXT 125 2005Alex Rey50% (2)

- 8098 pt1Document385 pages8098 pt1Hotib PerwiraPas encore d'évaluation

- Vision Class SyllabusDocument7 pagesVision Class SyllabuscaliechPas encore d'évaluation

- History 41 Poem My Pain Runs DeepDocument1 pageHistory 41 Poem My Pain Runs DeepcaliechPas encore d'évaluation

- Tips For Successful LeadershipDocument19 pagesTips For Successful LeadershipcaliechPas encore d'évaluation

- Payroll Setup ChecklistDocument4 pagesPayroll Setup ChecklistcaliechPas encore d'évaluation

- Ritual WorksheetDocument2 pagesRitual Worksheetcaliech100% (1)

- John Doe Smith 2 CHH ST BILE, GA 35555Document1 pageJohn Doe Smith 2 CHH ST BILE, GA 35555caliechPas encore d'évaluation

- Page 2Document2 pagesPage 2caliechPas encore d'évaluation

- 504 SNCR FLS SNCR SystemDocument10 pages504 SNCR FLS SNCR Systemvũ minh tâmPas encore d'évaluation

- Perkins: Engine: 1106C-E60TADocument2 pagesPerkins: Engine: 1106C-E60TAEricPas encore d'évaluation

- PTQ Q2 2014 PDFDocument132 pagesPTQ Q2 2014 PDFAntHony K-ianPas encore d'évaluation

- Full Presentation CompressedDocument253 pagesFull Presentation Compressedanon-940570100% (4)

- 2090 9tonne Front Tip UK PDFDocument2 pages2090 9tonne Front Tip UK PDFQuelmis De La Cruz Vilca AmesquitaPas encore d'évaluation

- Aug 22 C1 - Reading Test 2Document4 pagesAug 22 C1 - Reading Test 2Sunshine Hann71% (7)

- Coal Fired Thermal GenerationDocument4 pagesCoal Fired Thermal GenerationMuhammad Ahsan MushtaqPas encore d'évaluation

- Crank Shaft & Connecting Rod DesignDocument34 pagesCrank Shaft & Connecting Rod DesignVaraprasad Rao67% (3)

- GUIDE For COW PDFDocument85 pagesGUIDE For COW PDFnckpourlasPas encore d'évaluation

- Catalogo Motor KubotaDocument16 pagesCatalogo Motor KubotaLilly Novillo100% (1)

- ProSep Project and Company PicturesDocument35 pagesProSep Project and Company PicturesRiu100% (1)

- TM9-813 6x6 Truck White Corbitt Brockway PDFDocument339 pagesTM9-813 6x6 Truck White Corbitt Brockway PDFdieudecafePas encore d'évaluation

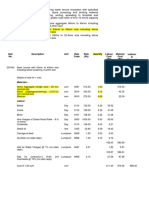

- Item No. Description Unit Rate Code Rate (RS) Quantity Labour Cost (RS) Material Cost (RS)Document1 pageItem No. Description Unit Rate Code Rate (RS) Quantity Labour Cost (RS) Material Cost (RS)RANADIP100% (2)

- General Information and Operating Instructions: GPU - 406 GPU - 409Document42 pagesGeneral Information and Operating Instructions: GPU - 406 GPU - 409William Jaldin CorralesPas encore d'évaluation

- Vehicle Builders Guide v14Document9 pagesVehicle Builders Guide v14georgemesfin@gmailPas encore d'évaluation

- Delivery Challan (Erv) Distributor Details SAP Code 0000170976Document1 pageDelivery Challan (Erv) Distributor Details SAP Code 0000170976vinodPas encore d'évaluation

- Kit Number 15432 Kit Number 15432 Kit Number 15432Document2 pagesKit Number 15432 Kit Number 15432 Kit Number 15432carlosPas encore d'évaluation

- PDFDocument9 pagesPDFkrarPas encore d'évaluation

- Ganesan - Gas Turbines (2010, MC Graw Hill India)Document645 pagesGanesan - Gas Turbines (2010, MC Graw Hill India)Nitish Gupta67% (3)

- Yamaha Vixion Fz150i R15 Parts Catalog PDFDocument28 pagesYamaha Vixion Fz150i R15 Parts Catalog PDFHamizan Mohd Noor0% (1)

- 17071-02 B13R D13C CHN 125761-132856 PDFDocument120 pages17071-02 B13R D13C CHN 125761-132856 PDFAnonymous EDNsviPas encore d'évaluation

- 1VD FTV Engine SpecsDocument4 pages1VD FTV Engine SpecsYannick de Walque0% (1)

- Executive Summary Power PlantDocument10 pagesExecutive Summary Power PlantBISMI1Pas encore d'évaluation