Vous aimerez peut-être aussi

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- AP.2902 - Property-Plant-And-Equipment - With AnswersDocument9 pagesAP.2902 - Property-Plant-And-Equipment - With AnswersEuhanna Karla BacolodPas encore d'évaluation

- AICPA Released Questions AUD 2015 DifficultDocument26 pagesAICPA Released Questions AUD 2015 DifficultTavan ShethPas encore d'évaluation

- Letter of CreditDocument7 pagesLetter of CreditprasadbpotdarPas encore d'évaluation

- Union Bank of India (1) Account Statement PDFDocument2 pagesUnion Bank of India (1) Account Statement PDFJoshua Hannity50% (4)

- World Retail Banking Report 2020 PDFDocument36 pagesWorld Retail Banking Report 2020 PDFBui Hoang Giang100% (1)

- Marketing Head Mumbai 4567Document8 pagesMarketing Head Mumbai 4567Wilfred Dsouza0% (1)

- Investors Perception Towards Investment in Mutual FundsDocument56 pagesInvestors Perception Towards Investment in Mutual Fundstanya dhamija100% (1)

- Name: MJR Invest: Your Current A/C StatusDocument5 pagesName: MJR Invest: Your Current A/C Statusmaakabhawan26Pas encore d'évaluation

- A Study ON "360 Performance Appraisal" Icici Prudential PVT LTDDocument13 pagesA Study ON "360 Performance Appraisal" Icici Prudential PVT LTDbagyaPas encore d'évaluation

- Lala Shanti Swarup Vs Munshi Singh & Ors On 3 January, 1967Document5 pagesLala Shanti Swarup Vs Munshi Singh & Ors On 3 January, 1967Knowledge GuruPas encore d'évaluation

- Asher Rapp BioDocument1 pageAsher Rapp BioarappmemPas encore d'évaluation

- Rsbsa-8 7 2015 PDFDocument4 pagesRsbsa-8 7 2015 PDFRonalene Garbin100% (1)

- Jeevan Arogya PDFDocument47 pagesJeevan Arogya PDFRizwan KhanPas encore d'évaluation

- Standard Chartered BankDocument28 pagesStandard Chartered BankRajni YadavPas encore d'évaluation

- Daily Cashier Report SummaryDocument1 pageDaily Cashier Report SummaryIbox MagPas encore d'évaluation

- Implied Authority of A Partner: A Comparative Study: Assistant Professor of LawDocument20 pagesImplied Authority of A Partner: A Comparative Study: Assistant Professor of LawHimanshuPas encore d'évaluation

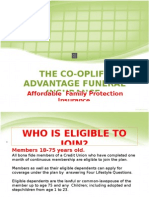

- Barbados Credit Unions Funeral InsuranceDocument12 pagesBarbados Credit Unions Funeral InsuranceKammiePas encore d'évaluation

- DV For MOOEDocument10 pagesDV For MOOELex AmariePas encore d'évaluation

- Sip Report - Bajaj MBADocument49 pagesSip Report - Bajaj MBAGaurav MantalaPas encore d'évaluation

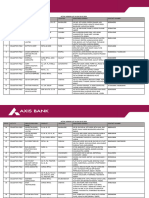

- List of Collection Agencies (1) (2)Document45 pagesList of Collection Agencies (1) (2)cahimanshu1911Pas encore d'évaluation

- Exam Review - Chapters 4, 5, 6: Key Terms and Concepts To KnowDocument21 pagesExam Review - Chapters 4, 5, 6: Key Terms and Concepts To KnowDanica De VeraPas encore d'évaluation

- Ex1 ExportDocument16 pagesEx1 ExportRicha KashyapPas encore d'évaluation

- Customer Satisfaction IndexDocument25 pagesCustomer Satisfaction IndexPrateek DeepPas encore d'évaluation

- Satorp Sukuk Main en Prospectus v.23 Web Final Part1 R6Document316 pagesSatorp Sukuk Main en Prospectus v.23 Web Final Part1 R6jhon ceanPas encore d'évaluation

- Checklist Distribution Agreement SPLDocument3 pagesChecklist Distribution Agreement SPLLitaPas encore d'évaluation

- Property 2015 ExhibitionDocument2 pagesProperty 2015 Exhibitionmanoranjan bagchiPas encore d'évaluation

- FNMA Form 3269-44Document2 pagesFNMA Form 3269-44rapiddocsPas encore d'évaluation

- Dharmendra Pradhan's Declaration of Assets and LiabilitiesDocument9 pagesDharmendra Pradhan's Declaration of Assets and LiabilitiesUday AgarwalPas encore d'évaluation

- Acme Shoe, Rubber and Plastic Corporation v. CA - Scire LicetDocument2 pagesAcme Shoe, Rubber and Plastic Corporation v. CA - Scire LicetRonn PagcoPas encore d'évaluation

- NAFSCOB-Branch OperationsDocument379 pagesNAFSCOB-Branch OperationsAshoak VarmaPas encore d'évaluation