Vous aimerez peut-être aussi

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- MM Inventory ManagementDocument43 pagesMM Inventory Managementjai dPas encore d'évaluation

- Why Is Credit Suisse in Trouble The Banking Turmoil Explained - WSJDocument6 pagesWhy Is Credit Suisse in Trouble The Banking Turmoil Explained - WSJLorindiPas encore d'évaluation

- Texas Court of Appeals Judge District 13 Place 3 Candidate Gregory Thomas Perkes 2010 Ethics FormDocument51 pagesTexas Court of Appeals Judge District 13 Place 3 Candidate Gregory Thomas Perkes 2010 Ethics FormTexas WatchdogPas encore d'évaluation

- Sample ESOP PlanDocument6 pagesSample ESOP PlanAnjali SharmaPas encore d'évaluation

- Causes of Great Depression Thesis StatementDocument7 pagesCauses of Great Depression Thesis Statementmelissajimenezmilwaukee100% (2)

- Investment and Security Law ProjectDocument17 pagesInvestment and Security Law ProjectVAMAXI CHAUHANPas encore d'évaluation

- Indian Stock MarketDocument48 pagesIndian Stock MarketAbhay JainPas encore d'évaluation

- A1238654318 18761 2 2019 Cmaexamsupportpackage201819Document552 pagesA1238654318 18761 2 2019 Cmaexamsupportpackage201819Sahil KumarPas encore d'évaluation

- MK - Dabur India Initiating Coverage - 30 07 08Document10 pagesMK - Dabur India Initiating Coverage - 30 07 08Sukumar SharmaPas encore d'évaluation

- Stop Losses: Help or Hindrance?: Dr. Bruce VanstoneDocument16 pagesStop Losses: Help or Hindrance?: Dr. Bruce VanstoneAleksandrPas encore d'évaluation

- The Efficiency of Financial Ratios Analysis To Evaluate Company'S ProfitabilityDocument15 pagesThe Efficiency of Financial Ratios Analysis To Evaluate Company'S Profitabilityfaizal1229Pas encore d'évaluation

- Finvasia Client Guidance NSE BSE 2016Document18 pagesFinvasia Client Guidance NSE BSE 2016tommyPas encore d'évaluation

- Economics Notes PDFDocument15 pagesEconomics Notes PDFEstherPas encore d'évaluation

- Securities Regulation Code NOTESDocument6 pagesSecurities Regulation Code NOTESLyka Rose MahamudPas encore d'évaluation

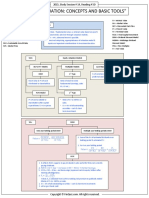

- Smart Summary Equity Valuation Concepts and Basic Tools CFADocument4 pagesSmart Summary Equity Valuation Concepts and Basic Tools CFABhuvnesh KotharPas encore d'évaluation

- Ch19 Performance Evaluation and Active Portfolio ManagementDocument29 pagesCh19 Performance Evaluation and Active Portfolio ManagementA_StudentsPas encore d'évaluation

- Jagoinvestor Ebook 15 BestDocument143 pagesJagoinvestor Ebook 15 BestjvgediyaPas encore d'évaluation

- UntitledDocument18 pagesUntitledAlok TiwariPas encore d'évaluation

- BSE 17062019162527 NSEintimationAnnualreport 249Document313 pagesBSE 17062019162527 NSEintimationAnnualreport 249projectboyPas encore d'évaluation

- Money TimesDocument21 pagesMoney Timesnageshwar raoPas encore d'évaluation

- Financial Management:: Getting Started - Principles of FinanceDocument41 pagesFinancial Management:: Getting Started - Principles of FinanceiqbalPas encore d'évaluation

- A Project Report On " " Working of Stock Exchange (Fullerton As A Depository) ParticipantDocument23 pagesA Project Report On " " Working of Stock Exchange (Fullerton As A Depository) ParticipantPriyanka GroverPas encore d'évaluation

- Litton v. Hill & Ceron - 1939Document7 pagesLitton v. Hill & Ceron - 1939Eugene RoxasPas encore d'évaluation

- Financial Management - Stock Valuation Assignment 2 - Abdullah Bin Amir - Section ADocument3 pagesFinancial Management - Stock Valuation Assignment 2 - Abdullah Bin Amir - Section AAbdullah AmirPas encore d'évaluation

- Does Stock Split Influence To Liquidity and Stock ReturnDocument9 pagesDoes Stock Split Influence To Liquidity and Stock ReturnBhavdeepsinh JadejaPas encore d'évaluation

- GROSS INCOME - InclusionDocument8 pagesGROSS INCOME - InclusionNessa Mae Leaño JamolinPas encore d'évaluation

- OTCEIDocument11 pagesOTCEIvisa_kpPas encore d'évaluation

- Litwin v. AllenDocument3 pagesLitwin v. AllenAnonymous 5MiN6I78I0Pas encore d'évaluation