Vous aimerez peut-être aussi

- VO Chidambaram: The Romance of Resistance - Open The MagazineDocument1 pageVO Chidambaram: The Romance of Resistance - Open The Magazinerangak2004Pas encore d'évaluation

- Scientists Baffled by Ancient Carvings of Civilisation That Invented The Toilet - Daily Mail OnlineDocument15 pagesScientists Baffled by Ancient Carvings of Civilisation That Invented The Toilet - Daily Mail Onlinerangak2004Pas encore d'évaluation

- Urban Catalyst Buys Third Downtown San Jose Property For $600M 2-Tower Project - Silicon Valley Business JournalDocument2 pagesUrban Catalyst Buys Third Downtown San Jose Property For $600M 2-Tower Project - Silicon Valley Business Journalrangak2004Pas encore d'évaluation

- Direct Project OverviewDocument14 pagesDirect Project OverviewmariomittePas encore d'évaluation

- Surface-Enhanced Cantilever Sensors with Nano-Porous FilmsDocument12 pagesSurface-Enhanced Cantilever Sensors with Nano-Porous Filmsrangak2004Pas encore d'évaluation

- 10 Ways Past Secure Boot v1.0 JVW ShakaconDocument27 pages10 Ways Past Secure Boot v1.0 JVW Shakaconrangak2004Pas encore d'évaluation

- Free Banking in England Lawarence WhiteDocument194 pagesFree Banking in England Lawarence WhiteUploaded By: Ann O'Ryan SpeharPas encore d'évaluation

- Cat Hay ConditionsDocument5 pagesCat Hay Conditionsrangak2004Pas encore d'évaluation

- Gold Commission Report Annex CDocument6 pagesGold Commission Report Annex Crangak2004Pas encore d'évaluation

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Payment ExternalCodeLists 16august10 v4Document36 pagesPayment ExternalCodeLists 16august10 v4DcStrokerehabPas encore d'évaluation

- Economics Club: Article Series - 7Document4 pagesEconomics Club: Article Series - 7Anshul AgrawalPas encore d'évaluation

- Exchange Rate PracticeDocument3 pagesExchange Rate PracticeRajesh KayiprathPas encore d'évaluation

- Work Experience Verification TemplateDocument17 pagesWork Experience Verification TemplateUSHA RANIPas encore d'évaluation

- History of EmuDocument21 pagesHistory of EmumeettotalkPas encore d'évaluation

- Why Is The BSP The Main Government Agency Responsible For Promoting Price StabilityDocument4 pagesWhy Is The BSP The Main Government Agency Responsible For Promoting Price StabilityMarielle CatiisPas encore d'évaluation

- AP Macroeconomics: Sample Student Responses and Scoring CommentaryDocument6 pagesAP Macroeconomics: Sample Student Responses and Scoring CommentaryDion Masayon BanquiaoPas encore d'évaluation

- Rekening Terpisah PT BPF PDFDocument1 pageRekening Terpisah PT BPF PDFDebbi FitrianiPas encore d'évaluation

- Russian RubleDocument13 pagesRussian RubleArjunPas encore d'évaluation

- Forecasting Usd - Euro Ex Rates Using ARMA ModelDocument13 pagesForecasting Usd - Euro Ex Rates Using ARMA ModelNavin Poddar100% (1)

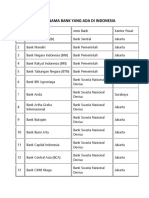

- List of Indonesian BanksDocument10 pagesList of Indonesian Bankswinni winPas encore d'évaluation

- EcbDocument210 pagesEcbhnkyPas encore d'évaluation

- Bank Data MasterDocument288 pagesBank Data MasterDallasPas encore d'évaluation

- Poi & PoaDocument14 pagesPoi & PoaKoundinyasa NishanthPas encore d'évaluation

- Gold As A Foreign Exchange Reserve of Central BanksDocument8 pagesGold As A Foreign Exchange Reserve of Central BanksMikiKikiPas encore d'évaluation

- RBI Master Circular on Facility for Exchange of Notes and CoinsDocument8 pagesRBI Master Circular on Facility for Exchange of Notes and CoinsadswerPas encore d'évaluation

- Modelling and Trading The EUR/USD Exchange Rate at The ECB FixingDocument25 pagesModelling and Trading The EUR/USD Exchange Rate at The ECB FixingSergio Santos VillamilPas encore d'évaluation

- T T-8-2-87-10-185-Chukwu-D-O-TtDocument15 pagesT T-8-2-87-10-185-Chukwu-D-O-TtGodspower UhuabaPas encore d'évaluation

- B - B - A - (Banking) 122 13 Banking Theory Juhb PDFDocument254 pagesB - B - A - (Banking) 122 13 Banking Theory Juhb PDFGargi MehrotraPas encore d'évaluation

- Certificate of Compliance With The Order 2.1 According To EN 10 204Document1 pageCertificate of Compliance With The Order 2.1 According To EN 10 204bebePas encore d'évaluation

- Sphinx Extract PRADocument1 362 pagesSphinx Extract PRAsomenathbasakPas encore d'évaluation

- Seylan Bank's 'The Case Study', A Fine Example of Financial ReportingDocument1 pageSeylan Bank's 'The Case Study', A Fine Example of Financial ReportingSmart Media - The Annual Report CompanyPas encore d'évaluation

- JDEdwards Manual - Euro ConversionDocument232 pagesJDEdwards Manual - Euro Conversionssanik1Pas encore d'évaluation

- Permatame: Mutasi TransaksiDocument6 pagesPermatame: Mutasi Transaksitrans duitPas encore d'évaluation

- The Perfect StormDocument41 pagesThe Perfect StormNickKr100% (1)

- Central Bank Balance Sheet Money SupplyDocument37 pagesCentral Bank Balance Sheet Money SupplyIzzy Cohn0% (1)

- 0B35JGQahqjmJNmdrcWdFd0FjSFE PDFDocument16 pages0B35JGQahqjmJNmdrcWdFd0FjSFE PDFPriyaSriPas encore d'évaluation

- Macroeconomics Discussion4Document2 pagesMacroeconomics Discussion4Chia Chia KoayPas encore d'évaluation

- Books by Dr. H N S KarunatillakeDocument2 pagesBooks by Dr. H N S KarunatillakeH L S ChandrajithPas encore d'évaluation

- Al Hadi Et Al. (2017)Document45 pagesAl Hadi Et Al. (2017)Sharif Ullah JanPas encore d'évaluation