Vous aimerez peut-être aussi

- Mirror Wills LeafletDocument8 pagesMirror Wills LeafletDeepak HingoraniPas encore d'évaluation

- W4 Wills & Estates 2Document16 pagesW4 Wills & Estates 2Iulii IuliikkPas encore d'évaluation

- Tutorial 3 Intestate Succession Calculations ExplainedDocument11 pagesTutorial 3 Intestate Succession Calculations ExplainedThabiso MathobelaPas encore d'évaluation

- Chapter 2 Part 3Document21 pagesChapter 2 Part 3ZanelePas encore d'évaluation

- Law of Succession Exam QuestionsDocument2 pagesLaw of Succession Exam QuestionsfabiolabeukesPas encore d'évaluation

- Pace Lex Et Sapientia: LegitimeDocument3 pagesPace Lex Et Sapientia: LegitimeHarriette Legaspi LabradaPas encore d'évaluation

- Introduction To Family LawDocument31 pagesIntroduction To Family LawcarolynPas encore d'évaluation

- Law of Succession Assignment 1Document16 pagesLaw of Succession Assignment 1Teofelus AndjenePas encore d'évaluation

- The Chartered Institute of Legal Executives Unit 14 - Probate Practice Case Study MaterialsDocument8 pagesThe Chartered Institute of Legal Executives Unit 14 - Probate Practice Case Study MaterialsantcbePas encore d'évaluation

- Tutoral 1 Family LawDocument6 pagesTutoral 1 Family LawMAISARA MOHD AMRANPas encore d'évaluation

- Slide 5Document34 pagesSlide 5Aisyah AnuarPas encore d'évaluation

- Islamic Will Kit AuatraliaDocument15 pagesIslamic Will Kit AuatraliaLegacy Gaming27Pas encore d'évaluation

- P6 RN - Residency & DomicileDocument3 pagesP6 RN - Residency & DomicileHuda AkramPas encore d'évaluation

- Property Rights Under Muslim Personal LawDocument31 pagesProperty Rights Under Muslim Personal LawMadivalappa MatolliPas encore d'évaluation

- Refugees Welcome In The UK: Hosting & Resettlement The Advantages & Disadvantages Of Hosting A Refugee Family Living In Your HomeD'EverandRefugees Welcome In The UK: Hosting & Resettlement The Advantages & Disadvantages Of Hosting A Refugee Family Living In Your HomePas encore d'évaluation

- Q4 Sheffield Investment BrochureDocument9 pagesQ4 Sheffield Investment BrochureMark I'AnsonPas encore d'évaluation

- Mus - Law SharesDocument58 pagesMus - Law SharesKiran kumarPas encore d'évaluation

- 1st Lecture INTESTATE SUCCESSION RULES - ARDocument23 pages1st Lecture INTESTATE SUCCESSION RULES - ARSteve KennedyPas encore d'évaluation

- Week 10 05122022 101242amDocument19 pagesWeek 10 05122022 101242amJehanzaib AminPas encore d'évaluation

- 10gfghhj OdtDocument3 pages10gfghhj OdtAkhila FrancisPas encore d'évaluation

- The Great Divide: Australia's Housing Mess and How to Fix It; Quarterly Essay 92D'EverandThe Great Divide: Australia's Housing Mess and How to Fix It; Quarterly Essay 92Pas encore d'évaluation

- Notes On Succession Under The Succession ActDocument3 pagesNotes On Succession Under The Succession Actkenny mbakhwaPas encore d'évaluation

- Keeping It in The Family PDFDocument12 pagesKeeping It in The Family PDFchsinclairPas encore d'évaluation

- 3 Bed House - KA18Document11 pages3 Bed House - KA18Mark I'AnsonPas encore d'évaluation

- Civil Law Review Lecture and Recitation NotesDocument36 pagesCivil Law Review Lecture and Recitation Notesekayekay14Pas encore d'évaluation

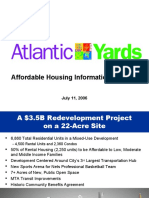

- Affordable Housing PowerPointDocument16 pagesAffordable Housing PowerPointNorman OderPas encore d'évaluation

- Guide RN - Oct 2023Document9 pagesGuide RN - Oct 2023Anver RassipPas encore d'évaluation

- DomicileDocument32 pagesDomicileNimrah Rehman SabiriPas encore d'évaluation

- Table of LegitimesDocument6 pagesTable of LegitimesRowena GallegoPas encore d'évaluation

- Suit For Dissolution of MarriageDocument5 pagesSuit For Dissolution of Marriagenabia lodhiPas encore d'évaluation

- Succession Short Reviewer On LegitimesDocument1 pageSuccession Short Reviewer On LegitimesDeborah StewartPas encore d'évaluation

- Pre Assessment Check List - June 2013 PDFDocument1 pagePre Assessment Check List - June 2013 PDFBishar OmarPas encore d'évaluation

- GraduationDocument42 pagesGraduationapi-356200913Pas encore d'évaluation

- Women, marriage and property in wealthy landed families in Ireland, 1750–1850D'EverandWomen, marriage and property in wealthy landed families in Ireland, 1750–1850Pas encore d'évaluation

- Property Investment Brochure - KA11Document9 pagesProperty Investment Brochure - KA11Mark I'AnsonPas encore d'évaluation

- Nortons Cottage: Albourne West SussexDocument4 pagesNortons Cottage: Albourne West SussexaskdljlasdjlkjPas encore d'évaluation

- Order of Intestate SuccessionDocument3 pagesOrder of Intestate Successiondiyesa100% (2)

- Marriage: in ScotlandDocument20 pagesMarriage: in Scotlandtcarpi2741Pas encore d'évaluation

- Variable and Invariable Consequences of MarriageDocument10 pagesVariable and Invariable Consequences of MarriageTeboho Tebu MofokengPas encore d'évaluation

- Estate Planning Utk PresentDocument60 pagesEstate Planning Utk PresentNur Aqilah JailaniPas encore d'évaluation

- Xtra Question Intestate Calculation ANSWER IS WRONG! SEE MY COMMENTSDocument5 pagesXtra Question Intestate Calculation ANSWER IS WRONG! SEE MY COMMENTSAyandaPas encore d'évaluation

- Legally Avoid Property Taxes: 51 Top Tips to Save Property Taxes and Increase Your WealthD'EverandLegally Avoid Property Taxes: 51 Top Tips to Save Property Taxes and Increase Your WealthPas encore d'évaluation

- Problem 8 & 9 Estate Tax: Married Decedents: Caraig Dela Cruz TanDocument12 pagesProblem 8 & 9 Estate Tax: Married Decedents: Caraig Dela Cruz TanmikaelaPas encore d'évaluation

- Case Study 4Document3 pagesCase Study 4JorgePas encore d'évaluation

- Press Release: Embargoed UntilDocument7 pagesPress Release: Embargoed UntilEmpty HomesPas encore d'évaluation

- Rm1 Leaflet RevisedDocument6 pagesRm1 Leaflet RevisedNadine Bär-SchmitzPas encore d'évaluation

- 67,500 Equity BrochureDocument8 pages67,500 Equity BrochureMark I'AnsonPas encore d'évaluation

- Wills Outline Summer 2007: Body of Law in NY Governing Wills & EstatesDocument42 pagesWills Outline Summer 2007: Body of Law in NY Governing Wills & EstatesSiddoPas encore d'évaluation

- 01 - Transfer and Business Tax - IntroductionDocument20 pages01 - Transfer and Business Tax - IntroductionGJ MendozaPas encore d'évaluation

- InheritanceDocument31 pagesInheritanceAusama MemonPas encore d'évaluation

- Muslim Law of InheritanceDocument4 pagesMuslim Law of Inheritanceanon_59359966Pas encore d'évaluation

- Gross Estate of Married DecedentDocument10 pagesGross Estate of Married Decedentbeverlyrtan85% (13)

- UK-Sponsorship-Information - Charitypeople - Co.ukDocument6 pagesUK-Sponsorship-Information - Charitypeople - Co.ukthaisalmeidalinda18Pas encore d'évaluation

- Tables of LegitimesDocument2 pagesTables of LegitimesagnatgaPas encore d'évaluation

- Loc019 EngDocument3 pagesLoc019 Engloulouche165Pas encore d'évaluation

- Understanding & Calculating Zaka H: Upda TED VER SionDocument16 pagesUnderstanding & Calculating Zaka H: Upda TED VER SionkhalidJMPas encore d'évaluation

- Legitime in Testate Succession: Mortis (Time of Death)Document6 pagesLegitime in Testate Succession: Mortis (Time of Death)No MercyPas encore d'évaluation

- Intestacy Laws Flow Chart: Are You Married or in A Civil Partnership?Document1 pageIntestacy Laws Flow Chart: Are You Married or in A Civil Partnership?StorrsWillsPas encore d'évaluation

- Understand The Rules of Intestacy UpdatedDocument2 pagesUnderstand The Rules of Intestacy UpdatedwestintaPas encore d'évaluation

- Customs of TagalogDocument20 pagesCustoms of TagalogKyubi Nine50% (2)

- Director 1Document64 pagesDirector 1Manoj Kumar MohanPas encore d'évaluation

- But It Is An Emergency. Carl Schmitt, John Locke and The Paradox of Prerogative - Douglas CassonDocument30 pagesBut It Is An Emergency. Carl Schmitt, John Locke and The Paradox of Prerogative - Douglas CassonAnonymous eDvzmvPas encore d'évaluation

- 003 UCC Insurance Vacation Interest Policy (UCC01-NP Rev.07-01-14) PDFDocument7 pages003 UCC Insurance Vacation Interest Policy (UCC01-NP Rev.07-01-14) PDFGerardo Enrique AlfonsoPas encore d'évaluation

- Cadiente vs. MacasDocument7 pagesCadiente vs. MacasNeriz RecintoPas encore d'évaluation

- Civil Law DoctrinesDocument21 pagesCivil Law DoctrinesAngela B. LumabasPas encore d'évaluation

- Domicile of Corporations and Pseudo CorporationsDocument20 pagesDomicile of Corporations and Pseudo CorporationsAnkur Gupta50% (2)

- Lozano Law OfficeDocument6 pagesLozano Law OfficeArcide Rcd ReynilPas encore d'évaluation

- Tagatac v. JimenezDocument5 pagesTagatac v. JimenezKimmyPas encore d'évaluation

- Law and Justice in A Globalised WorldDocument26 pagesLaw and Justice in A Globalised WorldShivam KumarPas encore d'évaluation

- Lagman v. Medialdea - Carpio Dissent DigestDocument4 pagesLagman v. Medialdea - Carpio Dissent DigestCathy Alcantara100% (1)

- Parliamentary Procedure Cheat SheetDocument2 pagesParliamentary Procedure Cheat SheetBrycen Nardone100% (3)

- People vs. Ramos, 122 SCRA 312, No. L-59318, May 16, 1983philippine Law CasesDocument2 pagesPeople vs. Ramos, 122 SCRA 312, No. L-59318, May 16, 1983philippine Law CasesJetJuárezPas encore d'évaluation

- The Case For Torture - Michael LevinDocument2 pagesThe Case For Torture - Michael LevinDylan StovallPas encore d'évaluation

- U.S. v. Michael T. Flynn: Plea AgreementDocument10 pagesU.S. v. Michael T. Flynn: Plea AgreementPete Madden100% (1)

- Department of Education: Daily Accomplishment ReportDocument10 pagesDepartment of Education: Daily Accomplishment ReportMirasolLynneCenabre-QuilangObsiomaPas encore d'évaluation

- High Commission of India: Visa Application FormDocument2 pagesHigh Commission of India: Visa Application FormShuhan Mohammad Ariful HoquePas encore d'évaluation

- Ex Parte Application To Freeze of Assets Consumer Rights Action Against Mazgani Social Services Mahvash Nazanin NeyazDocument43 pagesEx Parte Application To Freeze of Assets Consumer Rights Action Against Mazgani Social Services Mahvash Nazanin Neyazkevin67% (3)

- 102) People of The Philippines vs. Jumauan (722 SCRA 108)Document51 pages102) People of The Philippines vs. Jumauan (722 SCRA 108)Carmel Grace KiwasPas encore d'évaluation

- OAS Charter 1948Document24 pagesOAS Charter 1948Guillermo MurguiaPas encore d'évaluation

- ADR Chapter 4 PresentationDocument28 pagesADR Chapter 4 PresentationGustavo Fernandez DalenPas encore d'évaluation

- Obligations and Contracts Prelim ReviewerDocument4 pagesObligations and Contracts Prelim ReviewerMarcus AspacioPas encore d'évaluation

- Arbitration Status - Sept 2020Document3 pagesArbitration Status - Sept 2020Dipak PatelPas encore d'évaluation

- Lesson 1 Unit 1 - SalamatDocument1 pageLesson 1 Unit 1 - SalamatandreagassiPas encore d'évaluation

- Candano vs. Sugata-OnDocument2 pagesCandano vs. Sugata-OnAr LinePas encore d'évaluation

- Novice MemorialDocument11 pagesNovice MemorialAKANKSHYA BHATTACHARJEEPas encore d'évaluation

- Jeff Epstein Notes PDFDocument2 pagesJeff Epstein Notes PDFAnonymous SjL2rOwHan73% (11)

- West Africa Center For Peace StudiesDocument7 pagesWest Africa Center For Peace Studiestecnalite expertsPas encore d'évaluation

- Case For PracticumDocument11 pagesCase For Practicumwjap3Pas encore d'évaluation

- NDA Draft General-1Document7 pagesNDA Draft General-1Adi TPas encore d'évaluation

- Gonzales v. Office of The President GR No. 196231 Sept 4 2012Document47 pagesGonzales v. Office of The President GR No. 196231 Sept 4 2012wenny capplemanPas encore d'évaluation