Vous aimerez peut-être aussi

- IRS Forms and InstructionsDocument133 pagesIRS Forms and InstructionsMaster100% (4)

- Earnings Statement: Non-NegotiableDocument1 pageEarnings Statement: Non-NegotiableAyanna Sellers100% (5)

- Form 941 SummaryDocument5 pagesForm 941 SummaryCatori-Dakoda Eil100% (1)

- Introduction Letter - 3.4.21Document2 pagesIntroduction Letter - 3.4.21Gunjan PatelPas encore d'évaluation

- Companies ListDocument293 pagesCompanies ListKishor Kumar100% (1)

- IMA List of Company Members in Indonesia's Mining SectorDocument32 pagesIMA List of Company Members in Indonesia's Mining SectorArdhymanto Am. TanjungPas encore d'évaluation

- 2019 BAR EXAM TAXATION LAW REVIEWDocument9 pages2019 BAR EXAM TAXATION LAW REVIEWzealous9carrotPas encore d'évaluation

- Minaral and MetalDocument109 pagesMinaral and Metaldeva nesan100% (1)

- 6 Basic Employee Benefits in The PhilippinesDocument7 pages6 Basic Employee Benefits in The PhilippinesgeLO36Pas encore d'évaluation

- AP To TGDocument1 665 pagesAP To TGPavan TejaPas encore d'évaluation

- Thailand - PESTLE AnalysisDocument80 pagesThailand - PESTLE Analysisesteban trueba84% (25)

- FABM2 Q2 Mod13Document29 pagesFABM2 Q2 Mod13Fretty Mae Abubo100% (3)

- Pwcid Company Profile 2018Document28 pagesPwcid Company Profile 2018Kerja Sama KSPPas encore d'évaluation

- JSW Steel InfoDocument3 pagesJSW Steel InfoHiren PatelPas encore d'évaluation

- Plantation Companies ListDocument179 pagesPlantation Companies ListImage TubePas encore d'évaluation

- Delegate List - 10th IMRC With Contact Details - Removed (1) - Removed (1) - Removed (1) - RemovedDocument100 pagesDelegate List - 10th IMRC With Contact Details - Removed (1) - Removed (1) - Removed (1) - RemovedSharon SusmithaPas encore d'évaluation

- Eir - November2016Document1 372 pagesEir - November2016AbhishekPas encore d'évaluation

- Final Updated Contractor List As On Sep 19Document25 pagesFinal Updated Contractor List As On Sep 19Vishal JiyaniPas encore d'évaluation

- Top 51 Indian Companies Contact List with Address and Phone NumbersDocument5 pagesTop 51 Indian Companies Contact List with Address and Phone NumbersSwati SinghPas encore d'évaluation

- 2017 Presentation03 HandaDocument21 pages2017 Presentation03 HandasatyaseerPas encore d'évaluation

- FCI e-auction results from Jan 2018-Sept 2020Document5 pagesFCI e-auction results from Jan 2018-Sept 2020AvijitSinharoyPas encore d'évaluation

- Oil Country Tubular LimitedDocument2 pagesOil Country Tubular LimitedVineeth TejPas encore d'évaluation

- SEO-optimized title for document containing company contact detailsDocument11 pagesSEO-optimized title for document containing company contact detailsCharles BinuPas encore d'évaluation

- ExpoStone 2013 Exhibitor ListDocument18 pagesExpoStone 2013 Exhibitor ListKen EdwardPas encore d'évaluation

- GTTI connects tooling institutes with industriesDocument12 pagesGTTI connects tooling institutes with industriessansagithPas encore d'évaluation

- Updated SI Empanelment List 23022012Document2 pagesUpdated SI Empanelment List 23022012Vijay KumarPas encore d'évaluation

- RFQ-CP - November 2017Document12 pagesRFQ-CP - November 2017KshirabdhiTanayaSwainPas encore d'évaluation

- Delegate List - 10th IMRC With Contact Details - Removed (1) - Removed (1) - RemovedDocument100 pagesDelegate List - 10th IMRC With Contact Details - Removed (1) - Removed (1) - RemovedSharon SusmithaPas encore d'évaluation

- Name of Lessee Registration Number Mine - Code Email Id of The Owner/lesseeDocument3 pagesName of Lessee Registration Number Mine - Code Email Id of The Owner/lesseeKapil RampalPas encore d'évaluation

- Ssc-Jaa SpocDocument6 pagesSsc-Jaa SpocSai Teja NarsingojuPas encore d'évaluation

- MIDC IndustryDocument15 pagesMIDC Industrynikhil indoreinfolinePas encore d'évaluation

- Inquiry&EmaillistDocument13 pagesInquiry&EmaillistGunjan PatelPas encore d'évaluation

- Vendor PDFDocument189 pagesVendor PDFSandeep YadavPas encore d'évaluation

- Resource DirectoryDocument38 pagesResource DirectoryhareshPas encore d'évaluation

- Revised Final Allotment-17.06.2019... Pulses Importers List June 2019. 10.12.2019 PDFDocument222 pagesRevised Final Allotment-17.06.2019... Pulses Importers List June 2019. 10.12.2019 PDFsureshPas encore d'évaluation

- BookDocument44 pagesBookBinay ShawPas encore d'évaluation

- Dealer and Village Listing in Coimbatore DistrictDocument9 pagesDealer and Village Listing in Coimbatore DistrictgayathriPas encore d'évaluation

- HK Show ParticipentDocument57 pagesHK Show ParticipentAnonymous 2xtnzo100% (2)

- Directory 2007 WebDocument185 pagesDirectory 2007 WebprecastengineeringPas encore d'évaluation

- To Be Uploaded ListDocument10 pagesTo Be Uploaded ListAshish BhuvanPas encore d'évaluation

- Approved List of Firms for Manufacture and Supply of Electrical Signalling and Telecommunication ItemsDocument195 pagesApproved List of Firms for Manufacture and Supply of Electrical Signalling and Telecommunication ItemsMukul Kumar AgarwalPas encore d'évaluation

- EXHIBITOR LISTINGDocument117 pagesEXHIBITOR LISTINGLakshanmayaPas encore d'évaluation

- List 5 Approved Manufacturers of Iron Castings: As at 06 November 2012Document36 pagesList 5 Approved Manufacturers of Iron Castings: As at 06 November 2012wyvren88Pas encore d'évaluation

- Mobile India Expo BrochureDocument2 pagesMobile India Expo BrochureĀr Fåîzâl RähmåñPas encore d'évaluation

- Solar EDPDocument3 pagesSolar EDPGokulPas encore d'évaluation

- Eir December2017Document1 137 pagesEir December2017AbhishekPas encore d'évaluation

- Latest Title Deed ProposalNote 5371Document82 pagesLatest Title Deed ProposalNote 5371pranayvigPas encore d'évaluation

- Vendor List Defence ProductionDocument340 pagesVendor List Defence ProductionVinay SimhaPas encore d'évaluation

- Drugs Pharma Conference Karnataka Growth InnovationDocument2 pagesDrugs Pharma Conference Karnataka Growth InnovationRavindra T MakuntePas encore d'évaluation

- Automation 2013 Exhibitor ListDocument14 pagesAutomation 2013 Exhibitor Listscribdbesolutions0% (1)

- Fmai 5 PDFDocument53 pagesFmai 5 PDFvenkatesh_1829Pas encore d'évaluation

- List of Certified Manufacturer'S Under "Tested Product Certificate (TPC) " CategoryDocument4 pagesList of Certified Manufacturer'S Under "Tested Product Certificate (TPC) " CategoryArvind DharmarajPas encore d'évaluation

- Berger Paints India Limited PDFDocument37 pagesBerger Paints India Limited PDFSahil GargPas encore d'évaluation

- Overdue Payment Issue from NOCLDocument6 pagesOverdue Payment Issue from NOCLMohan RajPas encore d'évaluation

- 77922Document6 pages77922praneethrk53Pas encore d'évaluation

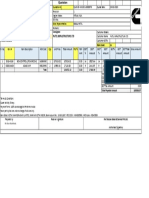

- Cummins 380KVA QuotationDocument1 pageCummins 380KVA QuotationabhibawaPas encore d'évaluation

- EHS Approved Green Building ConsultantsDocument2 pagesEHS Approved Green Building Consultantstp101267Pas encore d'évaluation

- Government of India accredited solar installersDocument20 pagesGovernment of India accredited solar installersarvindPas encore d'évaluation

- Chittoor District PDFDocument35 pagesChittoor District PDFSuresh Kumar100% (1)

- Group Company ListDocument12 pagesGroup Company ListsigmasundarPas encore d'évaluation

- AutoDocument15 pagesAutoprashanthkmPas encore d'évaluation

- Registered Alternative Investment Funds as of Nov 2016Document31 pagesRegistered Alternative Investment Funds as of Nov 2016bbdelhiPas encore d'évaluation

- CopyDocument2 pagesCopyRohitSalunkhePas encore d'évaluation

- Vendor Directory - 1stjuly - 31stdecember PDFDocument269 pagesVendor Directory - 1stjuly - 31stdecember PDFJaay VelPas encore d'évaluation

- Portrait of an Industrial City: 'Clanging Belfast' 1750-1914D'EverandPortrait of an Industrial City: 'Clanging Belfast' 1750-1914Pas encore d'évaluation

- Taxflash 2023 06Document3 pagesTaxflash 2023 06yaranami channelPas encore d'évaluation

- Taxflash 2023 02Document3 pagesTaxflash 2023 02Kasuma YeniPas encore d'évaluation

- Tax Invoice Dwaraka N: Dec, 2021 20/12/2021 906.9 Immediate 1,006.9Document2 pagesTax Invoice Dwaraka N: Dec, 2021 20/12/2021 906.9 Immediate 1,006.9Dwaraka PillaiPas encore d'évaluation

- Solved Paper FSD-2010Document11 pagesSolved Paper FSD-2010Kiran SoniPas encore d'évaluation

- MonthlyPaySlip 2023 07 17T08 47 05Document1 pageMonthlyPaySlip 2023 07 17T08 47 05Prosenjit MondalPas encore d'évaluation

- TDS Challan FormDocument1 pageTDS Challan FormVipin Kumar ChandelPas encore d'évaluation

- IBMI US State Tax Withholding FormDocument1 pageIBMI US State Tax Withholding FormDillipsahu14Pas encore d'évaluation

- Set Off & Carry Forward of LossesDocument21 pagesSet Off & Carry Forward of LossesanchalPas encore d'évaluation

- GSTR 3B Excel FormatDocument2 pagesGSTR 3B Excel Formatravibhartia1978Pas encore d'évaluation

- Tax Invoice: Smart Lifts & ElectricalsDocument1 pageTax Invoice: Smart Lifts & ElectricalsYours PharmacyPas encore d'évaluation

- CPAR Tax On Estates and Trusts (Batch 92) - HandoutDocument10 pagesCPAR Tax On Estates and Trusts (Batch 92) - HandoutNikkoPas encore d'évaluation

- PR 11 2016Document28 pagesPR 11 2016Ken ChiaPas encore d'évaluation

- CanonsDocument2 pagesCanonsonprocessPas encore d'évaluation

- 3229 To 3233 Dollar Industries LimitedDocument2 pages3229 To 3233 Dollar Industries LimitedmanjujeejooPas encore d'évaluation

- Torres Ma. Deidre Yciar L - Chapter 13 ADocument5 pagesTorres Ma. Deidre Yciar L - Chapter 13 AAriana Marie ArandiaPas encore d'évaluation

- Estate Tax ReportDocument4 pagesEstate Tax ReportMAICA SELGUERAPas encore d'évaluation

- m02 Government Budget and The EconomyDocument17 pagesm02 Government Budget and The EconomyAman patidarPas encore d'évaluation

- Salary Certificate Format Bank Loan GuideDocument2 pagesSalary Certificate Format Bank Loan GuideAjey Kulkarni100% (1)

- Batangas State University College of Accountancy QuizDocument5 pagesBatangas State University College of Accountancy QuizBABY JOY SEGUIPas encore d'évaluation

- Assignment No. 1 - The Budget ProcessDocument4 pagesAssignment No. 1 - The Budget ProcessCindy Faye CrusantePas encore d'évaluation

- Deloitte Guide To Fiscal Information Africa2015Document390 pagesDeloitte Guide To Fiscal Information Africa2015marco potoPas encore d'évaluation

- Juixs Floyd Morpheus Manalo: Tax Code: S Attendance Period Payroll Period Release DateDocument1 pageJuixs Floyd Morpheus Manalo: Tax Code: S Attendance Period Payroll Period Release DateFLOYD MORPHEUSPas encore d'évaluation

- Chapter 1 MCQs On Income Tax Rates and Basic Concept of Income TaxDocument28 pagesChapter 1 MCQs On Income Tax Rates and Basic Concept of Income TaxMeenal Luther100% (1)

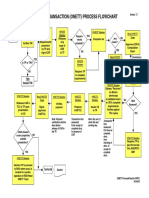

- One-Time Transaction (Onett) Process Flowchart: StartDocument1 pageOne-Time Transaction (Onett) Process Flowchart: StartJenely Joy Areola-TelanPas encore d'évaluation

- Omio Invoice D3ZZRHDocument2 pagesOmio Invoice D3ZZRHyalu.liu.proPas encore d'évaluation