Vous aimerez peut-être aussi

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- Mobileaware Banking Brief PDFDocument3 pagesMobileaware Banking Brief PDFThach NgoPas encore d'évaluation

- ANB Financial in VARBusiness PDFDocument3 pagesANB Financial in VARBusiness PDFThach NgoPas encore d'évaluation

- Astaro Email Security Datasheet Us PDFDocument2 pagesAstaro Email Security Datasheet Us PDFThach NgoPas encore d'évaluation

- Mutt GPG PDFDocument11 pagesMutt GPG PDFThach NgoPas encore d'évaluation

- Mwri - Annual Research Banking Review 2010 08 PDFDocument16 pagesMwri - Annual Research Banking Review 2010 08 PDFThach NgoPas encore d'évaluation

- Belgacom E-Mail Security en PDFDocument2 pagesBelgacom E-Mail Security en PDFThach NgoPas encore d'évaluation

- Network Security: Sasikumar Gurumurthy, Member, IAENGDocument5 pagesNetwork Security: Sasikumar Gurumurthy, Member, IAENGThach NgoPas encore d'évaluation

- ProtectingVM PDFDocument3 pagesProtectingVM PDFThach NgoPas encore d'évaluation

- ENBR0810 CORPORATE S PDFDocument12 pagesENBR0810 CORPORATE S PDFThach NgoPas encore d'évaluation

- E-Mail Security For The 21 CenturyDocument10 pagesE-Mail Security For The 21 CenturyThach NgoPas encore d'évaluation

- SMIME Slides PDFDocument8 pagesSMIME Slides PDFThach NgoPas encore d'évaluation

- CPM Group PDFDocument14 pagesCPM Group PDFThach NgoPas encore d'évaluation

- Afghanistan Bankingservices PDFDocument5 pagesAfghanistan Bankingservices PDFThach NgoPas encore d'évaluation

- Protecting Your Business From Online Banking Fraud: Robert Comella, Greg Farnham, John Jarocki October 2009Document13 pagesProtecting Your Business From Online Banking Fraud: Robert Comella, Greg Farnham, John Jarocki October 2009Thach NgoPas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Lesson 1 and 2 Summary On LANGUAGE, CULTURE & SOCIETYDocument4 pagesLesson 1 and 2 Summary On LANGUAGE, CULTURE & SOCIETYJasper RoquePas encore d'évaluation

- Manotoc Vs CADocument1 pageManotoc Vs CAGheeness Gerald Macadangdang MacaraigPas encore d'évaluation

- What Female Bodybuilding Workout Plans Are Like: Build Impressive MusclesDocument3 pagesWhat Female Bodybuilding Workout Plans Are Like: Build Impressive MusclesKunal jainPas encore d'évaluation

- OTC Interview Evaluation Sheet - Saumya PradhanDocument2 pagesOTC Interview Evaluation Sheet - Saumya PradhanVikky VikramPas encore d'évaluation

- Edgar Payne - Composition of Outdoor Painting PDFDocument187 pagesEdgar Payne - Composition of Outdoor Painting PDFihavenoimagination92% (90)

- Basu and Dutta Accountancy Book Class 12 SolutionsDocument14 pagesBasu and Dutta Accountancy Book Class 12 SolutionsGourab Gorai23% (30)

- Current ResumeDocument1 pageCurrent Resumeapi-489834119Pas encore d'évaluation

- U2 - Keith Haring Comprehension QuestionsDocument3 pagesU2 - Keith Haring Comprehension QuestionsSteve GOopPas encore d'évaluation

- Practical Guide For PHD Candidates at Epfl: Version: August 12, 2008Document91 pagesPractical Guide For PHD Candidates at Epfl: Version: August 12, 2008rjohn1Pas encore d'évaluation

- Muhammad Alif B. Mohd AnuarDocument2 pagesMuhammad Alif B. Mohd AnuarAlif AnuarPas encore d'évaluation

- Studiu de Caz - Lean SCM TescoDocument2 pagesStudiu de Caz - Lean SCM TescoMircea-Nesu CiprianPas encore d'évaluation

- Ogl 481 - Project Management Article - Ogl 320 Project Management Module 7 PaperDocument1 pageOgl 481 - Project Management Article - Ogl 320 Project Management Module 7 Paperapi-513938901Pas encore d'évaluation

- Group 4 Smith Speech Analysis Task 2-2Document4 pagesGroup 4 Smith Speech Analysis Task 2-2api-551088311Pas encore d'évaluation

- People v. Del RosarioDocument2 pagesPeople v. Del RosarioLyleTheresePas encore d'évaluation

- Lesson Plan PDFDocument5 pagesLesson Plan PDFsyed aliPas encore d'évaluation

- An Analysis of Students' Ability in Distinguishing Perfect TenseDocument103 pagesAn Analysis of Students' Ability in Distinguishing Perfect TenseThủy NguyễnPas encore d'évaluation

- ESD File PDFDocument130 pagesESD File PDFRaufPas encore d'évaluation

- Circulatory SystemDocument3 pagesCirculatory SystemAbdurahmaan RaikarPas encore d'évaluation

- Zari WorkDocument3 pagesZari WorkShaluPas encore d'évaluation

- Workshop Guide: The Design ProcessDocument29 pagesWorkshop Guide: The Design ProcessLuisana MartínPas encore d'évaluation

- District Primary Education ProgrammeDocument4 pagesDistrict Primary Education ProgrammeSajid AnsariPas encore d'évaluation

- The Impact of Technology On Learning EnvironmnentDocument7 pagesThe Impact of Technology On Learning EnvironmnentAhmad Ali75% (4)

- WDA WorldofPay A04Document6 pagesWDA WorldofPay A04AVPas encore d'évaluation

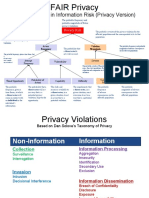

- Factor Analysis in Information Risk (Privacy Version)Document8 pagesFactor Analysis in Information Risk (Privacy Version)Otgonbayar TsengelPas encore d'évaluation

- Kennedy School BrochureDocument2 pagesKennedy School BrochureBrennan GamwellPas encore d'évaluation

- 2.1 Understanding REACH: How Does REACH Work?Document3 pages2.1 Understanding REACH: How Does REACH Work?xixixoxoPas encore d'évaluation

- Long Quiz - TNCTDocument2 pagesLong Quiz - TNCTEditha ArabePas encore d'évaluation

- Corrective and Preventive Action - WikipediaDocument20 pagesCorrective and Preventive Action - WikipediaFkPas encore d'évaluation

- A Critical Review of Benedict AndersonDocument7 pagesA Critical Review of Benedict AndersonMatt Cromwell100% (10)

- Village (NAME) Gram Panchayat (Name)Document135 pagesVillage (NAME) Gram Panchayat (Name)AmanPas encore d'évaluation