Vous aimerez peut-être aussi

- FINA 5470 - Case 3 - Eskimo PieDocument7 pagesFINA 5470 - Case 3 - Eskimo PieYifan ChenPas encore d'évaluation

- Eskimo PieDocument2 pagesEskimo Piechch91750% (2)

- What Is Your Estimate of The Value of Eskimo Pie Corporation As A Stand-Alone Company?Document7 pagesWhat Is Your Estimate of The Value of Eskimo Pie Corporation As A Stand-Alone Company?Ya-ting YangPas encore d'évaluation

- ESKIMO PIE Case StudyDocument13 pagesESKIMO PIE Case StudyPablo Vera100% (1)

- Eskimo PieDocument7 pagesEskimo PieHeather KellerPas encore d'évaluation

- Investment Banking Case AnalysisDocument3 pagesInvestment Banking Case AnalysisSunil VadhvaPas encore d'évaluation

- Eskimo PieDocument30 pagesEskimo PieMing Yang100% (1)

- Popsicle Unilever 7.6% Klondike Empire of Carolin 5.4% Eskimo Pie Eskimo Pie 5.3% Snickers Mars 4.8% Weight Watchers H.J. Heinz 4.3%Document18 pagesPopsicle Unilever 7.6% Klondike Empire of Carolin 5.4% Eskimo Pie Eskimo Pie 5.3% Snickers Mars 4.8% Weight Watchers H.J. Heinz 4.3%Irakli SaliaPas encore d'évaluation

- Eskimo Pie CaseDocument19 pagesEskimo Pie Casedese88Pas encore d'évaluation

- Eskimo Pie FileDocument15 pagesEskimo Pie FilesuwimolJPas encore d'évaluation

- Case IDocument20 pagesCase ICherry KanjanapornsinPas encore d'évaluation

- Eskimo PieDocument6 pagesEskimo PiesarahsalamonPas encore d'évaluation

- FIN4330 HirakiDocument7 pagesFIN4330 Hirakimsg-90Pas encore d'évaluation

- Linear Technology Payout Policy Case 3Document4 pagesLinear Technology Payout Policy Case 3Amrinder SinghPas encore d'évaluation

- case-UST IncDocument10 pagescase-UST Incnipun9143Pas encore d'évaluation

- UST IncDocument16 pagesUST IncNur 'AtiqahPas encore d'évaluation

- Alliance Concrete ForecastingDocument7 pagesAlliance Concrete ForecastingS r kPas encore d'évaluation

- ASTRAL RECORDS - EditedDocument11 pagesASTRAL RECORDS - EditedNarinderPas encore d'évaluation

- Strategic ManagementDocument9 pagesStrategic ManagementdiddiPas encore d'évaluation

- Buckeye Bank CaseDocument7 pagesBuckeye Bank CasePulkit Mathur0% (2)

- Eaton Case Study 2023Document19 pagesEaton Case Study 2023Paskal100% (1)

- FM - INT7 - P&G Case - Group4Document6 pagesFM - INT7 - P&G Case - Group4Ramarayo MotorPas encore d'évaluation

- Purinex Case StudyDocument9 pagesPurinex Case Studylucy007Pas encore d'évaluation

- Debt Policy at Ust Case SolutionDocument2 pagesDebt Policy at Ust Case Solutiontamur_ahan50% (2)

- Hbs Case - Ust Inc.Document4 pagesHbs Case - Ust Inc.Lau See YangPas encore d'évaluation

- TN15 Teletech Corporation 2005Document8 pagesTN15 Teletech Corporation 2005kirkland1234567890100% (2)

- Harris SeafoodsDocument2 pagesHarris SeafoodsNadia Iqbal100% (1)

- Burton SensorsDocument2 pagesBurton SensorsSankalp MishraPas encore d'évaluation

- Teletech Corporation 2005 Case SolutionDocument5 pagesTeletech Corporation 2005 Case SolutionAmrita Sharma100% (1)

- UST SpreadsheetDocument21 pagesUST SpreadsheetTUPas encore d'évaluation

- Debt Policy at Ust Inc Case StudyDocument7 pagesDebt Policy at Ust Inc Case StudyAnton Borisov100% (1)

- Section I. High-Growth Strategy of Marshall, Company Financing and Its Potential Stock Price ChangeDocument11 pagesSection I. High-Growth Strategy of Marshall, Company Financing and Its Potential Stock Price ChangeclendeavourPas encore d'évaluation

- Deluxe Corporation CaseDocument7 pagesDeluxe Corporation Caseankur.mastPas encore d'évaluation

- BurtonsDocument6 pagesBurtonsKritika GoelPas encore d'évaluation

- Debt Policy at UST IncDocument5 pagesDebt Policy at UST Incggrillo73Pas encore d'évaluation

- American Chemical CorporationDocument8 pagesAmerican Chemical CorporationAnastasiaPas encore d'évaluation

- Coursehero 40252829Document2 pagesCoursehero 40252829Janice JingPas encore d'évaluation

- RJR Case StudyDocument5 pagesRJR Case StudyFelipe Kasai MarcosPas encore d'évaluation

- Kohler CompanyDocument3 pagesKohler CompanyDuncan BakerPas encore d'évaluation

- USTDocument4 pagesUSTJames JeffersonPas encore d'évaluation

- Year 1979 1980 1981 1982 1983 1984 Period 0 1 2 3 4 5Document30 pagesYear 1979 1980 1981 1982 1983 1984 Period 0 1 2 3 4 5shardullavande33% (3)

- Astral Records LTD 2Document7 pagesAstral Records LTD 2MbavhaleloPas encore d'évaluation

- Clarkson Lumber Company (7.0)Document17 pagesClarkson Lumber Company (7.0)Hassan Mohiuddin100% (1)

- Encana Case SolutionDocument15 pagesEncana Case SolutionGautam SethiPas encore d'évaluation

- Midland Energy Resources Case Study: FINS3625-Applied Corporate FinanceDocument11 pagesMidland Energy Resources Case Study: FINS3625-Applied Corporate FinanceCourse Hero100% (1)

- Blaine-Kitchenware Case CalculationsDocument6 pagesBlaine-Kitchenware Case CalculationsDennis Alexander Guerrero100% (1)

- Dow 18,000 - What Should I Do About Risk?! - Gevers Wealth Management LLC - May 2015Document15 pagesDow 18,000 - What Should I Do About Risk?! - Gevers Wealth Management LLC - May 2015Gevers Wealth Management, LLCPas encore d'évaluation

- Common Sense InvestingDocument20 pagesCommon Sense InvestingAman TiwariPas encore d'évaluation

- Understanding Financial Statements: Problem 1Document5 pagesUnderstanding Financial Statements: Problem 1Sandeep MishraPas encore d'évaluation

- Earnings Power - Hewitt HeisermanDocument14 pagesEarnings Power - Hewitt HeisermanSivakumar GanesanPas encore d'évaluation

- AltaRock Mid 2011 LetterDocument15 pagesAltaRock Mid 2011 LetterAnoop Kamlesh Davé100% (1)

- Esmark, Inc.: Macr Case SubmissionDocument8 pagesEsmark, Inc.: Macr Case SubmissionAyush AgarwalPas encore d'évaluation

- Solution Engineering EconomicsDocument130 pagesSolution Engineering EconomicsSparrowGospleGilbertPas encore d'évaluation

- Greenlight Capital Q3 2013 LetterDocument8 pagesGreenlight Capital Q3 2013 LetterWall Street WanderlustPas encore d'évaluation

- FM AppleDocument12 pagesFM AppleREJISH MATHEWPas encore d'évaluation

- Stock Whyyys 3Document101 pagesStock Whyyys 3depressionhurtsmePas encore d'évaluation

- David Einhorn's Apple Inc. Iprefs PresentationDocument55 pagesDavid Einhorn's Apple Inc. Iprefs PresentationDealBook100% (1)

- Seven Generations Energy LTD.: Canada ResearchDocument27 pagesSeven Generations Energy LTD.: Canada ResearchAnonymous m3c6M1Pas encore d'évaluation

- Adecco Case Solution APO 3Document3 pagesAdecco Case Solution APO 3ArchismanPas encore d'évaluation

- API Blogger Conference Call: John Felmy and Industry Earnings - 4.23.07Document9 pagesAPI Blogger Conference Call: John Felmy and Industry Earnings - 4.23.07Energy TomorrowPas encore d'évaluation

- Nasdaq GRMN 2016Document150 pagesNasdaq GRMN 2016Irakli SaliaPas encore d'évaluation

- Garmin Final FileDocument34 pagesGarmin Final FileIrakli SaliaPas encore d'évaluation

- Garmin Final FileDocument34 pagesGarmin Final FileIrakli SaliaPas encore d'évaluation

- NamesDocument1 pageNamesIrakli SaliaPas encore d'évaluation

- Current Assets: Liabilities and Stockholders' EquityDocument9 pagesCurrent Assets: Liabilities and Stockholders' EquityIrakli SaliaPas encore d'évaluation

- Overview of Ocean Carriers CaseDocument2 pagesOverview of Ocean Carriers CaseIrakli SaliaPas encore d'évaluation

- Popsicle Unilever 7.6% Klondike Empire of Carolin 5.4% Eskimo Pie Eskimo Pie 5.3% Snickers Mars 4.8% Weight Watchers H.J. Heinz 4.3%Document18 pagesPopsicle Unilever 7.6% Klondike Empire of Carolin 5.4% Eskimo Pie Eskimo Pie 5.3% Snickers Mars 4.8% Weight Watchers H.J. Heinz 4.3%Irakli SaliaPas encore d'évaluation

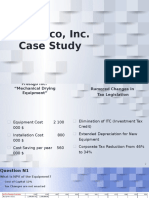

- Pressco, Inc. Case Study: Corporate Finance II Irakli Salia 17-9 Nino Merabishvili 17-8Document18 pagesPressco, Inc. Case Study: Corporate Finance II Irakli Salia 17-9 Nino Merabishvili 17-8Irakli SaliaPas encore d'évaluation

- No Tax Change ScenarioDocument52 pagesNo Tax Change ScenarioIrakli SaliaPas encore d'évaluation

- Eskimo Pie CorporationDocument1 pageEskimo Pie CorporationIrakli SaliaPas encore d'évaluation

- Exhibit 4 Industry Information For Frozen NoveltiesDocument25 pagesExhibit 4 Industry Information For Frozen NoveltiesIrakli SaliaPas encore d'évaluation

- No Tax Change ScenarioDocument52 pagesNo Tax Change ScenarioIrakli SaliaPas encore d'évaluation

- Pressco Case Memo PDFDocument7 pagesPressco Case Memo PDFIrakli SaliaPas encore d'évaluation

- No Tax Change ScenarioDocument52 pagesNo Tax Change ScenarioIrakli SaliaPas encore d'évaluation

- Pressco Inc. Case StudyDocument18 pagesPressco Inc. Case StudyIrakli SaliaPas encore d'évaluation

- Pressco, IncDocument6 pagesPressco, Incrasmitamisra0% (1)

- Case IDocument20 pagesCase ICherry KanjanapornsinPas encore d'évaluation

- No Tax Change ScenarioDocument52 pagesNo Tax Change ScenarioIrakli SaliaPas encore d'évaluation

- Pressco 2c IncDocument14 pagesPressco 2c IncIrakli SaliaPas encore d'évaluation

- Pressco Inc. Case StudyDocument19 pagesPressco Inc. Case StudyIrakli SaliaPas encore d'évaluation

- Nasdaq GRMN 2017Document149 pagesNasdaq GRMN 2017Irakli SaliaPas encore d'évaluation

- Garmin Final FileDocument34 pagesGarmin Final FileIrakli SaliaPas encore d'évaluation

- Eskimo Pie CorporationDocument1 pageEskimo Pie CorporationIrakli SaliaPas encore d'évaluation

- Nasdaq GRMN 2019Document112 pagesNasdaq GRMN 2019Irakli SaliaPas encore d'évaluation

- Nasdaq GRMN 2018Document188 pagesNasdaq GRMN 2018Irakli SaliaPas encore d'évaluation

- Nasdaq GRMN 2016Document150 pagesNasdaq GRMN 2016Irakli SaliaPas encore d'évaluation

- Amazon-Redshift-Case-Study-Brightcove - CopieDocument4 pagesAmazon-Redshift-Case-Study-Brightcove - CopieAbelBabelPas encore d'évaluation

- AfarDocument3 pagesAfarLeizzamar BayadogPas encore d'évaluation

- Together We LeadDocument8 pagesTogether We LeadBurjuman JumeirahPas encore d'évaluation

- Toward Enterprise Agile Scalability: Pat ReedDocument42 pagesToward Enterprise Agile Scalability: Pat ReedJason Oz100% (1)

- Annex H - CLSD Implementing Guidelines - Safekeeping of Loan Documents - FNDocument3 pagesAnnex H - CLSD Implementing Guidelines - Safekeeping of Loan Documents - FNJan Paolo CruzPas encore d'évaluation

- Lead Tracking TemplateDocument12 pagesLead Tracking TemplatevenkateshsjPas encore d'évaluation

- Proposed: Authorization Matrix - Human Resource / PayrollDocument1 pageProposed: Authorization Matrix - Human Resource / PayrollHussain Al ShakhouriPas encore d'évaluation

- Financial Statement Analysis Of: Asian Paints LimitedDocument20 pagesFinancial Statement Analysis Of: Asian Paints LimitedPreetiPas encore d'évaluation

- Chapter 5 - 7 Eleven Case Studies - QuesDocument3 pagesChapter 5 - 7 Eleven Case Studies - QuesMary KarmacharyaPas encore d'évaluation

- RIT - Case Brief - ALGO1 - Algorithmic ArbitrageDocument3 pagesRIT - Case Brief - ALGO1 - Algorithmic Arbitragechriswong0113Pas encore d'évaluation

- Cips L5M6 V4Document14 pagesCips L5M6 V4Batam InterpreterPas encore d'évaluation

- Process Process Process ProcessDocument2 pagesProcess Process Process Processarun mathewPas encore d'évaluation

- Fundamentals of Corporate Finance 12th Edition Ross Test BankDocument35 pagesFundamentals of Corporate Finance 12th Edition Ross Test Bankadeliahue1q9kl100% (19)

- BU9201 Course Outline 20132014s1Document2 pagesBU9201 Course Outline 20132014s1Feeling_so_flyPas encore d'évaluation

- Intermediate Accounting 2 Quiz #3Document4 pagesIntermediate Accounting 2 Quiz #3Claire Magbunag AntidoPas encore d'évaluation

- Isb511 - Assg Ind 1Document19 pagesIsb511 - Assg Ind 12022923703Pas encore d'évaluation

- Tally - ERP 9: Major Features of - Power of SimplicityDocument8 pagesTally - ERP 9: Major Features of - Power of SimplicityfawwazPas encore d'évaluation

- Mobily Case StudyDocument4 pagesMobily Case StudySteve CromptonPas encore d'évaluation

- Al Azim Transport PVT LTDDocument10 pagesAl Azim Transport PVT LTDAl Azim TransportPas encore d'évaluation

- Strategic Management and Business Policy Global 15th Edition Hunger Test BankDocument29 pagesStrategic Management and Business Policy Global 15th Edition Hunger Test Bankkiethanh0na91100% (31)

- 1 Pengenalan Penambangan Data-IMDDocument34 pages1 Pengenalan Penambangan Data-IMDherawatieti52Pas encore d'évaluation

- Chapter 9 (English)Document25 pagesChapter 9 (English)Idem MedPas encore d'évaluation

- Pidllite Training FinalDocument94 pagesPidllite Training FinalChandan SrivastavaPas encore d'évaluation

- Case 3 Chemalite Inc Cash FlowDocument3 pagesCase 3 Chemalite Inc Cash Flowmohiyuddinsakhib3260Pas encore d'évaluation

- Resume - Daniel Liu Aug 2019 3Document1 pageResume - Daniel Liu Aug 2019 3Daniel LiuPas encore d'évaluation

- Kolej Vokasional - Jabatan Teknologi Mekanikal Dan PembuatanDocument6 pagesKolej Vokasional - Jabatan Teknologi Mekanikal Dan PembuatanAnuar SallehPas encore d'évaluation

- GST Accounting PDFDocument17 pagesGST Accounting PDFBOO KIANG MINGPas encore d'évaluation

- Factors Affecting Channel Choice - PpsDocument14 pagesFactors Affecting Channel Choice - PpsSmriti KhannaPas encore d'évaluation

- Income Taxation - Ampongan (SolMan)Document56 pagesIncome Taxation - Ampongan (SolMan)John Dale Mondejar75% (12)

- Unit 3: Human Resource Management: Assignment BriefDocument4 pagesUnit 3: Human Resource Management: Assignment BriefGharis Soomro100% (1)