Vous aimerez peut-être aussi

- ABC MCQ TheoryDocument2 pagesABC MCQ TheoryGlayca PallerPas encore d'évaluation

- ZMSQ 12 Activity Based CostingDocument10 pagesZMSQ 12 Activity Based CostingJohn Carlo Peru0% (1)

- Cost Accounting IDocument46 pagesCost Accounting IMohamed HosnyPas encore d'évaluation

- CPA REVIEW SCHOOL ACTIVITY-BASED COSTINGDocument9 pagesCPA REVIEW SCHOOL ACTIVITY-BASED COSTINGVher Christopher DucayPas encore d'évaluation

- Activity Based CostingDocument16 pagesActivity Based CostingNekka FenkPas encore d'évaluation

- Activity Based CostingDocument18 pagesActivity Based CostingRavi ChauhanPas encore d'évaluation

- ZMSQ 12 Activity Based CostingDocument9 pagesZMSQ 12 Activity Based CostingMonica MonicaPas encore d'évaluation

- ABC - ReviewerDocument9 pagesABC - ReviewerAndrea Nicole MASANGKAYPas encore d'évaluation

- Mas 5Document6 pagesMas 5Krishia GarciaPas encore d'évaluation

- ABC QuizDocument11 pagesABC Quizlou-924Pas encore d'évaluation

- Abc & TraditionalDocument26 pagesAbc & TraditionalJamille Victorio BautistaPas encore d'évaluation

- Additional 14 and 5Document4 pagesAdditional 14 and 5Fatma ElzaytPas encore d'évaluation

- ABC Methods for Improved Costing and ManagementDocument26 pagesABC Methods for Improved Costing and ManagementPeter Angelo BangaanPas encore d'évaluation

- Galoso, Ma - Therese S.: Select The Letter of The Best AnswerDocument25 pagesGaloso, Ma - Therese S.: Select The Letter of The Best AnswerPatrick NocedoPas encore d'évaluation

- Activity-Based Cost SystemDocument15 pagesActivity-Based Cost SystemLuke Robert HemmingsPas encore d'évaluation

- ZMSQ 12 Activity Based CostingDocument8 pagesZMSQ 12 Activity Based CostingMonica MonicaPas encore d'évaluation

- Cost Old DeptalsDocument9 pagesCost Old Deptalsyugyeom rojas0% (1)

- Mock BA 116 2nd LEDocument11 pagesMock BA 116 2nd LEAria LeenPas encore d'évaluation

- COST ACCOUNTING 1-4 FinalDocument28 pagesCOST ACCOUNTING 1-4 FinalChristian Blanza Lleva100% (1)

- Additional Probllems For Service Cost Allocation PDFDocument9 pagesAdditional Probllems For Service Cost Allocation PDFsfsdfsdfPas encore d'évaluation

- MAS Bobadilla 01-Activity Based CostingDocument11 pagesMAS Bobadilla 01-Activity Based CostingEdi wow WowPas encore d'évaluation

- Activity-Based-Costing Q23-2Document12 pagesActivity-Based-Costing Q23-2Daniel HarrisonPas encore d'évaluation

- Cost Accounting Systems (B. Activity Based Cost System)Document13 pagesCost Accounting Systems (B. Activity Based Cost System)Clene DocontePas encore d'évaluation

- Reviewer in Abc Costing: Cost Accounting AND Control (B. Activity-Based Cost System)Document14 pagesReviewer in Abc Costing: Cost Accounting AND Control (B. Activity-Based Cost System)justine reine cornicoPas encore d'évaluation

- Activity-Based Costing Systems: Benefits, Concepts & ImplementationDocument11 pagesActivity-Based Costing Systems: Benefits, Concepts & ImplementationKeach Harrel CabagayPas encore d'évaluation

- Activity-Based Costing Systems: Benefits, Concepts & ImplementationDocument17 pagesActivity-Based Costing Systems: Benefits, Concepts & ImplementationnaddiePas encore d'évaluation

- MS 3413 Activity-Based Costing SystemDocument5 pagesMS 3413 Activity-Based Costing SystemMonica GarciaPas encore d'évaluation

- ABC Quiz With SolutionDocument13 pagesABC Quiz With Solutionlou-924Pas encore d'évaluation

- Activity Based CostingDocument13 pagesActivity Based CostingJoshPas encore d'évaluation

- 18 ABC Backflushed X 2.docx-1Document58 pages18 ABC Backflushed X 2.docx-1NopePas encore d'évaluation

- Operation Costing Review QuestionsDocument2 pagesOperation Costing Review QuestionsAndriaPas encore d'évaluation

- Job Costing Multiple Choice QuestionsDocument15 pagesJob Costing Multiple Choice Questionswer zul0% (2)

- ABC Traditional Costing - BCSVDocument25 pagesABC Traditional Costing - BCSVdenPas encore d'évaluation

- 18 x12 ABC A Traditional Cost AccountingDocument13 pages18 x12 ABC A Traditional Cost AccountingQueenie VallePas encore d'évaluation

- Activity Based CostingDocument13 pagesActivity Based CostingJoshPas encore d'évaluation

- 18 x12 ABC A Traditional Cost Accounting (MAS) BobadillaDocument11 pages18 x12 ABC A Traditional Cost Accounting (MAS) BobadillaAnnaPas encore d'évaluation

- Job Cost Multiple ChoiceeDocument4 pagesJob Cost Multiple ChoiceeLouisePas encore d'évaluation

- 19 x12 ABC B Activity-Based Cost SystemDocument15 pages19 x12 ABC B Activity-Based Cost SystemJericho Pedragosa67% (6)

- MasDocument4 pagesMasSe LujPas encore d'évaluation

- Test Bank ABCDocument36 pagesTest Bank ABCLoise ManioPas encore d'évaluation

- Cost Mock Compre With AnsDocument15 pagesCost Mock Compre With Anssky dela cruzPas encore d'évaluation

- Test bank-ABCDocument40 pagesTest bank-ABCKatrina Peralta FabianPas encore d'évaluation

- Activity Based CostingDocument11 pagesActivity Based CostingVijay Raghavan0% (1)

- Absorption and AbcDocument36 pagesAbsorption and AbcTricia Mae FernandezPas encore d'évaluation

- Activity Based CostingDocument12 pagesActivity Based CostingAilein GracePas encore d'évaluation

- MAS - Variance AnalysisDocument13 pagesMAS - Variance AnalysisGhaill CruzPas encore d'évaluation

- Management Advisory Services Adb/Jju/Bdt MAS.2814 - Activity-Based Costing System MAY 2020Document2 pagesManagement Advisory Services Adb/Jju/Bdt MAS.2814 - Activity-Based Costing System MAY 2020Donny TrumpPas encore d'évaluation

- ABC CHAPTERDocument11 pagesABC CHAPTERThezenwayPas encore d'évaluation

- 18 x12 ABC A Traditional Cost Accounting (MAS) BobadillaDocument12 pages18 x12 ABC A Traditional Cost Accounting (MAS) BobadillaAnnaPas encore d'évaluation

- Cost Management: A Case for Business Process Re-engineeringD'EverandCost Management: A Case for Business Process Re-engineeringPas encore d'évaluation

- Google Cloud Professional Cloud Architect Exam Q & A.D'EverandGoogle Cloud Professional Cloud Architect Exam Q & A.Pas encore d'évaluation

- Charging Communication Networks: From Theory to PracticeD'EverandCharging Communication Networks: From Theory to PracticeD.J. SonghurstPas encore d'évaluation

- Architect's Essentials of Cost ManagementD'EverandArchitect's Essentials of Cost ManagementÉvaluation : 5 sur 5 étoiles5/5 (2)

- SAP Variant Configuration: Your Successful Guide to ModelingD'EverandSAP Variant Configuration: Your Successful Guide to ModelingÉvaluation : 5 sur 5 étoiles5/5 (2)

- Cna PS Depot 10262023Document6 pagesCna PS Depot 10262023Phoeza Espinosa VillanuevaPas encore d'évaluation

- Activity Design MaramagDocument3 pagesActivity Design MaramagPhoeza Espinosa VillanuevaPas encore d'évaluation

- MOA For TABLET 2023Document2 pagesMOA For TABLET 2023Phoeza Espinosa VillanuevaPas encore d'évaluation

- DepEd Lanao del Norte Certification for RetirementDocument1 pageDepEd Lanao del Norte Certification for RetirementPhoeza Espinosa VillanuevaPas encore d'évaluation

- Certificate of Turn OverDocument3 pagesCertificate of Turn OverPhoeza Espinosa VillanuevaPas encore d'évaluation

- Cl2022!14!1 Insurance ContractsDocument5 pagesCl2022!14!1 Insurance ContractsPhoeza Espinosa VillanuevaPas encore d'évaluation

- CS Form No. 6, Revised 2020 (More Than 60 Days)Document1 pageCS Form No. 6, Revised 2020 (More Than 60 Days)Phoeza Espinosa VillanuevaPas encore d'évaluation

- 1041 COC-PolicyOrientationEO138 PDFDocument1 page1041 COC-PolicyOrientationEO138 PDFPhoeza Espinosa VillanuevaPas encore d'évaluation

- Foreign Grants Fund EntriesDocument23 pagesForeign Grants Fund Entriesjaymark canayaPas encore d'évaluation

- Investment in Associate-HandoutDocument9 pagesInvestment in Associate-HandoutPhoeza Espinosa VillanuevaPas encore d'évaluation

- Purchase OrderDocument4 pagesPurchase OrderPhoeza Espinosa VillanuevaPas encore d'évaluation

- Ali Sec17a 2020Document376 pagesAli Sec17a 2020Phoeza Espinosa VillanuevaPas encore d'évaluation

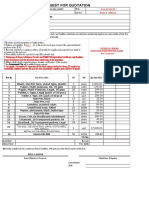

- Request For Quotation NewDocument1 pageRequest For Quotation NewPhoeza Espinosa VillanuevaPas encore d'évaluation

- CPAORS PPT Share-Based ConceptsDocument24 pagesCPAORS PPT Share-Based ConceptsPhoeza Espinosa VillanuevaPas encore d'évaluation

- 2021 Mooe Initial Reqts For DownloadingDocument2 pages2021 Mooe Initial Reqts For DownloadingPhoeza Espinosa VillanuevaPas encore d'évaluation

- AFAR Job Order Costing ProblemsDocument4 pagesAFAR Job Order Costing ProblemsPhoeza Espinosa VillanuevaPas encore d'évaluation

- Liquidation Certification 1Document1 pageLiquidation Certification 1Phoeza Espinosa VillanuevaPas encore d'évaluation

- 29 LDPlanningAug9-15Document1 page29 LDPlanningAug9-15Phoeza Espinosa VillanuevaPas encore d'évaluation

- How Do Contingency Factors Influence Organizational DesignDocument10 pagesHow Do Contingency Factors Influence Organizational DesignPhoeza Espinosa VillanuevaPas encore d'évaluation

- The Key To Organizational DesignDocument8 pagesThe Key To Organizational DesignPhoeza Espinosa VillanuevaPas encore d'évaluation

- Organization & Org StructureDocument16 pagesOrganization & Org StructurePhoeza Espinosa VillanuevaPas encore d'évaluation

- Pa 217 - Sani, NF - Whathow - Design Effective InterventionsDocument16 pagesPa 217 - Sani, NF - Whathow - Design Effective InterventionsPhoeza Espinosa VillanuevaPas encore d'évaluation

- New Format of FormsDocument21 pagesNew Format of FormsPhoeza Espinosa VillanuevaPas encore d'évaluation

- 217 Intro To OD, Process and Its RelevanceDocument8 pages217 Intro To OD, Process and Its RelevancePhoeza Espinosa VillanuevaPas encore d'évaluation

- Contingency Factors: Phoeza Espinosa-Villanueva PA 217 ReporterDocument13 pagesContingency Factors: Phoeza Espinosa-Villanueva PA 217 ReporterPhoeza Espinosa VillanuevaPas encore d'évaluation

- Omnibus Sworn StatementDocument3 pagesOmnibus Sworn StatementPhoeza Espinosa VillanuevaPas encore d'évaluation

- Design of Individual PositionsDocument12 pagesDesign of Individual PositionsPhoeza Espinosa VillanuevaPas encore d'évaluation

- 2020 ChecklistDocument17 pages2020 ChecklistPhoeza Espinosa Villanueva100% (1)

- MemberChangeInformation V06Document2 pagesMemberChangeInformation V06joy barrameda50% (2)

- DO s2020 018.deped - Order.memoDocument6 pagesDO s2020 018.deped - Order.memobenz cadiongPas encore d'évaluation

- Fair Value of The Property: Partner's Drawing, DebitDocument12 pagesFair Value of The Property: Partner's Drawing, DebitAera GarcesPas encore d'évaluation

- Fundamentals of Accountancy, Business and Management 1 (FABM 1)Document17 pagesFundamentals of Accountancy, Business and Management 1 (FABM 1)Gladzangel Loricabv50% (2)

- Daftar Pustaka: WWW - Bkkbn.go - IdDocument4 pagesDaftar Pustaka: WWW - Bkkbn.go - IdOca DocaPas encore d'évaluation

- Portfolio Management - Chapter 7Document85 pagesPortfolio Management - Chapter 7Dr Rushen SinghPas encore d'évaluation

- 02 Task Performance 3Document4 pages02 Task Performance 3Allyza RenoballesPas encore d'évaluation

- Marketing Strategies and Business Operations of Take Home Appliances and FurnitureDocument56 pagesMarketing Strategies and Business Operations of Take Home Appliances and FurnitureJericho Lavaniego-CerezoPas encore d'évaluation

- Study Break Audit UASDocument5 pagesStudy Break Audit UASCharis SubiantoPas encore d'évaluation

- Maf 620 Dutch LadyDocument9 pagesMaf 620 Dutch LadyNur IfaPas encore d'évaluation

- Creating Customer Value, Satisfaction, and LoyaltyDocument26 pagesCreating Customer Value, Satisfaction, and LoyaltyPratik RajPas encore d'évaluation

- Oligopoly Market.2022Document4 pagesOligopoly Market.2022Mouna RachidPas encore d'évaluation

- Mall of IndiaDocument19 pagesMall of IndiaBhupesh MaharaPas encore d'évaluation

- Business ModelDocument8 pagesBusiness Modelnalie208Pas encore d'évaluation

- Tropicana Case Study Packaging Design FailureDocument8 pagesTropicana Case Study Packaging Design FailureLamd100% (1)

- INTERNATIONAL MARKETINGDocument10 pagesINTERNATIONAL MARKETINGMaita Dabilbil Flores100% (2)

- Manila MAY 5, 2022 Preweek Material: Management Advisory ServicesDocument25 pagesManila MAY 5, 2022 Preweek Material: Management Advisory ServicesJoris YapPas encore d'évaluation

- Philippine Donut Consumer Behavior SurveyDocument5 pagesPhilippine Donut Consumer Behavior SurveyDerick FloresPas encore d'évaluation

- Strategic Management A Competitive Advantage Approach Concepts and Cases Global Edition 16th Edition David Test BankDocument39 pagesStrategic Management A Competitive Advantage Approach Concepts and Cases Global Edition 16th Edition David Test Bankmatthewho136100% (18)

- Upgrade & Increase Credit Limit FormDocument3 pagesUpgrade & Increase Credit Limit FormTan Kae JiunnPas encore d'évaluation

- How Large Is The MarketDocument3 pagesHow Large Is The MarketJef De VeraPas encore d'évaluation

- 02 Fixed Cost Manufacturing FinishedDocument6 pages02 Fixed Cost Manufacturing FinishedpankajPas encore d'évaluation

- Casestudy Kalsi AgroDocument3 pagesCasestudy Kalsi AgroGPLPas encore d'évaluation

- MRK718 - Assignment - Ice Castle-Qudsia NourasDocument7 pagesMRK718 - Assignment - Ice Castle-Qudsia NourasQudsia NourasPas encore d'évaluation

- Translation Exposure Management PDFDocument13 pagesTranslation Exposure Management PDFpilotPas encore d'évaluation

- MJ, J, JL JH LKNDocument285 pagesMJ, J, JL JH LKNdvgfgfdhPas encore d'évaluation

- SANIL Sales Resume 24.05.2023Document3 pagesSANIL Sales Resume 24.05.2023Sanil MonPas encore d'évaluation

- Little Blue Book, 2016 EditionDocument146 pagesLittle Blue Book, 2016 EditiongiovanniPas encore d'évaluation

- Case Summary-Moore MedicalDocument2 pagesCase Summary-Moore MedicalIshita RaiPas encore d'évaluation

- FY19 - QBDT Client - Lesson 1 - Get Started - BDB - v4Document26 pagesFY19 - QBDT Client - Lesson 1 - Get Started - BDB - v4Nyasha MakorePas encore d'évaluation

- SWOT Analysis and The Smart in BusinessDocument16 pagesSWOT Analysis and The Smart in BusinessSam SonPas encore d'évaluation

- Chapter 1 - Introduction To BusinessDocument27 pagesChapter 1 - Introduction To Businesstrandinh2828Pas encore d'évaluation