Vous aimerez peut-être aussi

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5795)

- Sustainability Dilemmas in Emerging Economies: SciencedirectDocument13 pagesSustainability Dilemmas in Emerging Economies: Sciencedirectpandey_manishPas encore d'évaluation

- Emotional Intelligence, Work/Family Conflict, and Work Values Among Customer Service Representatives: Basis For Organizational SupportDocument9 pagesEmotional Intelligence, Work/Family Conflict, and Work Values Among Customer Service Representatives: Basis For Organizational Supportpandey_manishPas encore d'évaluation

- Management Science Letters: Service Quality and Switching Behavior of CustomersDocument10 pagesManagement Science Letters: Service Quality and Switching Behavior of Customerspandey_manishPas encore d'évaluation

- CRM Practices in Electricity Distribution in India - Supply Side Perspective - v2 PDFDocument61 pagesCRM Practices in Electricity Distribution in India - Supply Side Perspective - v2 PDFpandey_manishPas encore d'évaluation

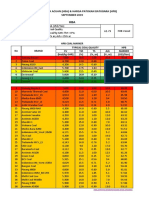

- Badaun - CGD Potential SummaryDocument1 pageBadaun - CGD Potential Summarypandey_manishPas encore d'évaluation

- The Difference Between Sales and Marketing by Jim StovallDocument11 pagesThe Difference Between Sales and Marketing by Jim Stovallpandey_manishPas encore d'évaluation

- Form No. 26AS Annual Tax Statement Under Section 203AADocument8 pagesForm No. 26AS Annual Tax Statement Under Section 203AApandey_manishPas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Belarus Project DetailsDocument2 pagesBelarus Project DetailsNikki KlevePas encore d'évaluation

- Brazil Map 2015062615 AdsDocument1 pageBrazil Map 2015062615 AdsSérgio SouzaPas encore d'évaluation

- CV Dedi Supriyadi - Ab - CT - PSV - AhtsDocument3 pagesCV Dedi Supriyadi - Ab - CT - PSV - AhtsDamar Lintas Buana Co., Ltd.Pas encore d'évaluation

- Trelleborg Engineered Products Bearing Product BrochureDocument14 pagesTrelleborg Engineered Products Bearing Product BrochureYong KimPas encore d'évaluation

- PGTF AepparticipantsDocument24 pagesPGTF AepparticipantsNeelesh ShettyPas encore d'évaluation

- 818PetroleumHistory6 PDFDocument1 page818PetroleumHistory6 PDFMazhar BadrPas encore d'évaluation

- Energy Argus Petroleum CokeDocument19 pagesEnergy Argus Petroleum CokeJohanMargono100% (1)

- Curriculum Vitae: January 1, 2020Document6 pagesCurriculum Vitae: January 1, 2020Green Sustain EnergyPas encore d'évaluation

- API 650-2007 钢制焊接石油储罐 ChineseDocument430 pagesAPI 650-2007 钢制焊接石油储罐 ChinesesujinlongPas encore d'évaluation

- Dip Tank5Document300 pagesDip Tank5Arshad KhanPas encore d'évaluation

- Prices Effective Dated April 01 2016Document13 pagesPrices Effective Dated April 01 2016Adnan AkhtarPas encore d'évaluation

- Voith: Voith Variable Speed Drives in Offshore Applications - 1Document2 pagesVoith: Voith Variable Speed Drives in Offshore Applications - 1sugeng wahyudiPas encore d'évaluation

- Cash MemoDocument2 pagesCash MemoJayesh PatilPas encore d'évaluation

- Sinopec (Internasional)Document15 pagesSinopec (Internasional)nazmanur aulia21Pas encore d'évaluation

- Development of Aspirational Districts0 3Document30 pagesDevelopment of Aspirational Districts0 3himanshuPas encore d'évaluation

- Heavy Oil Reservoir: University Project - II Seminar OnDocument10 pagesHeavy Oil Reservoir: University Project - II Seminar OnRahul ChandranPas encore d'évaluation

- Landowners' Motion For Oral ArgumentsDocument5 pagesLandowners' Motion For Oral ArgumentshefflingerPas encore d'évaluation

- Reference List For Compressor Application 2009Document10 pagesReference List For Compressor Application 2009sugeng wahyudi100% (1)

- 1basic Concepts in Reservoir EngineeringDocument14 pages1basic Concepts in Reservoir EngineeringAmir100% (1)

- Price Build-Up Effective 1st August 2023Document1 pagePrice Build-Up Effective 1st August 2023Lisa MalbonPas encore d'évaluation

- Harga Batubara Acuan (Hba) & Harga Patokan Batubara (HPB) September 2019Document8 pagesHarga Batubara Acuan (Hba) & Harga Patokan Batubara (HPB) September 2019Adnan NstPas encore d'évaluation

- Kazakh CrudeDocument11 pagesKazakh CrudeValentinoIgosevPas encore d'évaluation

- Downstream Oil and Gas Industry - Energy EducationDocument2 pagesDownstream Oil and Gas Industry - Energy Educationmbw000012378Pas encore d'évaluation

- (JP Morgan) Oil & Gas BasicsDocument69 pages(JP Morgan) Oil & Gas BasicsAnonymous Vbv8SHv0b100% (2)

- Lecture1 - Introduction To The Oil and Gas IndustryDocument118 pagesLecture1 - Introduction To The Oil and Gas IndustrygeorgiadisgPas encore d'évaluation

- Rekap Hasil Analisa Batubara Mingguan PLTU Sulbagut-1 2 X 50 MWDocument1 pageRekap Hasil Analisa Batubara Mingguan PLTU Sulbagut-1 2 X 50 MWmuhbayusaputroiPas encore d'évaluation

- Oil EngineDocument19 pagesOil Enginethomas kobakPas encore d'évaluation

- Paginas para Busqueda de Trabajo PetroleroDocument9 pagesPaginas para Busqueda de Trabajo PetroleroAngel ApontePas encore d'évaluation

- South Africa To InvestDocument5 pagesSouth Africa To InvestJatinPas encore d'évaluation

- Pret Benzina, Motorina Si GPL Gazprom, Lukoil, Mol, OMV, Petrom, Rompetrol, Socar, BLKOil, CellyRo, Fermierul, MaximCoLtd, MetrDocument1 pagePret Benzina, Motorina Si GPL Gazprom, Lukoil, Mol, OMV, Petrom, Rompetrol, Socar, BLKOil, CellyRo, Fermierul, MaximCoLtd, MetrNicu LunguPas encore d'évaluation