Vous aimerez peut-être aussi

- Consumer'S Behaviour & Theory of Demand: Unit 2Document13 pagesConsumer'S Behaviour & Theory of Demand: Unit 2poorviPas encore d'évaluation

- Ch4-2 Macro EconomicsDocument11 pagesCh4-2 Macro EconomicsSultan AnticsPas encore d'évaluation

- Elasticity of Demand ECODocument45 pagesElasticity of Demand ECOYash TRIPATHIPas encore d'évaluation

- Elasticity and Demand: Essential ConceptsDocument5 pagesElasticity and Demand: Essential ConceptsRohit SinhaPas encore d'évaluation

- Managerial Economics Foundations of Business Analysis and Strategy 12th Edition Thomas Solutions Manual DownloadDocument6 pagesManagerial Economics Foundations of Business Analysis and Strategy 12th Edition Thomas Solutions Manual DownloadDouglasColeybed100% (34)

- 专题1 7讲解版Document80 pages专题1 7讲解版bbbbdxPas encore d'évaluation

- Chapter II - MicroeconomicsDocument46 pagesChapter II - MicroeconomicsDuresa GemechuPas encore d'évaluation

- Consumer Behavior Indirect Utility and Reservation PricesDocument20 pagesConsumer Behavior Indirect Utility and Reservation PricesAnshu JainPas encore d'évaluation

- Elasticity and Its Applications - 5 - 6 - 920220823223838Document26 pagesElasticity and Its Applications - 5 - 6 - 920220823223838Aditi SinhaPas encore d'évaluation

- Term Paper On Micro EconomicsDocument39 pagesTerm Paper On Micro EconomicsFardus MahmudPas encore d'évaluation

- 1 ElasticityOfDemand 1Document23 pages1 ElasticityOfDemand 1Sam SamPas encore d'évaluation

- Session5-Elasticity and Its Application-1Document39 pagesSession5-Elasticity and Its Application-1askdgasPas encore d'évaluation

- Market Demand & Elasticity: © 2004 Thomson Learning/South-WesternDocument68 pagesMarket Demand & Elasticity: © 2004 Thomson Learning/South-WesternAsif Islam SamannoyPas encore d'évaluation

- Tutorial 03 Solution 05-03-2024Document59 pagesTutorial 03 Solution 05-03-2024Aziz AyadiPas encore d'évaluation

- Elasticity of Demand and Supply at Makerere UniversityDocument5 pagesElasticity of Demand and Supply at Makerere UniversitysdgsfgdgPas encore d'évaluation

- Demand Notes1Document25 pagesDemand Notes1Jada CallistePas encore d'évaluation

- 2 - Market Demand Analysis & Applications - Dr. MakuyanaDocument31 pages2 - Market Demand Analysis & Applications - Dr. MakuyanasimbaPas encore d'évaluation

- Eks B 40 A - Victoria Febrina R S 40P20035Document9 pagesEks B 40 A - Victoria Febrina R S 40P20035Viky SongorPas encore d'évaluation

- Micro Economics DemandDocument33 pagesMicro Economics DemandDr. Sana FatimaPas encore d'évaluation

- Demand, Supply, and Market Equilibrium Concepts ExplainedDocument35 pagesDemand, Supply, and Market Equilibrium Concepts ExplainedRobert AxelssonPas encore d'évaluation

- Project Report ON Elasticity of Demand & Supply: Mba/Pgdm (2009-2011) New Delhi Institute of ManagementDocument32 pagesProject Report ON Elasticity of Demand & Supply: Mba/Pgdm (2009-2011) New Delhi Institute of ManagementNitin Rana71% (7)

- A Generalized Huff ModelDocument10 pagesA Generalized Huff ModelasharPas encore d'évaluation

- Demand Willingness+ Purchasing PowerDocument7 pagesDemand Willingness+ Purchasing PowerZahra ArifPas encore d'évaluation

- 10e 02 Chap Student WorkbookDocument25 pages10e 02 Chap Student WorkbookTakuriPas encore d'évaluation

- Logic HumDocument10 pagesLogic Humapi-3709182Pas encore d'évaluation

- Elastisitas Dan Sensitivitas Demand: Mata Kuliah: Ekonomi TransportasiDocument40 pagesElastisitas Dan Sensitivitas Demand: Mata Kuliah: Ekonomi TransportasipramudyadhePas encore d'évaluation

- R14 - Topics in Demand and Supply AnalysisDocument11 pagesR14 - Topics in Demand and Supply AnalysisGayathri22394Pas encore d'évaluation

- Managerial Economics: An Analysis of Business IssuesDocument16 pagesManagerial Economics: An Analysis of Business IssuesJeanPas encore d'évaluation

- Solution Manual For Managerial Economics 12th Edition Christopher Thomas S Charles MauriceDocument24 pagesSolution Manual For Managerial Economics 12th Edition Christopher Thomas S Charles MauriceAshleyThompsonjzrb100% (46)

- Elasticity From WikiDocument19 pagesElasticity From WikiAravind PillaiPas encore d'évaluation

- Sensitivity of Travel DemandDocument6 pagesSensitivity of Travel DemandShilpa AglurPas encore d'évaluation

- Change The DemandDocument3 pagesChange The DemandLinh ThuỳPas encore d'évaluation

- Micro Economics SlidesDocument77 pagesMicro Economics SlidessnuichPas encore d'évaluation

- Consumer Equilibrium and DemandDocument33 pagesConsumer Equilibrium and DemandAishwarya MishraPas encore d'évaluation

- Elasticityofdemandandsupply 090309123105 Phpapp01Document31 pagesElasticityofdemandandsupply 090309123105 Phpapp01Joshua AsucroPas encore d'évaluation

- Elasticity of Demand & SupplyDocument41 pagesElasticity of Demand & SupplyAbhay BaraPas encore d'évaluation

- ECON 201 Lecture 1Document21 pagesECON 201 Lecture 1SquishyPoopPas encore d'évaluation

- Understand Elasticity of DemandDocument36 pagesUnderstand Elasticity of DemandMahek Anwar AliPas encore d'évaluation

- Group 8 Report DEMANDDocument22 pagesGroup 8 Report DEMANDMa'am Roma GualbertoPas encore d'évaluation

- Elasticity 1Document13 pagesElasticity 1nervasmith21Pas encore d'évaluation

- Economics4 Elasticity ShortDocument20 pagesEconomics4 Elasticity ShortAnimation & PuzzlesPas encore d'évaluation

- Lecture 11 Consumer SurplusDocument17 pagesLecture 11 Consumer SurplusPreeti SubudhiPas encore d'évaluation

- Demand Theory: Dr. Smita ShuklaDocument46 pagesDemand Theory: Dr. Smita ShuklaAmey HamandPas encore d'évaluation

- Short Answer QuestionsDocument7 pagesShort Answer QuestionsmustafaPas encore d'évaluation

- Price, Income and Cross ElasticityDocument28 pagesPrice, Income and Cross ElasticityGurJot SandhuPas encore d'évaluation

- Elasticity of Demand and Types of DemandDocument8 pagesElasticity of Demand and Types of Demanddeepa_kamalim1722Pas encore d'évaluation

- Chap 6 ElasticityDocument26 pagesChap 6 ElasticityShivkarthik G SPas encore d'évaluation

- Demand Curve Characteristics and FactorsDocument4 pagesDemand Curve Characteristics and Factorsmises55Pas encore d'évaluation

- Module 1 - Topics in Demand and Supply Analysis - HandoutsDocument15 pagesModule 1 - Topics in Demand and Supply Analysis - HandoutsAyman Al HakimPas encore d'évaluation

- Demand ElasticityDocument48 pagesDemand ElasticitySaurabh MehrotraPas encore d'évaluation

- Elasticities Applications of Supply Demand AnalysisDocument30 pagesElasticities Applications of Supply Demand AnalysisHafiz bbaPas encore d'évaluation

- Elasticity and Its Application: Dr.B.Venkatraja Associate Professor-SDMIMDDocument33 pagesElasticity and Its Application: Dr.B.Venkatraja Associate Professor-SDMIMDRishikesh DargudePas encore d'évaluation

- Elasticity: - Dr. Shubhada A. JoshiDocument20 pagesElasticity: - Dr. Shubhada A. JoshiVijay KhandarePas encore d'évaluation

- Chapter 2 Theory of Demand BBMDocument5 pagesChapter 2 Theory of Demand BBMPaamir ShresthaPas encore d'évaluation

- ECO 101 Principles of Microeconomics: Lecturer: Dr. Joshua SebuDocument47 pagesECO 101 Principles of Microeconomics: Lecturer: Dr. Joshua SebuYimer FentawPas encore d'évaluation

- ElasticityDocument39 pagesElasticitymd sitab aliPas encore d'évaluation

- Individual Demand and ElasticityDocument34 pagesIndividual Demand and ElasticityAGRAWAL UTKARSHPas encore d'évaluation

- Learning Objectives: Chapter 2: Demand, Supply, and Market EquilibriumDocument25 pagesLearning Objectives: Chapter 2: Demand, Supply, and Market EquilibriumGileah ZuasolaPas encore d'évaluation

- Economics Chapter 4Document14 pagesEconomics Chapter 4Sharif HassanPas encore d'évaluation

- Problem Sheet 06 ADocument1 pageProblem Sheet 06 ARashmi SahooPas encore d'évaluation

- Aimcat 1202Document19 pagesAimcat 1202Rashmi SahooPas encore d'évaluation

- Solutions Assignment-2Document8 pagesSolutions Assignment-2Rashmi SahooPas encore d'évaluation

- Problem Sheet 05Document2 pagesProblem Sheet 05Rashmi SahooPas encore d'évaluation

- Aimcat 1203Document12 pagesAimcat 1203Rashmi SahooPas encore d'évaluation

- CRT Solid LiqdDocument13 pagesCRT Solid LiqdRashmi SahooPas encore d'évaluation

- Problem Sheet 08Document2 pagesProblem Sheet 08Rashmi SahooPas encore d'évaluation

- Problem Sheet 06 BDocument1 pageProblem Sheet 06 BRashmi SahooPas encore d'évaluation

- Problem Sheet 08Document2 pagesProblem Sheet 08Rashmi SahooPas encore d'évaluation

- CRT Solid LiqdDocument13 pagesCRT Solid LiqdRashmi SahooPas encore d'évaluation

- CHE S402 Chapter5 Rate Equations For Fluid Solid Reactions Kinetic ModelsPart1Document6 pagesCHE S402 Chapter5 Rate Equations For Fluid Solid Reactions Kinetic ModelsPart1Rashmi SahooPas encore d'évaluation

- Activated Carbon Filteration PDFDocument50 pagesActivated Carbon Filteration PDFashraf refaatPas encore d'évaluation

- Problem Sheet 07Document4 pagesProblem Sheet 07Rashmi SahooPas encore d'évaluation

- CHE S402 Chapter5 Rate Equations For Fluid Solid Reactions Kinetic ModelsPart2Document9 pagesCHE S402 Chapter5 Rate Equations For Fluid Solid Reactions Kinetic ModelsPart2Rashmi SahooPas encore d'évaluation

- Diversion Headworks: CEL351: Design of Hydraulic StructuresDocument78 pagesDiversion Headworks: CEL351: Design of Hydraulic StructuresAlvaro Rodrigo Chavez Viveros100% (1)

- Surveying Module 6 Tacheometric SurveyingDocument52 pagesSurveying Module 6 Tacheometric SurveyingRashmi SahooPas encore d'évaluation

- 18.construction Ecology KibertDocument15 pages18.construction Ecology KibertSanshrit SinghaiPas encore d'évaluation

- JRF Qror QRB 2019Document8 pagesJRF Qror QRB 2019Rashmi SahooPas encore d'évaluation

- Human Population GrowthDocument14 pagesHuman Population GrowthRashmi SahooPas encore d'évaluation

- Hydrological Measurements: Thom BogaardDocument23 pagesHydrological Measurements: Thom BogaardRashmi SahooPas encore d'évaluation

- 19.hazardous Waste CharacterizationDocument42 pages19.hazardous Waste CharacterizationRashmi SahooPas encore d'évaluation

- India-Eu Environment Forum Hazardous Waste Management in India: An Overview 'Document42 pagesIndia-Eu Environment Forum Hazardous Waste Management in India: An Overview 'shree_soni92Pas encore d'évaluation

- 21.HTRA Risk AssessmentDocument27 pages21.HTRA Risk AssessmentRashmi SahooPas encore d'évaluation

- Building Acoustics and Noise Control by Prof - RamachandraiahDocument35 pagesBuilding Acoustics and Noise Control by Prof - RamachandraiahRashmi SahooPas encore d'évaluation

- Hydrological Measurements: Wim LuxemburgDocument6 pagesHydrological Measurements: Wim LuxemburgRashmi SahooPas encore d'évaluation

- 2.5 Hydraulic Design of Urban Drainage SystemsDocument42 pages2.5 Hydraulic Design of Urban Drainage SystemsRashmi SahooPas encore d'évaluation

- Traffic Flow Theory & Simulation Lecture: Introduction to Shockwave TheoryDocument41 pagesTraffic Flow Theory & Simulation Lecture: Introduction to Shockwave TheoryChiranjaya HulangamuwaPas encore d'évaluation

- Lateral Driving Behaviour Theory and SimulationDocument60 pagesLateral Driving Behaviour Theory and SimulationRashmi SahooPas encore d'évaluation

- Pedestrian Flow TheoryDocument94 pagesPedestrian Flow TheoryRashmi SahooPas encore d'évaluation

- Interaction Between Wastewater Collection and Treatment PDFDocument23 pagesInteraction Between Wastewater Collection and Treatment PDFRashmi SahooPas encore d'évaluation

- Quiz 3. (2) Adjusting Entries - Attempt ReviewDocument11 pagesQuiz 3. (2) Adjusting Entries - Attempt ReviewErika Yasto100% (2)

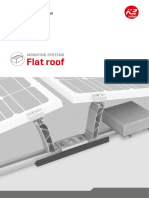

- Support PV systems for flat roofsDocument28 pagesSupport PV systems for flat roofsoctavvvianPas encore d'évaluation

- Satip H 002 02Document10 pagesSatip H 002 02Rijwan MohammadPas encore d'évaluation

- CS - Programmation Mai 2017Document14 pagesCS - Programmation Mai 2017Munezero Jean de DieuPas encore d'évaluation

- Module 5 - Far - Activity-Answer KEYDocument2 pagesModule 5 - Far - Activity-Answer KEYRhadzmae OmalPas encore d'évaluation

- Daniel Romualdez AirportDocument8 pagesDaniel Romualdez AirportMariz PorlayPas encore d'évaluation

- Format of Bottlers NepalDocument12 pagesFormat of Bottlers NepalReya TaujalePas encore d'évaluation

- Scarcity and Opportunity Cost: The Economic ProblemDocument10 pagesScarcity and Opportunity Cost: The Economic ProblemElise Smoll (Elise)Pas encore d'évaluation

- Duns Numbers For - Fed and OregonDocument11 pagesDuns Numbers For - Fed and OregonSotiris Christou100% (1)

- GOVERNANCE PRELIM QUIZ MergedDocument147 pagesGOVERNANCE PRELIM QUIZ MergedSofia SantosPas encore d'évaluation

- Preparation of Financial Statements-Sole TradersDocument5 pagesPreparation of Financial Statements-Sole TradersHeavens Mupedzisa100% (1)

- Bollinger Bands Essentials 1Document13 pagesBollinger Bands Essentials 1Kiran KudtarkarPas encore d'évaluation

- Concept Map 2Document8 pagesConcept Map 2mike raninPas encore d'évaluation

- A25 Highway Drawing Volume 25.03.22 67Document1 pageA25 Highway Drawing Volume 25.03.22 67Monjit GogoiPas encore d'évaluation

- Tax Invoice/Retail Invoice: OptivalDocument1 pageTax Invoice/Retail Invoice: Optivalrangasamy.tnstcPas encore d'évaluation

- Carrefour S.A.Document10 pagesCarrefour S.A.sjc1789Pas encore d'évaluation

- Lecture 2 Notes IDocument23 pagesLecture 2 Notes I林靖雯Pas encore d'évaluation

- To Get More Videos of All Subjects: ShareDocument50 pagesTo Get More Videos of All Subjects: ShareMridul UpadhyayPas encore d'évaluation

- Assignment AccDocument47 pagesAssignment Acchakimstars2003Pas encore d'évaluation

- GKInvest New Account Types 2022Document1 pageGKInvest New Account Types 2022AJI PANGESTUPas encore d'évaluation

- Schedule Pelatihan Powerindo 2023Document40 pagesSchedule Pelatihan Powerindo 2023Bhinnekaborneo mandiriPas encore d'évaluation

- GCSE History Class Note Russian RevolutionDocument4 pagesGCSE History Class Note Russian RevolutionCrystal DonfackPas encore d'évaluation

- 10 Ijetmr18 A05 381Document9 pages10 Ijetmr18 A05 381Koushik SahaPas encore d'évaluation

- NTS GAT Subject Test Sample Paper of Management SciencesDocument9 pagesNTS GAT Subject Test Sample Paper of Management SciencesubillPas encore d'évaluation

- Multinational Business Finance - MiniCase-Chapter 12Document21 pagesMultinational Business Finance - MiniCase-Chapter 12Khoa HuỳnhPas encore d'évaluation

- Final Exam: Dual Degree Programme - DDPDocument16 pagesFinal Exam: Dual Degree Programme - DDPHoàng Vũ HuyPas encore d'évaluation

- JDP Introduction - Rev 3 - 04 Dec 2019Document24 pagesJDP Introduction - Rev 3 - 04 Dec 2019TeatimerobPas encore d'évaluation

- Joe Mark P. Salvadora BSED FILIPINO 1 Contemporary ACTIVITYDocument4 pagesJoe Mark P. Salvadora BSED FILIPINO 1 Contemporary ACTIVITYJoe Mark Periabras SalvadoraPas encore d'évaluation

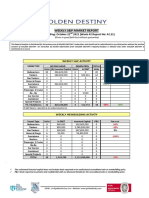

- Weekly S&P and Newbuilding Market Report SummaryDocument7 pagesWeekly S&P and Newbuilding Market Report SummarySandesh Tukaram GhandatPas encore d'évaluation

- International Business The Challenges of Globalization 5th Edition Wild Test BankDocument25 pagesInternational Business The Challenges of Globalization 5th Edition Wild Test BankStephenBowenbxtm100% (50)