Vous aimerez peut-être aussi

- Major Energy SourcesDocument60 pagesMajor Energy SourcesAshish ChaurasiaPas encore d'évaluation

- 140723-d1s2 IndoDocument9 pages140723-d1s2 IndoGinting BerthPas encore d'évaluation

- Bio-Fuels: The BackdropDocument22 pagesBio-Fuels: The Backdropjivitesh YadavPas encore d'évaluation

- Ieo 2020Document7 pagesIeo 2020Riandy PutraPas encore d'évaluation

- Highlight of RUEN - Ver EnglishDocument15 pagesHighlight of RUEN - Ver EnglishLuthfieSangKaptenPas encore d'évaluation

- Energy Usage Trends PPT (Lecture - 2)Document14 pagesEnergy Usage Trends PPT (Lecture - 2)tesfayregs gebretsadik100% (1)

- Lecture 1 - Introduction and Overview - BDocument93 pagesLecture 1 - Introduction and Overview - BkEWQ 865kPas encore d'évaluation

- Chairperson, PNGRB (080110)Document44 pagesChairperson, PNGRB (080110)Sainu KalathingalPas encore d'évaluation

- BS Simon MinerbapabumDocument15 pagesBS Simon MinerbapabumDadanPas encore d'évaluation

- P10 Steven GustDocument37 pagesP10 Steven GustRaka BachtiaraPas encore d'évaluation

- E85: Future Gasoline Substitute Fuel TechnologyDocument45 pagesE85: Future Gasoline Substitute Fuel Technologyapi-26678889Pas encore d'évaluation

- Journal Pre-Proof: Current Opinion in Green and Sustainable ChemistryDocument24 pagesJournal Pre-Proof: Current Opinion in Green and Sustainable ChemistryNestor Armando Marin SolanoPas encore d'évaluation

- Week One World Energy Demand and SupplyDocument43 pagesWeek One World Energy Demand and SupplyJosé Miguel Pajares TorresPas encore d'évaluation

- Annual Energy Outlook 2021 (AEO2021) : U.S. Energy Information AdministrationDocument21 pagesAnnual Energy Outlook 2021 (AEO2021) : U.S. Energy Information AdministrationLusy UciePas encore d'évaluation

- Lecture - 1 - Es - 2 - Petchem - 2021 - Objectives of Petrochemistry, Raw Materials, Products, Relationship Among Petchemand Other Industrial SectorsDocument44 pagesLecture - 1 - Es - 2 - Petchem - 2021 - Objectives of Petrochemistry, Raw Materials, Products, Relationship Among Petchemand Other Industrial SectorsCarlos francisco PerézPas encore d'évaluation

- JORGE PAUL DELMONTE Presentação Evento Bolivia Inglês - RevFinalDocument42 pagesJORGE PAUL DELMONTE Presentação Evento Bolivia Inglês - RevFinallucmontPas encore d'évaluation

- ICCT Comments Renewable Fuel Standard Program Rvo Noda 20171019Document5 pagesICCT Comments Renewable Fuel Standard Program Rvo Noda 20171019The International Council on Clean TransportationPas encore d'évaluation

- Alternative Fuels PowerpointDocument24 pagesAlternative Fuels PowerpointNARESHA RPas encore d'évaluation

- Study Id13642 Energy-Prices-WorldwideDocument40 pagesStudy Id13642 Energy-Prices-WorldwideBel NochuPas encore d'évaluation

- Exxonmobil / Xto Merger: R.W. Tillerson and D.S. RosenthalDocument22 pagesExxonmobil / Xto Merger: R.W. Tillerson and D.S. Rosenthalmattlams100% (1)

- International Energy Outlook 2021 (IEO2021) : U.S. Energy Information AdministrationDocument21 pagesInternational Energy Outlook 2021 (IEO2021) : U.S. Energy Information AdministrationMercedesPas encore d'évaluation

- Global Energy Demand and Carbon Emissions: Primary Energy Consumption CO Emissions From Energy UseDocument18 pagesGlobal Energy Demand and Carbon Emissions: Primary Energy Consumption CO Emissions From Energy UseNishith GuptaPas encore d'évaluation

- Annual Energy Outlook 2021 (AEO2021) : U.S. Energy Information AdministrationDocument21 pagesAnnual Energy Outlook 2021 (AEO2021) : U.S. Energy Information AdministrationJunaid ArsahdPas encore d'évaluation

- 2022 Eotm Energy PaperDocument49 pages2022 Eotm Energy PaperFiliaAltheaPas encore d'évaluation

- Sustainable Energy Eco-SystemsDocument83 pagesSustainable Energy Eco-Systemserwin seraficaPas encore d'évaluation

- Biofuel Production by Country - Region and Fuel Type, 2016-2022 - Charts - Data & Statistics - IEADocument3 pagesBiofuel Production by Country - Region and Fuel Type, 2016-2022 - Charts - Data & Statistics - IEAgjhPas encore d'évaluation

- Annual Energy Outlook 2022: With Projections To 2050 Chart LibraryDocument16 pagesAnnual Energy Outlook 2022: With Projections To 2050 Chart LibrarySCAP SADECVPas encore d'évaluation

- Oil and Gas Sustainability StrategiesDocument67 pagesOil and Gas Sustainability StrategiesctprimaPas encore d'évaluation

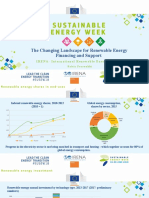

- The Changing Landscape For RE Financing and Support R FerroukhiDocument14 pagesThe Changing Landscape For RE Financing and Support R Ferroukhikarikalcholan mayavanPas encore d'évaluation

- Cheng 2020Document17 pagesCheng 2020ptashko1986Pas encore d'évaluation

- Flightpaths Biojetffuel PDFDocument18 pagesFlightpaths Biojetffuel PDFНиколай РулевPas encore d'évaluation

- Government Regulation in The Development of Nre in IndonesiaDocument21 pagesGovernment Regulation in The Development of Nre in IndonesiaNina KonitatPas encore d'évaluation

- 13 47 749294 BPStatisticalReviewofWorldEnergy-Brussels September2008 PDFDocument37 pages13 47 749294 BPStatisticalReviewofWorldEnergy-Brussels September2008 PDFyoesseoyPas encore d'évaluation

- Pyrolysis Oil To Gasoline-Final: R Marinangelli G Ellis E Boldingh R Bain S Cabanban D Hsu Z Fei DC ElliottDocument295 pagesPyrolysis Oil To Gasoline-Final: R Marinangelli G Ellis E Boldingh R Bain S Cabanban D Hsu Z Fei DC ElliottLindsey BondPas encore d'évaluation

- E - Overview of The Vietnamese Energy Sector - EREADocument17 pagesE - Overview of The Vietnamese Energy Sector - EREAnamakPas encore d'évaluation

- Power Choices Power ChoicesDocument19 pagesPower Choices Power Choicesapi-25935701Pas encore d'évaluation

- MLT Out Look 2023 EditionDocument46 pagesMLT Out Look 2023 EditionhambaliPas encore d'évaluation

- World Energy Outlook 2008 Key GraphsDocument12 pagesWorld Energy Outlook 2008 Key GraphsJonathan MouettePas encore d'évaluation

- Case For GTL - ShellDocument28 pagesCase For GTL - ShellFahim AbidiPas encore d'évaluation

- S&P-Platts Webinar H2 18MAR2020Document32 pagesS&P-Platts Webinar H2 18MAR2020Prith HarasgamaPas encore d'évaluation

- Climbers Scale BP HeadquartersDocument69 pagesClimbers Scale BP HeadquartersProtect Florida's BeachesPas encore d'évaluation

- Chapter 3: Literature Review: A. Feedstock Waste Cooking OilDocument4 pagesChapter 3: Literature Review: A. Feedstock Waste Cooking OilPriyankaPas encore d'évaluation

- Role of Ongc in The India's Road Map For Energy SecurityDocument65 pagesRole of Ongc in The India's Road Map For Energy SecuritynanimbaPas encore d'évaluation

- 2 Energy Vision Pak MZDocument20 pages2 Energy Vision Pak MZbitf03m030100% (2)

- Key World Energy Statistics 2020Document81 pagesKey World Energy Statistics 2020Amin DehghaniPas encore d'évaluation

- IEA G20 Hydrogen Report: AssumptionsDocument14 pagesIEA G20 Hydrogen Report: Assumptionspragya89Pas encore d'évaluation

- Fuel Cells For A Sustainable Energy FutureDocument51 pagesFuel Cells For A Sustainable Energy Futuregreen707Pas encore d'évaluation

- Characterization of Waste Frying Oils Obtained From Different FacilitiesDocument7 pagesCharacterization of Waste Frying Oils Obtained From Different FacilitiesAhmed SajitPas encore d'évaluation

- China DME OutlookDocument31 pagesChina DME OutlookRamaOktavianPas encore d'évaluation

- Review of Gas Based Power Technologies - Gas Turbines: Robin W. AmesDocument37 pagesReview of Gas Based Power Technologies - Gas Turbines: Robin W. AmesAndri YantoPas encore d'évaluation

- Spencer Dale: Group Chief EconomistDocument32 pagesSpencer Dale: Group Chief EconomistRonal Stepan HarianjaPas encore d'évaluation

- Energy and Greenhouse Gas Emissions Effects of Fuel EthanolDocument12 pagesEnergy and Greenhouse Gas Emissions Effects of Fuel EthanolGlorie Mae BurerosPas encore d'évaluation

- Opportunities and Challenges For Solar PV Rooftop in IndonesiaDocument24 pagesOpportunities and Challenges For Solar PV Rooftop in IndonesiaIskandarPas encore d'évaluation

- Results and Outlook: February 2021Document55 pagesResults and Outlook: February 2021Nicolas RoulleauPas encore d'évaluation

- Bernhard Meyhofer Potential BarriersDocument15 pagesBernhard Meyhofer Potential BarriersSaqib AliPas encore d'évaluation

- BP Energy Outlook 2017 Presentation SlidesDocument34 pagesBP Energy Outlook 2017 Presentation SlidesLindsey BondPas encore d'évaluation

- Future Energy Outlook Special Report (16 September 2021)Document7 pagesFuture Energy Outlook Special Report (16 September 2021)Videsh RamsahaiPas encore d'évaluation

- Environmental Impact of Energy Strategies Within the EEC: A Report Prepared for the Environment and Consumer Protection, Service of the Commission of the European CommunitiesD'EverandEnvironmental Impact of Energy Strategies Within the EEC: A Report Prepared for the Environment and Consumer Protection, Service of the Commission of the European CommunitiesPas encore d'évaluation

- Financing Solutions to Reduce Natural Gas Flaring and Methane EmissionsD'EverandFinancing Solutions to Reduce Natural Gas Flaring and Methane EmissionsÉvaluation : 5 sur 5 étoiles5/5 (1)

- Effluent Operator JobDocument1 pageEffluent Operator JobQing JyulyanPas encore d'évaluation

- ThesisDocument190 pagesThesisAliRazaSattar100% (1)

- Shannon Diversity IndexDocument2 pagesShannon Diversity IndexlinubinoyPas encore d'évaluation

- Perhitungan Unit Alat PlambingDocument19 pagesPerhitungan Unit Alat PlambingMuhammad Iqbal NovantaPas encore d'évaluation

- NAP Company ProfileDocument13 pagesNAP Company Profilesameer sahaanPas encore d'évaluation

- STP Calculation NS - 2200Document42 pagesSTP Calculation NS - 2200Anandaraju Saminathan67% (3)

- Target Indicator: Targets IndicatorsDocument4 pagesTarget Indicator: Targets IndicatorsRashiqah RazlanPas encore d'évaluation

- Note Guidance Use Stability Testing Human Medicinal Products - en PDFDocument3 pagesNote Guidance Use Stability Testing Human Medicinal Products - en PDFcindi saputriPas encore d'évaluation

- Bush Fire Danger Period and Fire Permits - NSW Rural Fire ServiceDocument2 pagesBush Fire Danger Period and Fire Permits - NSW Rural Fire ServiceJames CurryPas encore d'évaluation

- ISO AgricultureDocument24 pagesISO AgricultureKatiePas encore d'évaluation

- GEOS3340 S2 2019 - FinalExam - RESCHEDULEDDocument10 pagesGEOS3340 S2 2019 - FinalExam - RESCHEDULEDAnthony KiemPas encore d'évaluation

- CMR - QuarryDocument9 pagesCMR - Quarryaldrin mamaril0% (1)

- Journal of Environmental Economics and Management: Ralph MastromonacoDocument17 pagesJournal of Environmental Economics and Management: Ralph MastromonacoBayu Pramana PutraPas encore d'évaluation

- Comparision of AZF Jacobs TechnologyDocument23 pagesComparision of AZF Jacobs Technologyসাইদুর রহমানPas encore d'évaluation

- DeforestationDocument24 pagesDeforestationGufran Shaikh60% (5)

- 3-5-đã chuyển đổiDocument10 pages3-5-đã chuyển đổiHải Yến ĐoànPas encore d'évaluation

- NRCS-CB Vetiver FactsheetDocument2 pagesNRCS-CB Vetiver FactsheetSaran KumarPas encore d'évaluation

- Case Digest: Title of The Case: MMDA v. Concern Citizens of Manila BayDocument2 pagesCase Digest: Title of The Case: MMDA v. Concern Citizens of Manila Bayjoey artem torresPas encore d'évaluation

- E-PFwBetzDearbornAE1125 ENDocument2 pagesE-PFwBetzDearbornAE1125 ENindahpsPas encore d'évaluation

- ANIL-FINAL Climate Change - Emerging Challenges For Sustainable DevelopmentDocument21 pagesANIL-FINAL Climate Change - Emerging Challenges For Sustainable DevelopmentanilbarikPas encore d'évaluation

- Different Issues or Challenges Affecting Tourism in The PhilippinesDocument2 pagesDifferent Issues or Challenges Affecting Tourism in The PhilippinesAl-juffrey Luis AmilhamjaPas encore d'évaluation

- GHG Emissions Related To Freshwater ReservoirsDocument166 pagesGHG Emissions Related To Freshwater ReservoirsSantiago Flores AlonsoPas encore d'évaluation

- Floraxx TopDocument6 pagesFloraxx TopSnezana MitrovicPas encore d'évaluation

- 0001Document36 pages0001Googool YPas encore d'évaluation

- Relatório SternDocument613 pagesRelatório SternANDI Agencia de Noticias do Direito da Infancia100% (2)

- Air Pollution ChemistryDocument25 pagesAir Pollution Chemistryjanice omadtoPas encore d'évaluation

- SUMMATIVE TEST Climate Answer KeyDocument2 pagesSUMMATIVE TEST Climate Answer KeyCarissa Mae Cañete100% (3)

- TI - GB5749-2006 Standards For Drinking Water QualityDocument16 pagesTI - GB5749-2006 Standards For Drinking Water QualityRegional Economic Cooperation and Integration (RCI) in Asia67% (3)

- House Designs, QHC, 1959Document64 pagesHouse Designs, QHC, 1959House Histories92% (13)

- Xcel EmailDocument2 pagesXcel EmailRob PortPas encore d'évaluation