Vous aimerez peut-être aussi

- ACI Diploma Sample QuestionsDocument7 pagesACI Diploma Sample Questionsattractram100% (1)

- Unified Compliance Framework The Ultimate Step-By-Step GuideD'EverandUnified Compliance Framework The Ultimate Step-By-Step GuidePas encore d'évaluation

- Summary and Analysis of Never Split the Difference:: Negotiating As If Your Life Depended On ItD'EverandSummary and Analysis of Never Split the Difference:: Negotiating As If Your Life Depended On ItPas encore d'évaluation

- Chapter 12Document15 pagesChapter 12cnd1982Pas encore d'évaluation

- PWC Consumer Lending RadarDocument34 pagesPWC Consumer Lending RadarNaveen TandanPas encore d'évaluation

- Aci - The Financial Markets Association: Examination FormulaeDocument8 pagesAci - The Financial Markets Association: Examination FormulaeJovan SsenkandwaPas encore d'évaluation

- Finmar FormulaDocument2 pagesFinmar FormulaCPAs AccountPas encore d'évaluation

- Complete Strategic Financial Management FormulaeDocument39 pagesComplete Strategic Financial Management FormulaePrashanth Yadhav100% (2)

- FormulaDocument4 pagesFormulaZIKIE CHOYPas encore d'évaluation

- Formula Sheet PDFDocument3 pagesFormula Sheet PDFmadhav1111Pas encore d'évaluation

- Bonds and Their Valuation FormulasDocument1 pageBonds and Their Valuation FormulasGabrielle VaporPas encore d'évaluation

- Công thức IM tự luận- cho finalDocument6 pagesCông thức IM tự luận- cho finalTuấn NguyễnPas encore d'évaluation

- Finalexam - Financial Management FicheDocument6 pagesFinalexam - Financial Management FicheLouis BarbierPas encore d'évaluation

- Financial FormulasDocument2 pagesFinancial FormulasCoreyPas encore d'évaluation

- FM 2555 FinalDocument28 pagesFM 2555 Finalguowen liPas encore d'évaluation

- BEC CPA Formulas November 2015 Becker CPA Review PDFDocument20 pagesBEC CPA Formulas November 2015 Becker CPA Review PDFsasyedaPas encore d'évaluation

- 1+totalchange 1+ Actual Change 1change PriceDocument3 pages1+totalchange 1+ Actual Change 1change PriceMit DavePas encore d'évaluation

- FORMULA SHEET For Final - FMDocument1 pageFORMULA SHEET For Final - FMNajia SiddiquiPas encore d'évaluation

- Exam 1 Formula SheetDocument3 pagesExam 1 Formula SheetYingfanPas encore d'évaluation

- Chap 2: 1. CF (A) OCF - Capital Spending - 2. CF (B) Debt Service - Long-Term DebtDocument5 pagesChap 2: 1. CF (A) OCF - Capital Spending - 2. CF (B) Debt Service - Long-Term DebtTRANG NGUYỄN LÊ QUỲNHPas encore d'évaluation

- النسب المالية - إنجليزىDocument5 pagesالنسب المالية - إنجليزىMohamed Ahmed YassinPas encore d'évaluation

- Study Unit 2Document20 pagesStudy Unit 2pphelokazi54Pas encore d'évaluation

- Reviewer-Stock ValuationDocument7 pagesReviewer-Stock ValuationSheira Mae GuzmanPas encore d'évaluation

- SFM Formulas Sheet For Quick Revision Before ExamDocument28 pagesSFM Formulas Sheet For Quick Revision Before ExamKamakshi AdadadiPas encore d'évaluation

- S4 Valuation Online VersionDocument52 pagesS4 Valuation Online Versionconstruction omanPas encore d'évaluation

- RSM430 Final Cheat SheetDocument1 pageRSM430 Final Cheat SheethappyPas encore d'évaluation

- Sample Level 1 Wiley Formula Sheets PDFDocument10 pagesSample Level 1 Wiley Formula Sheets PDFMuhammed RafiudeenPas encore d'évaluation

- HKEAA Formula of Financial RatiosDocument1 pageHKEAA Formula of Financial RatiosEvanna ChungPas encore d'évaluation

- CF ResumeDocument2 pagesCF ResumejoanalinPas encore d'évaluation

- Ca Final SFM ChalisaDocument44 pagesCa Final SFM ChalisaSarabjeet SinghPas encore d'évaluation

- Study Unit 2Document19 pagesStudy Unit 2Irfaan CassimPas encore d'évaluation

- RecipeDocument4 pagesRecipesasyedaPas encore d'évaluation

- MM L1 Formula SheetDocument20 pagesMM L1 Formula SheetMlungisi MalazaPas encore d'évaluation

- Financial Market Problems and FormulasDocument3 pagesFinancial Market Problems and FormulasNufayl KatoPas encore d'évaluation

- Topic 7-ValuationDocument36 pagesTopic 7-ValuationK60 Nguyễn Ngọc Quế AnhPas encore d'évaluation

- Lecture Notes CH 2Document22 pagesLecture Notes CH 2Bobby WilliamsPas encore d'évaluation

- FM Formula Sheet - Not GivenDocument4 pagesFM Formula Sheet - Not GivenSophie ChopraPas encore d'évaluation

- 1 FV Annuity C× 1+r - 1 R FV Annuity $100,000 C 1 1 1+r - 1 1.004868 - 1 R 0.004868 $615.47 Per Month.Document2 pages1 FV Annuity C× 1+r - 1 R FV Annuity $100,000 C 1 1 1+r - 1 1.004868 - 1 R 0.004868 $615.47 Per Month.nino nakashidzePas encore d'évaluation

- asset-v1-IMF+FMAx+1T2017+type@asset+block@FMAx M1 CLEAN NewDocument42 pagesasset-v1-IMF+FMAx+1T2017+type@asset+block@FMAx M1 CLEAN NewBURUNDI1Pas encore d'évaluation

- Bộ Đề Speaking Part 1 Winter 2016 - Version 01Document53 pagesBộ Đề Speaking Part 1 Winter 2016 - Version 01Eli LiPas encore d'évaluation

- Feedback and Warm-Up Review: - Feedback of Your Requests - Cash Flow - Cash Flow Diagrams - Economic EquivalenceDocument30 pagesFeedback and Warm-Up Review: - Feedback of Your Requests - Cash Flow - Cash Flow Diagrams - Economic EquivalenceSajid IqbalPas encore d'évaluation

- Corp Fin 3Document25 pagesCorp Fin 3Nguyễn GiangPas encore d'évaluation

- Finance BECDocument8 pagesFinance BECJon LeinsPas encore d'évaluation

- Finman FormulasDocument11 pagesFinman FormulasArnelli GregorioPas encore d'évaluation

- Async CFin-I Annuities and Perpetuities Friday 5august2022Document35 pagesAsync CFin-I Annuities and Perpetuities Friday 5august2022SSPas encore d'évaluation

- CA Aaditya Jain: With Sunrise You RiseDocument48 pagesCA Aaditya Jain: With Sunrise You RiseAnand JhaPas encore d'évaluation

- Ch. 5 The Time Value of Money: 5.1. Future Values and Compound InterestDocument2 pagesCh. 5 The Time Value of Money: 5.1. Future Values and Compound InterestShahid NaseemPas encore d'évaluation

- UNIT 2 Time and Money RelationshipDocument79 pagesUNIT 2 Time and Money Relationshipcuajohnpaull.schoolbackup.002Pas encore d'évaluation

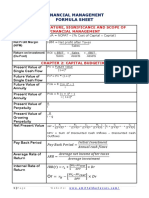

- Financial Management Formula Sheet: Chapter 1: Nature, Significance and Scope of Financial ManagementDocument6 pagesFinancial Management Formula Sheet: Chapter 1: Nature, Significance and Scope of Financial ManagementEilen Joyce Bisnar100% (1)

- Ratio Analysis Formula GuideDocument2 pagesRatio Analysis Formula GuideMuhammed KhalidPas encore d'évaluation

- Chapter 2 1 Determination of Interest RatesDocument63 pagesChapter 2 1 Determination of Interest RatesLâm Bulls100% (1)

- Chapter 2 - How To Calculate Present ValuesDocument36 pagesChapter 2 - How To Calculate Present ValuesDeok NguyenPas encore d'évaluation

- Formula Sheet-2nd QuizDocument6 pagesFormula Sheet-2nd QuizEge MelihPas encore d'évaluation

- CA Final SFM New Syllabus Full Chalisa Book by Aaditya Jain SirDocument48 pagesCA Final SFM New Syllabus Full Chalisa Book by Aaditya Jain SirYedu KrishnanPas encore d'évaluation

- Notes Cfa Fixed Income R41Document30 pagesNotes Cfa Fixed Income R41Ayah AkPas encore d'évaluation

- Fin2704X Formula Sheet PDFDocument2 pagesFin2704X Formula Sheet PDFwwwPas encore d'évaluation

- The Meaning of Interest RatesDocument23 pagesThe Meaning of Interest RatesThảo NhiPas encore d'évaluation

- Operating Cash Flow Per Share (Net Income + Depreciation + Amortization) / Common Shares OutstandingDocument5 pagesOperating Cash Flow Per Share (Net Income + Depreciation + Amortization) / Common Shares OutstandingzacchariahPas encore d'évaluation

- A Project Report On Indian Capital MarkeDocument85 pagesA Project Report On Indian Capital MarkeZeeshan KhanPas encore d'évaluation

- Slum Clearance and RedevelopmentDocument7 pagesSlum Clearance and RedevelopmentAnwar SalahadinPas encore d'évaluation

- Chapter 1 Corporation and Corporate GovernanceDocument32 pagesChapter 1 Corporation and Corporate GovernanceWellaPas encore d'évaluation

- Carlos v. Mindoro SugarDocument6 pagesCarlos v. Mindoro Sugarvmanalo16Pas encore d'évaluation

- An Overview of Financial Management: Multiple Choice: ConceptualDocument15 pagesAn Overview of Financial Management: Multiple Choice: ConceptualApril Isidro0% (1)

- ASF AgendaDocument23 pagesASF Agendaank333Pas encore d'évaluation

- 10 Years For 50% Ownership 10 Years With Interest Rate of 5%Document5 pages10 Years For 50% Ownership 10 Years With Interest Rate of 5%Every Drop CountsPas encore d'évaluation

- Financial Scandals and The Role of Private Enforcement PDFDocument59 pagesFinancial Scandals and The Role of Private Enforcement PDFJonathan RubinPas encore d'évaluation

- Financial Instruments - IllustrationsDocument12 pagesFinancial Instruments - Illustrationszynga1457Pas encore d'évaluation

- Derivatives and Public Debt Management Rivatives and Public Debt Management Gustavo PigaDocument150 pagesDerivatives and Public Debt Management Rivatives and Public Debt Management Gustavo Pigapaul embleyPas encore d'évaluation

- Kimmel Acct 7e Ch10 Reporting and Analyzing LiabilitiesDocument97 pagesKimmel Acct 7e Ch10 Reporting and Analyzing LiabilitiesElectronPas encore d'évaluation

- VUL Mock Exam 2 (October 2018)Document11 pagesVUL Mock Exam 2 (October 2018)Alona Villamor Chanco100% (1)

- Mutual FundDocument27 pagesMutual FundDinesh sawPas encore d'évaluation

- 2020 Cost of Capital Practitioners Guide External - v031Document25 pages2020 Cost of Capital Practitioners Guide External - v031Баир ДамбаевPas encore d'évaluation

- Lesson 4 Stocks and Bonds 1Document11 pagesLesson 4 Stocks and Bonds 1Adriel MaglaquiPas encore d'évaluation

- MBA Exam 1 Spring 2010 PDFDocument6 pagesMBA Exam 1 Spring 2010 PDFAnonymous JmeZ95P0Pas encore d'évaluation

- Prelim Exam-Banking and Financial Institution-March 2020Document4 pagesPrelim Exam-Banking and Financial Institution-March 2020Richard Oliver CortezPas encore d'évaluation

- LYons Bond Case SolutionDocument2 pagesLYons Bond Case SolutionGautam Sethi75% (4)

- Bond Price Volatility: Dr. Himanshu Joshi FORE School of Management New DelhiDocument51 pagesBond Price Volatility: Dr. Himanshu Joshi FORE School of Management New Delhiashishbansal85Pas encore d'évaluation

- (Problems) - Audit of InvestmentsDocument17 pages(Problems) - Audit of Investmentsapatos50% (6)

- General Mathematics Reviewer s1 q2Document5 pagesGeneral Mathematics Reviewer s1 q2lancono86Pas encore d'évaluation

- PNB Metlife 2015-16Document44 pagesPNB Metlife 2015-16khannasankalpPas encore d'évaluation

- Candidate Information FormDocument3 pagesCandidate Information FormRainy RustPas encore d'évaluation

- Revision Notes Book Corporate Finance Chapter 1 18Document15 pagesRevision Notes Book Corporate Finance Chapter 1 18Yashrajsing LuckkanaPas encore d'évaluation

- Thesis On Credit Rating Agencies in IndiaDocument5 pagesThesis On Credit Rating Agencies in IndiaPaySomeoneToWriteMyPaperSingapore100% (2)

- Test Bank For Investments 9th Canadian by BodieDocument32 pagesTest Bank For Investments 9th Canadian by BodieMonica Sanchez100% (32)

- Flinder Valves and Controls Inc. - WorksheetsDocument22 pagesFlinder Valves and Controls Inc. - WorksheetsBach Cao50% (4)

- 3.1. Basic Puzzles About Financial Structure Around The WorldDocument75 pages3.1. Basic Puzzles About Financial Structure Around The WorldNhatty WeroPas encore d'évaluation

- Module 5 - Interests Formula and RatesDocument14 pagesModule 5 - Interests Formula and RatesAnna HansenPas encore d'évaluation

- Bond Valuation PDFDocument5 pagesBond Valuation PDFGibson ZimbaPas encore d'évaluation