Vous aimerez peut-être aussi

- Structured Financial Product A Complete Guide - 2020 EditionD'EverandStructured Financial Product A Complete Guide - 2020 EditionPas encore d'évaluation

- The Advanced Fixed Income and Derivatives Management GuideD'EverandThe Advanced Fixed Income and Derivatives Management GuidePas encore d'évaluation

- Essays in Derivatives: Risk-Transfer Tools and Topics Made EasyD'EverandEssays in Derivatives: Risk-Transfer Tools and Topics Made EasyPas encore d'évaluation

- Bonds Are Not Forever: The Crisis Facing Fixed Income InvestorsD'EverandBonds Are Not Forever: The Crisis Facing Fixed Income InvestorsPas encore d'évaluation

- Quantitative Equity Investing: Techniques and StrategiesD'EverandQuantitative Equity Investing: Techniques and StrategiesÉvaluation : 4 sur 5 étoiles4/5 (1)

- Problems and Solutions in Mathematical Finance, Volume 2: Equity DerivativesD'EverandProblems and Solutions in Mathematical Finance, Volume 2: Equity DerivativesPas encore d'évaluation

- CLO Investing: With an Emphasis on CLO Equity & BB NotesD'EverandCLO Investing: With an Emphasis on CLO Equity & BB NotesPas encore d'évaluation

- Fixed Income and Interest Rate Derivative AnalysisD'EverandFixed Income and Interest Rate Derivative AnalysisPas encore d'évaluation

- Portfolio Representations: A step-by-step guide to representing value, exposure and risk for fixed income, equity, FX and derivativesD'EverandPortfolio Representations: A step-by-step guide to representing value, exposure and risk for fixed income, equity, FX and derivativesÉvaluation : 5 sur 5 étoiles5/5 (1)

- The Sterling Bonds and Fixed Income Handbook: A practical guide for investors and advisersD'EverandThe Sterling Bonds and Fixed Income Handbook: A practical guide for investors and advisersÉvaluation : 5 sur 5 étoiles5/5 (1)

- The Handbook of Credit Risk Management: Originating, Assessing, and Managing Credit ExposuresD'EverandThe Handbook of Credit Risk Management: Originating, Assessing, and Managing Credit ExposuresPas encore d'évaluation

- The Management of Bond Investments and Trading of DebtD'EverandThe Management of Bond Investments and Trading of DebtPas encore d'évaluation

- Alternative Investment Strategies A Complete Guide - 2020 EditionD'EverandAlternative Investment Strategies A Complete Guide - 2020 EditionPas encore d'évaluation

- Understanding Credit Derivatives and Related InstrumentsD'EverandUnderstanding Credit Derivatives and Related InstrumentsÉvaluation : 4.5 sur 5 étoiles4.5/5 (2)

- Financial Risk Modelling and Portfolio Optimization with RD'EverandFinancial Risk Modelling and Portfolio Optimization with RÉvaluation : 4 sur 5 étoiles4/5 (2)

- Alternative Investments Complete Self-Assessment GuideD'EverandAlternative Investments Complete Self-Assessment GuidePas encore d'évaluation

- Introduction to Fixed Income Analytics: Relative Value Analysis, Risk Measures and ValuationD'EverandIntroduction to Fixed Income Analytics: Relative Value Analysis, Risk Measures and ValuationPas encore d'évaluation

- Portfolio and Investment Analysis with SAS: Financial Modeling Techniques for OptimizationD'EverandPortfolio and Investment Analysis with SAS: Financial Modeling Techniques for OptimizationÉvaluation : 3 sur 5 étoiles3/5 (1)

- Pricing and Hedging Interest and Credit Risk Sensitive InstrumentsD'EverandPricing and Hedging Interest and Credit Risk Sensitive InstrumentsPas encore d'évaluation

- Strategic Asset Allocation in Fixed Income Markets: A Matlab Based User's GuideD'EverandStrategic Asset Allocation in Fixed Income Markets: A Matlab Based User's GuidePas encore d'évaluation

- Advanced Bond Portfolio Management: Best Practices in Modeling and StrategiesD'EverandAdvanced Bond Portfolio Management: Best Practices in Modeling and StrategiesPas encore d'évaluation

- Value at Risk and Bank Capital Management: Risk Adjusted Performances, Capital Management and Capital Allocation Decision MakingD'EverandValue at Risk and Bank Capital Management: Risk Adjusted Performances, Capital Management and Capital Allocation Decision MakingPas encore d'évaluation

- CLO Liquidity Provision and the Volcker Rule: Implications on the Corporate Bond MarketD'EverandCLO Liquidity Provision and the Volcker Rule: Implications on the Corporate Bond MarketPas encore d'évaluation

- Practical Portfolio Performance Measurement and AttributionD'EverandPractical Portfolio Performance Measurement and AttributionÉvaluation : 3.5 sur 5 étoiles3.5/5 (2)

- Managed Futures for Institutional Investors: Analysis and Portfolio ConstructionD'EverandManaged Futures for Institutional Investors: Analysis and Portfolio ConstructionPas encore d'évaluation

- The New Science of Asset Allocation: Risk Management in a Multi-Asset WorldD'EverandThe New Science of Asset Allocation: Risk Management in a Multi-Asset WorldPas encore d'évaluation

- Managing Downside Risk in Financial MarketsD'EverandManaging Downside Risk in Financial MarketsÉvaluation : 3 sur 5 étoiles3/5 (1)

- Yield Curve Modeling and Forecasting: The Dynamic Nelson-Siegel ApproachD'EverandYield Curve Modeling and Forecasting: The Dynamic Nelson-Siegel ApproachÉvaluation : 4 sur 5 étoiles4/5 (2)

- Financial Risk Management: A Practitioner's Guide to Managing Market and Credit RiskD'EverandFinancial Risk Management: A Practitioner's Guide to Managing Market and Credit RiskÉvaluation : 2.5 sur 5 étoiles2.5/5 (2)

- How to Invest in Structured Products: A Guide for Investors and Asset ManagersD'EverandHow to Invest in Structured Products: A Guide for Investors and Asset ManagersPas encore d'évaluation

- Corporate Bonds and Structured Financial ProductsD'EverandCorporate Bonds and Structured Financial ProductsÉvaluation : 5 sur 5 étoiles5/5 (1)

- Forecasting Expected Returns in the Financial MarketsD'EverandForecasting Expected Returns in the Financial MarketsÉvaluation : 4.5 sur 5 étoiles4.5/5 (2)

- Insider's Guide to Fixed Income Securities & MarketsD'EverandInsider's Guide to Fixed Income Securities & MarketsÉvaluation : 5 sur 5 étoiles5/5 (1)

- Mortgage-Backed Securities: Products, Structuring, and Analytical TechniquesD'EverandMortgage-Backed Securities: Products, Structuring, and Analytical TechniquesPas encore d'évaluation

- C++ for Financial Engineers Complete Self-Assessment GuideD'EverandC++ for Financial Engineers Complete Self-Assessment GuidePas encore d'évaluation

- Continuous-Time Models in Corporate Finance, Banking, and Insurance: A User's GuideD'EverandContinuous-Time Models in Corporate Finance, Banking, and Insurance: A User's GuidePas encore d'évaluation

- Interest Rate Markets: A Practical Approach to Fixed IncomeD'EverandInterest Rate Markets: A Practical Approach to Fixed IncomeÉvaluation : 4 sur 5 étoiles4/5 (2)

- Handbook of Basel III Capital: Enhancing Bank Capital in PracticeD'EverandHandbook of Basel III Capital: Enhancing Bank Capital in PracticePas encore d'évaluation

- Investment Performance Measurement: Evaluating and Presenting ResultsD'EverandInvestment Performance Measurement: Evaluating and Presenting ResultsPhilip Lawton, CIPMÉvaluation : 1 sur 5 étoiles1/5 (1)

- The Econometrics of Individual Risk: Credit, Insurance, and MarketingD'EverandThe Econometrics of Individual Risk: Credit, Insurance, and MarketingPas encore d'évaluation

- Fixed Income Markets: Management, Trading and HedgingD'EverandFixed Income Markets: Management, Trading and HedgingPas encore d'évaluation

- Positive Alpha Generation: Designing Sound Investment ProcessesD'EverandPositive Alpha Generation: Designing Sound Investment ProcessesPas encore d'évaluation

- Derivatives and Risk Management JP Morgan ReportDocument24 pagesDerivatives and Risk Management JP Morgan Reportanirbanccim8493Pas encore d'évaluation

- Evaluating and Hedging Exotic Swap Instruments Via LGMDocument33 pagesEvaluating and Hedging Exotic Swap Instruments Via LGMalexandergirPas encore d'évaluation

- JPMorgan Guide To Credit DerivativesDocument88 pagesJPMorgan Guide To Credit Derivativesl_lidiyaPas encore d'évaluation

- CV DR Rituparna DasDocument8 pagesCV DR Rituparna DasCRMD JodhpurPas encore d'évaluation

- Continuous Test On Project FinanceDocument1 pageContinuous Test On Project FinanceCRMD JodhpurPas encore d'évaluation

- Continuous Test 4: Principles and Practice of BankingDocument5 pagesContinuous Test 4: Principles and Practice of BankingCRMD JodhpurPas encore d'évaluation

- Continuous Test 4: Principles and Practice of BankingDocument5 pagesContinuous Test 4: Principles and Practice of BankingCRMD JodhpurPas encore d'évaluation

- Project List MBA (Ins)Document1 pageProject List MBA (Ins)CRMD JodhpurPas encore d'évaluation

- Instructions: Write Your Roll Number On The Top of The Question Paper Do NotDocument20 pagesInstructions: Write Your Roll Number On The Top of The Question Paper Do NotCRMD JodhpurPas encore d'évaluation

- Instructions: Answer Any Two. Supplement Your Answer With Practical Examples Wherever Possible. All Questions Carry Equal MarksDocument1 pageInstructions: Answer Any Two. Supplement Your Answer With Practical Examples Wherever Possible. All Questions Carry Equal MarksCRMD JodhpurPas encore d'évaluation

- The Financial Markets, MoneyDocument8 pagesThe Financial Markets, MoneyNirmal ShresthaPas encore d'évaluation

- Vi. Manipulation, Fraud, and Insider Trading Manipulation of Security Prices Devices and PracticesDocument9 pagesVi. Manipulation, Fraud, and Insider Trading Manipulation of Security Prices Devices and PracticesJasfher CallejoPas encore d'évaluation

- Model Test Papers For BCSMDocument16 pagesModel Test Papers For BCSMnikhil_kankariaPas encore d'évaluation

- Operational Case Study Prototype Answers Variant 1: Task 1Document8 pagesOperational Case Study Prototype Answers Variant 1: Task 1MyDustbin2010Pas encore d'évaluation

- Financial MarketsDocument32 pagesFinancial MarketsEmil BabiloniaPas encore d'évaluation

- How To Record IFRS 16 LeaseDocument24 pagesHow To Record IFRS 16 Leasehur hussainPas encore d'évaluation

- Coronavirus SME Survey Instrument EnglishDocument6 pagesCoronavirus SME Survey Instrument EnglishnganduPas encore d'évaluation

- Financial DerivativesDocument4 pagesFinancial DerivativesnomanPas encore d'évaluation

- Natura Annual Report 2011Document134 pagesNatura Annual Report 2011Tibério AraújoPas encore d'évaluation

- Fin Mar Ce 910Document29 pagesFin Mar Ce 910moriary artPas encore d'évaluation

- Transmamerica FFIUL Client BrochureDocument24 pagesTransmamerica FFIUL Client BrochuredjdazedPas encore d'évaluation

- Series 7 Suitability Exercise SecuredDocument28 pagesSeries 7 Suitability Exercise SecuredAnthony Mcnichols100% (1)

- Treasury MGTDocument21 pagesTreasury MGTVikram MendaPas encore d'évaluation

- Beaumont vs. Prieto., 41 Phil. 670, No. 8988 March 30, 1916Document42 pagesBeaumont vs. Prieto., 41 Phil. 670, No. 8988 March 30, 1916Elizabeth Jade D. CalaorPas encore d'évaluation

- PruLink Surrender Form PDFDocument4 pagesPruLink Surrender Form PDFHui Jia JunnPas encore d'évaluation

- Share Based Compensation Cheat SheetDocument2 pagesShare Based Compensation Cheat SheetJanePas encore d'évaluation

- Carter J - Using Voodoo Lines-1 PDFDocument34 pagesCarter J - Using Voodoo Lines-1 PDFShabir Rizwan0% (1)

- PGDM II FINANCE ElectivesDocument21 pagesPGDM II FINANCE ElectivesSonia BhagwatPas encore d'évaluation

- Triple Profit Winner Users GuideDocument15 pagesTriple Profit Winner Users GuideNik RazmanPas encore d'évaluation

- Kanpur Confectionries Private Limited (A)Document10 pagesKanpur Confectionries Private Limited (A)GS0402Pas encore d'évaluation

- Practice Questions MDocument18 pagesPractice Questions MYilin YANGPas encore d'évaluation

- Corporate Finance GlossaryDocument10 pagesCorporate Finance Glossaryanmol2590Pas encore d'évaluation

- Equity Variance Swaps With Dividends OpenGammaDocument13 pagesEquity Variance Swaps With Dividends OpenGammamshchetkPas encore d'évaluation

- Australian Interest Rate SwaptionsDocument4 pagesAustralian Interest Rate SwaptionsOMiNYCPas encore d'évaluation

- Late Delivery of Hull From Top CrestDocument3 pagesLate Delivery of Hull From Top Crestsnjanani04Pas encore d'évaluation

- Pathfinders Stock Market Training - Online Course PDFDocument3 pagesPathfinders Stock Market Training - Online Course PDFGarv JainPas encore d'évaluation

- Interesting Thesis Topics FinanceDocument5 pagesInteresting Thesis Topics FinanceTracy Drey100% (2)

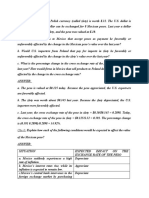

- Câu 5: Assume That The Polish Currency (Called Zloty) Is Worth $.32. The U.S. Dollar IsDocument4 pagesCâu 5: Assume That The Polish Currency (Called Zloty) Is Worth $.32. The U.S. Dollar IsQuốc HuyPas encore d'évaluation

- Derivatives Note SeminarDocument7 pagesDerivatives Note SeminarCA Vikas NevatiaPas encore d'évaluation

- Structured Products SummaryDocument28 pagesStructured Products Summaryfwm949fwxrPas encore d'évaluation