Vous aimerez peut-être aussi

- Unclaimed Balances Law, Dormant Accounts, Etc.Document4 pagesUnclaimed Balances Law, Dormant Accounts, Etc.Maria Lena HuecasPas encore d'évaluation

- Atty. WBC - Data PrivacyDocument7 pagesAtty. WBC - Data PrivacyWarren Barrameda ConcepcionPas encore d'évaluation

- Atty. WBC - Credit Information System ActDocument9 pagesAtty. WBC - Credit Information System ActWarren Barrameda ConcepcionPas encore d'évaluation

- Atty. WBC - Financial LeasingDocument4 pagesAtty. WBC - Financial LeasingWarren Barrameda ConcepcionPas encore d'évaluation

- Atty. WBC - Personal Property Security ActDocument2 pagesAtty. WBC - Personal Property Security ActWarren Barrameda ConcepcionPas encore d'évaluation

- Unclaimed Balances Law, Dormant Accounts, Etc.Document4 pagesUnclaimed Balances Law, Dormant Accounts, Etc.Maria Lena HuecasPas encore d'évaluation

- Atty. WBC - Financial LeasingDocument4 pagesAtty. WBC - Financial LeasingWarren Barrameda ConcepcionPas encore d'évaluation

- McKEE vs. IACDocument29 pagesMcKEE vs. IACWarren Barrameda ConcepcionPas encore d'évaluation

- Personal LawDocument1 pagePersonal LawWarren Barrameda ConcepcionPas encore d'évaluation

- PIL Case DigestDocument13 pagesPIL Case DigestWarren Barrameda ConcepcionPas encore d'évaluation

- CARLDocument1 pageCARLWarren Barrameda ConcepcionPas encore d'évaluation

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (120)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Firth, Raymond (Ed.) (1964) Capital, Savings and Credit in Peasant Societies (Só o Índice!)Document2 pagesFirth, Raymond (Ed.) (1964) Capital, Savings and Credit in Peasant Societies (Só o Índice!)Felipe SilvaPas encore d'évaluation

- Resume of SirducdinhDocument1 pageResume of Sirducdinhapi-25690844Pas encore d'évaluation

- Kanlaon Vs NLRCDocument3 pagesKanlaon Vs NLRCJade Belen Zaragoza0% (2)

- LP BrochureDocument2 pagesLP BrochureSyed Abdul RafeyPas encore d'évaluation

- Greenberg-Megaworld Demand LetterDocument2 pagesGreenberg-Megaworld Demand LetterLilian RoquePas encore d'évaluation

- Paper 3 of JAIIB Is Legal and Regulatory Aspects of BankingDocument3 pagesPaper 3 of JAIIB Is Legal and Regulatory Aspects of BankingDhiraj PatrePas encore d'évaluation

- A Final Board Packet August 7, 2013 - 0.... 5Document199 pagesA Final Board Packet August 7, 2013 - 0.... 5نيرمين احمدPas encore d'évaluation

- Ch. 4: Financial Forecasting, Planning, and BudgetingDocument41 pagesCh. 4: Financial Forecasting, Planning, and BudgetingFahmia Winata8Pas encore d'évaluation

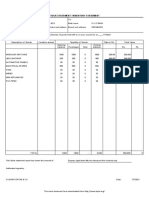

- Stock Statement Format For Bank LoanDocument1 pageStock Statement Format For Bank Loanpsycho Neha40% (5)

- Synopsis Self-Sustainable CommunityDocument3 pagesSynopsis Self-Sustainable Communityankitankit yadavPas encore d'évaluation

- La Part 3 PDFDocument23 pagesLa Part 3 PDFShubhaPas encore d'évaluation

- Revised Withholding Tax TablesDocument2 pagesRevised Withholding Tax TablesReylan San PascualPas encore d'évaluation

- Business StudiesDocument2 pagesBusiness StudiesSonal JhaPas encore d'évaluation

- Wells Fargo Everyday CheckingDocument6 pagesWells Fargo Everyday CheckingDavid Dali Rojas Huamanchau100% (1)

- Jun 16 Bill-AnandDocument1 pageJun 16 Bill-AnandanandPas encore d'évaluation

- Syllabus DUDocument67 pagesSyllabus DUMohit GoyalPas encore d'évaluation

- Katalog Akitaka Opory Dvigatelya 2017-2018Document223 pagesKatalog Akitaka Opory Dvigatelya 2017-2018Alexey KolmakovPas encore d'évaluation

- Ethics DigestDocument29 pagesEthics DigestTal Migallon100% (1)

- Indirect Impact of GST On Income TaxDocument14 pagesIndirect Impact of GST On Income TaxNAMAN KANSALPas encore d'évaluation

- Berkshire Blueprint 2.0Document82 pagesBerkshire Blueprint 2.0iBerkshires.com100% (1)

- Game Theory (2) - Mechanism Design With TransfersDocument60 pagesGame Theory (2) - Mechanism Design With Transfersjm15yPas encore d'évaluation

- Thurstone Interest Test by Marie ReyDocument9 pagesThurstone Interest Test by Marie Reymarie annPas encore d'évaluation

- Case Study 18 PresentationDocument11 pagesCase Study 18 PresentationZara KhanPas encore d'évaluation

- List of Topics For A Research Paper EconomicsDocument4 pagesList of Topics For A Research Paper Economicstitamyg1p1j2100% (1)

- Collection of Pitch Decks From Venture Capital Funded StartupsDocument22 pagesCollection of Pitch Decks From Venture Capital Funded StartupsAlan Petzold50% (2)

- Assessment of The Kosovo Innovation SystemDocument113 pagesAssessment of The Kosovo Innovation SystemOECD Global RelationsPas encore d'évaluation

- Holly Tree 2015 990taxDocument21 pagesHolly Tree 2015 990taxstan rawlPas encore d'évaluation

- Global Batrch 11Document57 pagesGlobal Batrch 11mohanPas encore d'évaluation

- The Fundamentals of Managerial Economics: Mcgraw-Hill/IrwinDocument33 pagesThe Fundamentals of Managerial Economics: Mcgraw-Hill/IrwinRanyDAmandaPas encore d'évaluation

- GM OEM Financials Dgi9ja-2Document1 pageGM OEM Financials Dgi9ja-2Dananjaya GokhalePas encore d'évaluation