Vous aimerez peut-être aussi

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- Hybrid Vehicle ToyotaDocument30 pagesHybrid Vehicle ToyotaAdf TrendPas encore d'évaluation

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

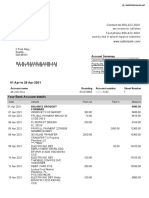

- Sutton Bank StatementDocument2 pagesSutton Bank StatementNadiia AvetisianPas encore d'évaluation

- IRS Document 6209 Manual (2003 Ed.)Document0 pageIRS Document 6209 Manual (2003 Ed.)iamnumber8Pas encore d'évaluation

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Day Trading StrategiesDocument3 pagesDay Trading Strategiesswetha reddy100% (2)

- IB Economics SL8 - Overall Economic ActivityDocument6 pagesIB Economics SL8 - Overall Economic ActivityTerran100% (1)

- Volvo Trucks CaseDocument33 pagesVolvo Trucks Caseravichauhan18100% (3)

- SaleDocument1 pageSaleMegan HerreraPas encore d'évaluation

- Dear Nanay: How This Story of A Little Girl and Her OFW Mother Came To Be, by Zarah GagatigaDocument3 pagesDear Nanay: How This Story of A Little Girl and Her OFW Mother Came To Be, by Zarah GagatigaMarkchester Cerezo100% (1)

- Ayushman Bharat NewDocument21 pagesAyushman Bharat NewburhanPas encore d'évaluation

- Education and Social DevelopmentDocument30 pagesEducation and Social DevelopmentMichelleAlejandroPas encore d'évaluation

- Greenberg-Megaworld Demand LetterDocument2 pagesGreenberg-Megaworld Demand LetterLilian RoquePas encore d'évaluation

- Tax Invoice GJ1181910 AK79503Document3 pagesTax Invoice GJ1181910 AK79503AnkitPas encore d'évaluation

- Postpaid Monthly Statement: This Month's SummaryDocument8 pagesPostpaid Monthly Statement: This Month's SummaryAVINASH KUMBARPas encore d'évaluation

- Green Coffee FOB, C & F, CIF Contract: Specialty Coffee Association of AmericaDocument4 pagesGreen Coffee FOB, C & F, CIF Contract: Specialty Coffee Association of AmericacoffeepathPas encore d'évaluation

- Inflation AccountingDocument9 pagesInflation AccountingyasheshgaglaniPas encore d'évaluation

- Macroeconomics - Assignment IIDocument6 pagesMacroeconomics - Assignment IIRahul Thapa MagarPas encore d'évaluation

- Folder Gründen in Wien Englisch Web 6-10-17Document6 pagesFolder Gründen in Wien Englisch Web 6-10-17rodicabaltaPas encore d'évaluation

- Special Economic ZoneDocument7 pagesSpecial Economic ZoneAnonymous cRMw8feac8Pas encore d'évaluation

- Acceptance Payment Form: Tax Amnesty On DelinquenciesDocument1 pageAcceptance Payment Form: Tax Amnesty On DelinquenciesJennyMariedeLeonPas encore d'évaluation

- UAS MS NathanaelCahya 115190307Document2 pagesUAS MS NathanaelCahya 115190307Nathanael CahyaPas encore d'évaluation

- Biznis Plan MLIN EngDocument16 pagesBiznis Plan MLIN EngBoris ZecPas encore d'évaluation

- DELIVERY Transfer of Risk and Transfer of TitleDocument2 pagesDELIVERY Transfer of Risk and Transfer of TitleLesterPas encore d'évaluation

- Black and Gold Gala - On WebDocument1 pageBlack and Gold Gala - On Webapi-670861250Pas encore d'évaluation

- A Cost Model of Industrial Maintenance For Profitability Analysis and Benchmarking PDFDocument17 pagesA Cost Model of Industrial Maintenance For Profitability Analysis and Benchmarking PDFHugoCabanillasPas encore d'évaluation

- Case Study 3 NirmaDocument9 pagesCase Study 3 NirmaPravin DhoblePas encore d'évaluation

- Aggregate Demand and Aggregate Supply PDFDocument18 pagesAggregate Demand and Aggregate Supply PDFAsif WarsiPas encore d'évaluation

- At 5906 Audit ReportDocument11 pagesAt 5906 Audit ReportZyl Diez MagnoPas encore d'évaluation

- Sarvodaya Public School Azamgarh Class - XI Annual Examination Subject - EconomicsDocument4 pagesSarvodaya Public School Azamgarh Class - XI Annual Examination Subject - EconomicsAshraf JamalPas encore d'évaluation

- 0 Wage TheoriesDocument13 pages0 Wage Theoriessatyam.pmir6789Pas encore d'évaluation

- Fidelity Bond Form Attachment BDocument9 pagesFidelity Bond Form Attachment BLucelyn Yruma TurtonaPas encore d'évaluation