Vous aimerez peut-être aussi

- 5 Disbursements 1Document199 pages5 Disbursements 1John Karl Mabini100% (1)

- Johnson Tax Statement 10.22.18Document2 pagesJohnson Tax Statement 10.22.18Andrew KochPas encore d'évaluation

- JNTUH Delivery ReportDocument72 pagesJNTUH Delivery ReportSrinu GattuPas encore d'évaluation

- List of Live Kua2018Document66 pagesList of Live Kua2018Yogesh ChhaprooPas encore d'évaluation

- Japan Based Investment BanksDocument36 pagesJapan Based Investment BanksSiddharth JoshiPas encore d'évaluation

- NGO Partnership SystemDocument3 pagesNGO Partnership Systemarun_trikha7530Pas encore d'évaluation

- Kanban System For Toyota Outbound LogisticsDocument2 pagesKanban System For Toyota Outbound LogisticsDebopriyo RoyPas encore d'évaluation

- List of Empanelled RIs Uttar Pradesh State PDFDocument2 pagesList of Empanelled RIs Uttar Pradesh State PDFVishal Pratap SinghPas encore d'évaluation

- Bihar State Power (Holding) Company Limited Directory-2013-1Document106 pagesBihar State Power (Holding) Company Limited Directory-2013-1sonukarma321Pas encore d'évaluation

- Gujarat Based DetailsDocument21 pagesGujarat Based DetailsAnil BhatiaPas encore d'évaluation

- Vendor Enlistment For FY 207980Document20 pagesVendor Enlistment For FY 207980Ankita RawatPas encore d'évaluation

- Sponsorship For Mrs. UniverseDocument2 pagesSponsorship For Mrs. UniverseKate PestanasPas encore d'évaluation

- Website All CA-PACS Till Nov-2018 (90 Nos)Document13 pagesWebsite All CA-PACS Till Nov-2018 (90 Nos)Donor CrewPas encore d'évaluation

- About Us and SessionsDocument3 pagesAbout Us and SessionsNithin BabuPas encore d'évaluation

- LC Copy - Ef-004 2021 - Vikohasan - 6X40'FT - 3hochiminh 3haiphongDocument4 pagesLC Copy - Ef-004 2021 - Vikohasan - 6X40'FT - 3hochiminh 3haiphongKhaerul FazriPas encore d'évaluation

- Directory Uttipec (TT Centre) : As On 13.11.2009Document29 pagesDirectory Uttipec (TT Centre) : As On 13.11.2009abhishekchhabra_69Pas encore d'évaluation

- High Sea SalesDocument15 pagesHigh Sea SalesdarcyPas encore d'évaluation

- Study of Mobiles WalletsDocument42 pagesStudy of Mobiles WalletsVijay TendolkarPas encore d'évaluation

- Non Rotary SpeakersDocument36 pagesNon Rotary SpeakerskinananthaPas encore d'évaluation

- Port ProceduresDocument50 pagesPort ProceduresPaul Saquido CapiliPas encore d'évaluation

- Imi Brochure 2014 FinalDocument72 pagesImi Brochure 2014 Finalarpit_9688Pas encore d'évaluation

- HrjobsDocument15 pagesHrjobsapi-19473092Pas encore d'évaluation

- Electricity BillDocument1 pageElectricity Billsreeram yadavPas encore d'évaluation

- Accident Insurance CoverDocument24 pagesAccident Insurance Coversantanu40Pas encore d'évaluation

- Aditya Birla Group ProfileDocument4 pagesAditya Birla Group ProfileSarvesh JanotiPas encore d'évaluation

- Edu DelhiDocument12 pagesEdu Delhisheena sondhiPas encore d'évaluation

- List of Participants - Refresher Course - ARCP - October 2021Document16 pagesList of Participants - Refresher Course - ARCP - October 2021PRATIK CHAUHAN100% (1)

- EeeeeeeeeeeeeeDocument266 pagesEeeeeeeeeeeeeeHarshal Joshi100% (1)

- SR Mentor 27 July 2016Document76 pagesSR Mentor 27 July 2016varaPas encore d'évaluation

- NGOs in BangaloreDocument7 pagesNGOs in BangaloreSudhakar GanjikuntaPas encore d'évaluation

- Finance ProfileDocument4 pagesFinance Profilehoney_29Pas encore d'évaluation

- Third Phase With Mentor DetailsDocument1 pageThird Phase With Mentor DetailsGvr MurthyPas encore d'évaluation

- Contact List of SAADocument6 pagesContact List of SAAmantoo kumarPas encore d'évaluation

- Punjab PDFDocument51 pagesPunjab PDFਰੁਪਿੰਦਰ ਸਿੰਘPas encore d'évaluation

- CBA Batch 5 Profile Book 25JAN18 PDFDocument62 pagesCBA Batch 5 Profile Book 25JAN18 PDFhappiness ElemPas encore d'évaluation

- SchoolDocument42 pagesSchoolUpender BhatiPas encore d'évaluation

- Updated List of ArbitratorsDocument89 pagesUpdated List of ArbitratorsAnshu SinghPas encore d'évaluation

- List-II (Validity Till 20th May, 2021)Document4 pagesList-II (Validity Till 20th May, 2021)Garvit TiwariPas encore d'évaluation

- Aparna Western MeadowsDocument9 pagesAparna Western Meadowsa_veerenderPas encore d'évaluation

- Arcil 191121Document3 pagesArcil 191121sudha.KPas encore d'évaluation

- NASSCOM Membership Application - 08-09Document11 pagesNASSCOM Membership Application - 08-09Rohit Dangayach100% (1)

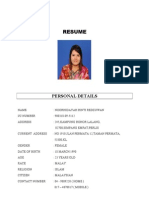

- Resume: Personal DetailsDocument6 pagesResume: Personal DetailssuhanizamPas encore d'évaluation

- BAPL Business Plan & Marketing Road MapDocument58 pagesBAPL Business Plan & Marketing Road MapHemant UpadhyayPas encore d'évaluation

- List of NGOs PDFDocument23 pagesList of NGOs PDFThe Telugu ChannelPas encore d'évaluation

- List of Placement Consultants in HyderabadDocument3 pagesList of Placement Consultants in Hyderabadpattabhi2reddy9841Pas encore d'évaluation

- KVK List in MaharashtraDocument7 pagesKVK List in Maharashtravaibhav_sparsh100% (1)

- Registered NGO List VODocument15 pagesRegistered NGO List VOHarsh AroraPas encore d'évaluation

- Varun Jain 88Document3 pagesVarun Jain 88Neha SinghalPas encore d'évaluation

- Natural Resource Management PDFDocument221 pagesNatural Resource Management PDFSanjeev KumarPas encore d'évaluation

- IIMI CCBMDO Placement Brochure 2016-17Document54 pagesIIMI CCBMDO Placement Brochure 2016-17sanjeetmohantyPas encore d'évaluation

- Study Centres Functioning at Present: Sl. Location TOTAL NO. No. of Study Centres 37Document10 pagesStudy Centres Functioning at Present: Sl. Location TOTAL NO. No. of Study Centres 37Rajat S SahaPas encore d'évaluation

- PAT - List of Sector-Wise Firms - 0Document6 pagesPAT - List of Sector-Wise Firms - 0RohitPas encore d'évaluation

- HNIDocument5 pagesHNIAmrita MishraPas encore d'évaluation

- National Institute of Technology Durgapur: Mahatma Gandhi Avenue, Durgapur 713 209, West Bengal, IndiaDocument2 pagesNational Institute of Technology Durgapur: Mahatma Gandhi Avenue, Durgapur 713 209, West Bengal, IndiavivekPas encore d'évaluation

- Emerging Trends in Information and Communications TechnologyDocument19 pagesEmerging Trends in Information and Communications TechnologyzulPas encore d'évaluation

- JFM Quarterly Result Preview Apr 18 EDEL 2Document16 pagesJFM Quarterly Result Preview Apr 18 EDEL 2Rajesh KumarPas encore d'évaluation

- ProjectX India - 1st November 2020 Issue HighlightsDocument14 pagesProjectX India - 1st November 2020 Issue Highlightssandeep sharmaPas encore d'évaluation

- Curriculum Vitae of Lufuno Donna MphaphuliDocument5 pagesCurriculum Vitae of Lufuno Donna Mphaphulifunim7815Pas encore d'évaluation

- National Council For TeachDocument41 pagesNational Council For Teachসন্দীপ চন্দ্রPas encore d'évaluation

- State Nodel Officers For Direct SellingDocument4 pagesState Nodel Officers For Direct SellingChetan BhardwajPas encore d'évaluation

- Final List of Empanelled Hospitals.1120417Document52 pagesFinal List of Empanelled Hospitals.1120417AkshayKumarPas encore d'évaluation

- Upes Registration LetterDocument25 pagesUpes Registration LetterDon Poul JosePas encore d'évaluation

- Category: Capital, Tier 2: City: Bhubaneswar State: OrissaDocument4 pagesCategory: Capital, Tier 2: City: Bhubaneswar State: OrissaAkshay ChavanPas encore d'évaluation

- Ministers OfficeDocument102 pagesMinisters OfficeDennis LittlePas encore d'évaluation

- Name of Institution Head SL. No. Phone NumberDocument3 pagesName of Institution Head SL. No. Phone NumberMD. NASIF HOSSAIN IMONPas encore d'évaluation

- Portrait of an Industrial City: 'Clanging Belfast' 1750-1914D'EverandPortrait of an Industrial City: 'Clanging Belfast' 1750-1914Pas encore d'évaluation

- B2B MarketingDocument17 pagesB2B Marketingsurbhi rajPas encore d'évaluation

- Credit Annual STMTDocument8 pagesCredit Annual STMTallinoneetmtPas encore d'évaluation

- Lembaga Hasil Dalam Negeri: Inland Revenue BoardDocument20 pagesLembaga Hasil Dalam Negeri: Inland Revenue BoardKen ChiaPas encore d'évaluation

- SMChap 008Document55 pagesSMChap 008Ine100% (2)

- Unit4 AnalysisSpreadsheetDocument135 pagesUnit4 AnalysisSpreadsheetTamar PkhakadzePas encore d'évaluation

- Master AccountingDocument12 pagesMaster Accountingyeshi janexoPas encore d'évaluation

- Bank Reconcialiation ProblemDocument10 pagesBank Reconcialiation ProblemChatlyn Kaye MediavilloPas encore d'évaluation

- Wooden Spoon Cake and PastriesDocument1 pageWooden Spoon Cake and PastriesErika BuenaPas encore d'évaluation

- Annual Subscription Form-1Document2 pagesAnnual Subscription Form-1Ahmed_Rishwan_156100% (1)

- GSI ISSMGE Membership Form 2020-2021Document1 pageGSI ISSMGE Membership Form 2020-2021marketing_925862570Pas encore d'évaluation

- Account Statement From 1 Jul 2022 To 31 Jul 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument6 pagesAccount Statement From 1 Jul 2022 To 31 Jul 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceL JanardanaPas encore d'évaluation

- 030 - InV - Arise (Borescope)Document2 pages030 - InV - Arise (Borescope)Rony YudaPas encore d'évaluation

- High-Speed Rail Freight Sub-Report in Efficient Train Systems For Freight TransportDocument93 pagesHigh-Speed Rail Freight Sub-Report in Efficient Train Systems For Freight Transportwizz33Pas encore d'évaluation

- A Study On Online Payment Methods Among College Students With Special Reference To Christ CollegeDocument60 pagesA Study On Online Payment Methods Among College Students With Special Reference To Christ CollegeAnjaliPas encore d'évaluation

- Computation of Total Income Income From Business or Profession (Chapter IV D) 300000Document4 pagesComputation of Total Income Income From Business or Profession (Chapter IV D) 300000ramanPas encore d'évaluation

- 2312100607329500000Document2 pages2312100607329500000SHRESHTHA COLLEGESPas encore d'évaluation

- 195r-Circular No 12 2022Document7 pages195r-Circular No 12 2022DEVA1985Pas encore d'évaluation

- Shipper' S Letter of InstructionsDocument4 pagesShipper' S Letter of Instructionsmanvendra singhPas encore d'évaluation

- Introduction of Online BankingDocument18 pagesIntroduction of Online BankingRavi Kashyap506Pas encore d'évaluation

- Ross Supply Chain StudyDocument22 pagesRoss Supply Chain StudyKaushik ReddyPas encore d'évaluation

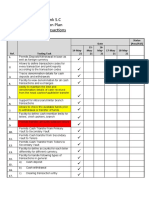

- Zamzam Bank S.C Project Test Action Plan Cash Related TransactionsDocument7 pagesZamzam Bank S.C Project Test Action Plan Cash Related Transactionstofik awelPas encore d'évaluation

- SRM Sem1 Exam Fee ReceiptDocument2 pagesSRM Sem1 Exam Fee Receiptdeeksha6548gkPas encore d'évaluation

- For Claim Registration, Please Call On Toll Free Number 1800 2 666Document4 pagesFor Claim Registration, Please Call On Toll Free Number 1800 2 666RehaanPas encore d'évaluation

- Hindustan Petroleum Corporation Limited Direct Sales Office 130/1, Sarojini Devi Street, Secunderabad - 500 003Document1 pageHindustan Petroleum Corporation Limited Direct Sales Office 130/1, Sarojini Devi Street, Secunderabad - 500 00379LiterPas encore d'évaluation