Vous aimerez peut-être aussi

- Refunds: Chapter - 19Document28 pagesRefunds: Chapter - 19Ashma KhanalPas encore d'évaluation

- PayslipDocument1 pagePayslipAnonymous QYeq3h37Pas encore d'évaluation

- Procter & GambleDocument3 pagesProcter & GambleShawaiz AfzalPas encore d'évaluation

- Good Agriculture Practice (An Approach)Document28 pagesGood Agriculture Practice (An Approach)Robinson GultomPas encore d'évaluation

- InvoiceDocument1 pageInvoiceJanhvii tiwariPas encore d'évaluation

- Facture Apple Store UsDocument2 pagesFacture Apple Store Usmelgayla9Pas encore d'évaluation

- NMR Solvent Data ChartDocument2 pagesNMR Solvent Data ChartNGUYỄN HOÀNG LINHPas encore d'évaluation

- I4g Linkedin ChecklistDocument5 pagesI4g Linkedin ChecklistAdaPas encore d'évaluation

- How Lloyds TSB Achieved Success Under Brian PitmanDocument8 pagesHow Lloyds TSB Achieved Success Under Brian PitmanAmit SrivastavaPas encore d'évaluation

- Infrastructure Development Plan for Chhattisgarh - Road Project Viability OptionsDocument3 pagesInfrastructure Development Plan for Chhattisgarh - Road Project Viability Optionsjavedarzoo50% (2)

- Economics Unit 1 Revision NotesDocument32 pagesEconomics Unit 1 Revision NotesJohn EdwardPas encore d'évaluation

- New Product DevelopmentDocument24 pagesNew Product DevelopmentSaurabh JindalPas encore d'évaluation

- Supply Chain Management Complete Notes - Manoj ShriwasDocument66 pagesSupply Chain Management Complete Notes - Manoj Shriwasshubham singhPas encore d'évaluation

- Podcast Market ResearchDocument12 pagesPodcast Market Researchapi-394443105Pas encore d'évaluation

- QTG Inv Ae 2022 020117Document2 pagesQTG Inv Ae 2022 020117İnsömnia ÇöğPas encore d'évaluation

- Innocentive Solution Submission - Sustainable PackagingDocument7 pagesInnocentive Solution Submission - Sustainable PackagingThomas_S100% (1)

- Eco 101 Question and Answer PDFDocument28 pagesEco 101 Question and Answer PDFOlawale100% (3)

- Design Thinking 1Document46 pagesDesign Thinking 1Andrea A. UribePas encore d'évaluation

- Manual and Simulation Guide Simul8 2011Document363 pagesManual and Simulation Guide Simul8 2011dalmeidanielPas encore d'évaluation

- Tax317 Group Project SSTDocument23 pagesTax317 Group Project SSTNik Syarizal Nik MahadhirPas encore d'évaluation

- GooglepreviewDocument84 pagesGooglepreviewFernando Edward Chambi QuimberPas encore d'évaluation

- Hong Kong Polytechnic University Individual Assignment on Toys City IncDocument15 pagesHong Kong Polytechnic University Individual Assignment on Toys City IncHolly Cheung100% (2)

- Delays at Logan Airport Problem SetDocument4 pagesDelays at Logan Airport Problem Setavadhanam770% (2)

- GG ToysDocument3 pagesGG ToysIzzahIkramIllahiPas encore d'évaluation

- ServitisationDocument32 pagesServitisation256850100% (1)

- Pan-Europa Case Study ProjectsDocument7 pagesPan-Europa Case Study ProjectsBornxlr80% (1)

- SM 06 Innovation & EntrepreneurshipDocument29 pagesSM 06 Innovation & EntrepreneurshipGhighilan AlexandruPas encore d'évaluation

- Value PropositionDocument4 pagesValue PropositionKARAN AGRAWALPas encore d'évaluation

- The Product/Market Fit Canvas: Quick GuideDocument9 pagesThe Product/Market Fit Canvas: Quick GuideJesús AlfredoPas encore d'évaluation

- Nagavara Ramarao Narayana MurthyDocument21 pagesNagavara Ramarao Narayana MurthyRobert AyalaPas encore d'évaluation

- Poel - 2016 - An Ethical Framework For Evaluating Experimental TechnologyDocument20 pagesPoel - 2016 - An Ethical Framework For Evaluating Experimental TechnologyJohnPas encore d'évaluation

- 6 Zero Based BudgetDocument19 pages6 Zero Based BudgetangadsinghmalhanPas encore d'évaluation

- Government Printing GuidelinesDocument10 pagesGovernment Printing GuidelinesYash Nagar0% (1)

- Delays at Logan Group B3Document20 pagesDelays at Logan Group B3Shubham Agnihotri100% (1)

- Mark 3054 SlidesDocument121 pagesMark 3054 SlidesJessy ParkPas encore d'évaluation

- A Study of Analysis and Trends For Embedded Business Intelligence MarketDocument9 pagesA Study of Analysis and Trends For Embedded Business Intelligence MarketIJRASETPublicationsPas encore d'évaluation

- SOUTH KOREA'S DAIRY MARKET OFFERS POTENTIAL FOR TH TRUE MILKDocument43 pagesSOUTH KOREA'S DAIRY MARKET OFFERS POTENTIAL FOR TH TRUE MILKLê Thị ThảoPas encore d'évaluation

- MGMT and Leadership 704-2Document9 pagesMGMT and Leadership 704-2SyedEshaqueSirajPas encore d'évaluation

- International Journal of Economics and Financial IssuesDocument9 pagesInternational Journal of Economics and Financial IssuesAfifahPas encore d'évaluation

- BCG Matrix Template Docx ToolsheroDocument1 pageBCG Matrix Template Docx ToolsheroShubham KumarPas encore d'évaluation

- SSRN Id3177534 PDFDocument11 pagesSSRN Id3177534 PDFRajesh LalPas encore d'évaluation

- His Is A Full Class Attendance at The First Day of Class Is MandatoryDocument11 pagesHis Is A Full Class Attendance at The First Day of Class Is MandatoryChaucer19100% (1)

- SDL Trados Studio 2011 - AdvancedDocument35 pagesSDL Trados Studio 2011 - AdvancedPreda AndreiPas encore d'évaluation

- Con Club - Fms Delhi: Online Induction Learning - Batch 2021 - Activity 3Document3 pagesCon Club - Fms Delhi: Online Induction Learning - Batch 2021 - Activity 3tusharsinghal94Pas encore d'évaluation

- Zero Based BudgetingDocument15 pagesZero Based Budgetingdp021Pas encore d'évaluation

- The 3CDocument4 pagesThe 3CPankaj KumarPas encore d'évaluation

- Grower Resume ExamplesDocument8 pagesGrower Resume Examplesafaydoter100% (2)

- There's No Such Thing As Big Data in HRDocument5 pagesThere's No Such Thing As Big Data in HRDapo TaiwoPas encore d'évaluation

- AMAZON Case StudyDocument2 pagesAMAZON Case StudyAbid KhanPas encore d'évaluation

- Guy Kawasaki's The Art of InnovationDocument6 pagesGuy Kawasaki's The Art of InnovationAdrien Katsuya TatenoPas encore d'évaluation

- The Worst Error in Strategy Is To Compete With Rivals On Same DimensionsDocument43 pagesThe Worst Error in Strategy Is To Compete With Rivals On Same DimensionsmayankPas encore d'évaluation

- DDS Overview - HighlightsDocument2 pagesDDS Overview - HighlightsBreakingDefensePas encore d'évaluation

- Equity ValuationDocument18 pagesEquity ValuationsharmilaPas encore d'évaluation

- Independent Institute of Lay Adventists of KigaliDocument75 pagesIndependent Institute of Lay Adventists of KigalimshabPas encore d'évaluation

- A Comparative Study On The Effect of Marketing Techniques of Volkswagen and ToyotaDocument92 pagesA Comparative Study On The Effect of Marketing Techniques of Volkswagen and ToyotaPranshu Sahni100% (3)

- Automation - Not A Job KillerDocument80 pagesAutomation - Not A Job KillerpoimartiPas encore d'évaluation

- BMG Case StudyDocument5 pagesBMG Case Studynwakah100% (1)

- International Business RESIT Summative Assessment BriefDocument12 pagesInternational Business RESIT Summative Assessment BriefSahibzada Abu Bakar GhayyurPas encore d'évaluation

- Descriptive Analytics: Machine Learning For Dummies, IBM Limited EditionDocument1 pageDescriptive Analytics: Machine Learning For Dummies, IBM Limited EditionJackPas encore d'évaluation

- Hackathon Statements V1Document10 pagesHackathon Statements V1AayushPas encore d'évaluation

- Review of OreoDocument4 pagesReview of OreoNaincy Chhabra0% (1)

- Zero Base Budgeting A and Performance Budgeting 090823145427 Phpapp01Document9 pagesZero Base Budgeting A and Performance Budgeting 090823145427 Phpapp01natrix029Pas encore d'évaluation

- Session 13 Bench Marking 2Document21 pagesSession 13 Bench Marking 2ALIPas encore d'évaluation

- Foxy Originals Case StudyDocument7 pagesFoxy Originals Case StudyJoshua NyabindaPas encore d'évaluation

- LJ Institute of Management Studies (IMBA)Document5 pagesLJ Institute of Management Studies (IMBA)Hardik PatelPas encore d'évaluation

- Prediction of Wine Quality Using Machine LearningDocument12 pagesPrediction of Wine Quality Using Machine LearningSaif Alfarizi100% (1)

- Business Process Engineering A Complete Guide - 2020 EditionD'EverandBusiness Process Engineering A Complete Guide - 2020 EditionPas encore d'évaluation

- Cost and Benefit AnalysisDocument2 pagesCost and Benefit AnalysisGulnara CadenasPas encore d'évaluation

- OW WE Succeed: Genco Atc ImprovementsDocument3 pagesOW WE Succeed: Genco Atc ImprovementsgencoatcPas encore d'évaluation

- Sharp Printing Case Study5211Document3 pagesSharp Printing Case Study5211SarinParikh0% (3)

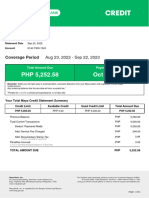

- MayaCredit SoA 2023SEPDocument3 pagesMayaCredit SoA 2023SEPjepoy palaruanPas encore d'évaluation

- Taxguru - In-How To Prepare Directors Report As Per Companies Act 2013Document9 pagesTaxguru - In-How To Prepare Directors Report As Per Companies Act 2013g26agarwalPas encore d'évaluation

- Palweb E-000-000000012241393 21sep2023Document1 pagePalweb E-000-000000012241393 21sep2023Danielle Therese TempladoPas encore d'évaluation

- Mis Proposal Ay 2019 2020Document15 pagesMis Proposal Ay 2019 2020Emmanuel Duria CaindecPas encore d'évaluation

- KushalDocument1 pageKushalKushal SinghalPas encore d'évaluation

- Contemporary World.Document3 pagesContemporary World.Liezel CabilatazanPas encore d'évaluation

- 3Document26 pages3JDPas encore d'évaluation

- Annual ReportDocument160 pagesAnnual ReportSivaPas encore d'évaluation

- Citizens Charter Provides Timelines for Tax ServicesDocument7 pagesCitizens Charter Provides Timelines for Tax ServicesAnonymous tmtyiZAPas encore d'évaluation

- Taxation Academy Handout-CDocument5 pagesTaxation Academy Handout-CMarcellin MarcaPas encore d'évaluation

- Analysing India'S Lability For A Framework in Trade: SUBMITTED TO MR - Animesh Das, Assistant ProfessorDocument19 pagesAnalysing India'S Lability For A Framework in Trade: SUBMITTED TO MR - Animesh Das, Assistant ProfessorVishwaja RaoPas encore d'évaluation

- Commissioner of Internal Revenue v. Procter and Gamble G.R. L-66838Document11 pagesCommissioner of Internal Revenue v. Procter and Gamble G.R. L-66838Dino Bernard LapitanPas encore d'évaluation

- Lec 3 SalaryDocument28 pagesLec 3 SalaryManasi PatilPas encore d'évaluation

- 17-12691 Becker v. Hodges (Order Quashing Writ and Dismissing Petition)Document14 pages17-12691 Becker v. Hodges (Order Quashing Writ and Dismissing Petition)Adam BelzPas encore d'évaluation

- Northeast Federal Credit Union v. Anthony J. Neves, 837 F.2d 531, 1st Cir. (1988)Document9 pagesNortheast Federal Credit Union v. Anthony J. Neves, 837 F.2d 531, 1st Cir. (1988)Scribd Government DocsPas encore d'évaluation

- Government Pay SlipDocument1 pageGovernment Pay SlipBidhya DahalPas encore d'évaluation

- ComputationDocument6 pagesComputationRipfeelingsPas encore d'évaluation

- State Life Building: Supply, Installation, Commissioning Testing of 150 Kva Diesel Generator SetDocument43 pagesState Life Building: Supply, Installation, Commissioning Testing of 150 Kva Diesel Generator SetZia Ur Rehman100% (1)

- Quiz 1 CDocument6 pagesQuiz 1 Crana ahmedPas encore d'évaluation

- Supreme Court rules on local government units' share of national taxesDocument21 pagesSupreme Court rules on local government units' share of national taxesHannah Keziah Dela CernaPas encore d'évaluation