Vous aimerez peut-être aussi

- Project Document (March 2020)Document9 pagesProject Document (March 2020)Wessel BrissettPas encore d'évaluation

- Career Progression WorksheetDocument2 pagesCareer Progression WorksheetWessel BrissettPas encore d'évaluation

- House of RepresentativesDocument3 pagesHouse of RepresentativesWessel BrissettPas encore d'évaluation

- Tour GuidingDocument1 pageTour GuidingWessel BrissettPas encore d'évaluation

- HEART Trust/NTA Community Training: Interventions: (Skill Area (S)Document1 pageHEART Trust/NTA Community Training: Interventions: (Skill Area (S)Wessel BrissettPas encore d'évaluation

- Entertainment Program Revised 2015Document29 pagesEntertainment Program Revised 2015Wessel BrissettPas encore d'évaluation

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (400)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (74)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (121)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- Risk Management ProposalDocument13 pagesRisk Management ProposalromanPas encore d'évaluation

- Authorise Agent 64-8Document3 pagesAuthorise Agent 64-8Hannah LeedhamPas encore d'évaluation

- Mhhs 4 GM NSXBDocument26 pagesMhhs 4 GM NSXBSanchit ChadhaPas encore d'évaluation

- Taxation Finance Act 2022 28Th Edition Alan Melville Full ChapterDocument67 pagesTaxation Finance Act 2022 28Th Edition Alan Melville Full Chapterkenneth.cronin772100% (7)

- 208 Wise V MeerDocument1 page208 Wise V Meeragnes13Pas encore d'évaluation

- T1Q Introduction & RSDocument9 pagesT1Q Introduction & RS吕仙姿Pas encore d'évaluation

- Cash FlowsDocument7 pagesCash FlowsJasmine ActaPas encore d'évaluation

- Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument8 pagesManila Cavite Laguna Cebu Cagayan de Oro DavaoRaymond RosalesPas encore d'évaluation

- HW 6Document3 pagesHW 6Mishalm960% (1)

- Answer Ni Chat GPT HAAHAHADocument3 pagesAnswer Ni Chat GPT HAAHAHAjevocab12Pas encore d'évaluation

- Reimbursement Expense Receipt (RER)Document6 pagesReimbursement Expense Receipt (RER)Alex BuracPas encore d'évaluation

- Tax2 Donalvo 2018 TSN First ExamDocument33 pagesTax2 Donalvo 2018 TSN First ExamsonyaPas encore d'évaluation

- Cremica Food Industries Limited: Tax InvoiceDocument1 pageCremica Food Industries Limited: Tax InvoiceKartik DhimanPas encore d'évaluation

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Gopal SPas encore d'évaluation

- Counties United in Opposition To NYS Budget Proposal That Would Take $625 Million From Local TaxpayersDocument2 pagesCounties United in Opposition To NYS Budget Proposal That Would Take $625 Million From Local TaxpayersNewzjunkyPas encore d'évaluation

- Nutriarc: Tax InvoiceDocument1 pageNutriarc: Tax InvoiceARC FitnessPas encore d'évaluation

- Maulana Azad National Urdu University: CircularDocument4 pagesMaulana Azad National Urdu University: CircularDebasish BiswalPas encore d'évaluation

- Summary of Thailand-Tax-Guide and LawsDocument34 pagesSummary of Thailand-Tax-Guide and LawsPranav BhatPas encore d'évaluation

- RCC Bridge and Culvert DesignDocument1 pageRCC Bridge and Culvert DesignDineshAkshay100% (1)

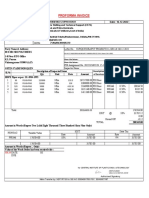

- Srisri Pilymer PI16122022-1Document1 pageSrisri Pilymer PI16122022-1GNANA CHARAN GPas encore d'évaluation

- Tax 301 Income Taxation Module 4 Co Ownership, Estates and TrustDocument6 pagesTax 301 Income Taxation Module 4 Co Ownership, Estates and TrustKristine hazzel ReynoPas encore d'évaluation

- 1 - Shrout Indictment December 15, 2015Document5 pages1 - Shrout Indictment December 15, 2015Freeman LawyerPas encore d'évaluation

- 2007 2013d Suggested Answers JayArhSals LadotDocument334 pages2007 2013d Suggested Answers JayArhSals LadotAngelic TesioPas encore d'évaluation

- RR 02-98 AmendedDocument136 pagesRR 02-98 AmendedPaul Angelo TombocPas encore d'évaluation

- GST Issues Real Estate Sector Yashwant KasarDocument49 pagesGST Issues Real Estate Sector Yashwant KasarSaikrishna AlluPas encore d'évaluation

- 07 DELPHER-TRADES V IACDocument4 pages07 DELPHER-TRADES V IACElla CanuelPas encore d'évaluation

- Subcontractor's Statement PDFDocument2 pagesSubcontractor's Statement PDFAnonymous M4DMq2CZXPas encore d'évaluation

- Income Taxation ReviewerDocument65 pagesIncome Taxation ReviewerShiela100% (10)

- CIR v. Next Mobile, G.R. No. 212825, December 7, 2015.odfDocument7 pagesCIR v. Next Mobile, G.R. No. 212825, December 7, 2015.odfHenry LPas encore d'évaluation

- 2307 For EBS Private Individual Percenateg TaxDocument4 pages2307 For EBS Private Individual Percenateg TaxAGrace MercadoPas encore d'évaluation