Vous aimerez peut-être aussi

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- US Internal Revenue Service: 2290rulesty2007v4 0Document6 pagesUS Internal Revenue Service: 2290rulesty2007v4 0IRSPas encore d'évaluation

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- 2008 Objectives Report To Congress v2Document153 pages2008 Objectives Report To Congress v2IRSPas encore d'évaluation

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 2008 Credit Card Bulk Provider RequirementsDocument112 pages2008 Credit Card Bulk Provider RequirementsIRSPas encore d'évaluation

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 2008 Data DictionaryDocument260 pages2008 Data DictionaryIRSPas encore d'évaluation

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeD'EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeÉvaluation : 4 sur 5 étoiles4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingD'EverandThe Little Book of Hygge: Danish Secrets to Happy LivingÉvaluation : 3.5 sur 5 étoiles3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryD'EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryÉvaluation : 3.5 sur 5 étoiles3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceD'EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceÉvaluation : 4 sur 5 étoiles4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)D'EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Évaluation : 4 sur 5 étoiles4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeD'EverandShoe Dog: A Memoir by the Creator of NikeÉvaluation : 4.5 sur 5 étoiles4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureD'EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureÉvaluation : 4.5 sur 5 étoiles4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItD'EverandNever Split the Difference: Negotiating As If Your Life Depended On ItÉvaluation : 4.5 sur 5 étoiles4.5/5 (838)

- Grit: The Power of Passion and PerseveranceD'EverandGrit: The Power of Passion and PerseveranceÉvaluation : 4 sur 5 étoiles4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaD'EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaÉvaluation : 4.5 sur 5 étoiles4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerD'EverandThe Emperor of All Maladies: A Biography of CancerÉvaluation : 4.5 sur 5 étoiles4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealD'EverandOn Fire: The (Burning) Case for a Green New DealÉvaluation : 4 sur 5 étoiles4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersD'EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersÉvaluation : 4.5 sur 5 étoiles4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnD'EverandTeam of Rivals: The Political Genius of Abraham LincolnÉvaluation : 4.5 sur 5 étoiles4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaD'EverandThe Unwinding: An Inner History of the New AmericaÉvaluation : 4 sur 5 étoiles4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyD'EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyÉvaluation : 3.5 sur 5 étoiles3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreD'EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreÉvaluation : 4 sur 5 étoiles4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)D'EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Évaluation : 4.5 sur 5 étoiles4.5/5 (119)

- Her Body and Other Parties: StoriesD'EverandHer Body and Other Parties: StoriesÉvaluation : 4 sur 5 étoiles4/5 (821)

- All AcDocument32 pagesAll AcVinod KumarPas encore d'évaluation

- ATM Timeout or Command RejectDocument21 pagesATM Timeout or Command RejectDass HariPas encore d'évaluation

- Taxation II Final Exam ReviewDocument2 pagesTaxation II Final Exam ReviewnoelremolacioPas encore d'évaluation

- Tax Invoice: 36AADCM3491M1Z2 30AAACC6253G1Z6Document1 pageTax Invoice: 36AADCM3491M1Z2 30AAACC6253G1Z6VIDHI JAINENDRASINH RANAPas encore d'évaluation

- Government Suspense AccountsDocument63 pagesGovernment Suspense Accountsbharanivldv9Pas encore d'évaluation

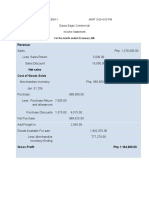

- Davao Eagle Commercial January Income StatementDocument6 pagesDavao Eagle Commercial January Income Statementablay logenePas encore d'évaluation

- CFAS: Petty Cash Fund AccountingDocument3 pagesCFAS: Petty Cash Fund AccountingSteffanie OlivarPas encore d'évaluation

- Chapter 1-Introduction To Taxation PDFDocument7 pagesChapter 1-Introduction To Taxation PDFAbraham ChinPas encore d'évaluation

- Panasonic Communications Imaging Corp. v. CIRDocument3 pagesPanasonic Communications Imaging Corp. v. CIRAbigayle RecioPas encore d'évaluation

- Echallan MH000503223202324 EDocument1 pageEchallan MH000503223202324 Eankit trivediPas encore d'évaluation

- Screenshot 2023-12-12 at 2.34.53 PMDocument1 pageScreenshot 2023-12-12 at 2.34.53 PMshashikumarsk0711Pas encore d'évaluation

- Apply NEFT funds transfer onlineDocument5 pagesApply NEFT funds transfer onlinePPCPL Chandrapur0% (1)

- Auth Representative Consent FormDocument2 pagesAuth Representative Consent FormRaminder SinghPas encore d'évaluation

- 50% Discount for Women Candidates at Fosma Maritime InstituteDocument2 pages50% Discount for Women Candidates at Fosma Maritime InstituteAshis SarkarPas encore d'évaluation

- Emergent Payments India Private Limited Tax InvoiceDocument1 pageEmergent Payments India Private Limited Tax InvoiceSuganthan SundharamPas encore d'évaluation

- Unicredit vs. IngDocument3 pagesUnicredit vs. IngAlina AndrioaePas encore d'évaluation

- Tax incentives for BioNexus companiesDocument41 pagesTax incentives for BioNexus companiesagasthia23Pas encore d'évaluation

- CashDocument7 pagesCashhellohello100% (1)

- Bank account statement details for Mr. BODA MALLESHDocument5 pagesBank account statement details for Mr. BODA MALLESHSanthosh Naik BhukyaPas encore d'évaluation

- Alnissiy Yemen - 04052018 Quo-33397 Batry + Spares YemenDocument2 pagesAlnissiy Yemen - 04052018 Quo-33397 Batry + Spares YemenSamir AjiPas encore d'évaluation

- DAV Public School Jasola Vihar Fee Receipt for Gourav Thakur Class IXDocument1 pageDAV Public School Jasola Vihar Fee Receipt for Gourav Thakur Class IXGauravthakur 9BPas encore d'évaluation

- ITR-2 Form PDFDocument22 pagesITR-2 Form PDFChandra SekaranPas encore d'évaluation

- Saudi Arabia Tax SetupDocument23 pagesSaudi Arabia Tax SetupAnshuanupamPas encore d'évaluation

- PolicyDocument3 pagesPolicyBhavsmeetforeverPas encore d'évaluation

- Country Specific Document XMLv3 Santander BrazilDocument21 pagesCountry Specific Document XMLv3 Santander BrazilJimmy De la CruzPas encore d'évaluation

- Philamlife vs. SOFDocument1 pagePhilamlife vs. SOFMichellePas encore d'évaluation

- Donor's Tax Exam AnswersDocument6 pagesDonor's Tax Exam AnswersKyla BarbosaPas encore d'évaluation

- GST ProjectDocument24 pagesGST ProjectPratyush DeroliaPas encore d'évaluation

- Payment and Settlements in India-ExamPundit FinalDocument8 pagesPayment and Settlements in India-ExamPundit FinalUjjwal MishraPas encore d'évaluation

- Eight Methods To Pay Vendor in SapDocument7 pagesEight Methods To Pay Vendor in Sapadit1435Pas encore d'évaluation